ERIE INDEMNITY (ERIE)·Q4 2025 Earnings Summary

Erie Indemnity Q4 2025: CEO Announces Retirement as $100M Charitable Gift Masks Underlying Strength

February 24, 2026 · by Fintool AI Agent

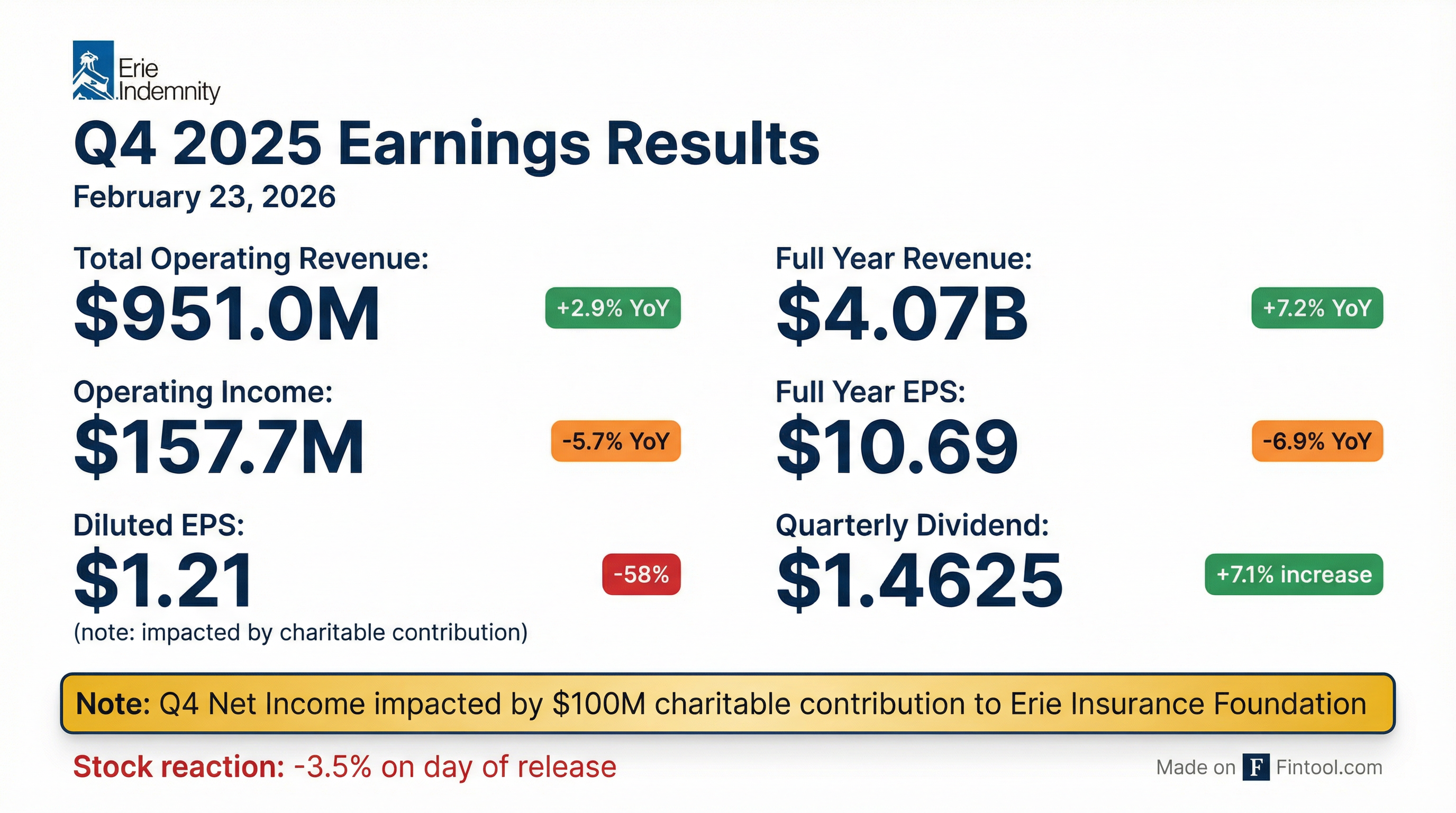

Erie Indemnity Company (NASDAQ: ERIE) wrapped up its centennial year with a Q4 report that buried the lede: CEO Tim Nicastro announced he will retire at the end of 2026 . The stock has fallen 5%+ over two days, trading at $258.42 today after closing at $263.77 yesterday — now down 43% from its 52-week high.

The headline EPS of $1.21 (down 58% YoY) was distorted by a $100 million charitable contribution to the newly-formed Erie Insurance Foundation. Strip that out, and normalized EPS of $2.76 beat consensus of $1.59 by 74%.* More importantly, the Erie Insurance Exchange's combined ratio improved 11.6 points to 94.1% in Q4, signaling the rate actions are finally working.

Did Erie Indemnity Beat Earnings?

On a normalized basis, yes. Q4 2025 normalized EPS came in at $2.76, beating consensus of $1.59 by 74%.* Reported GAAP EPS was $1.21, down 58% from $2.91 in Q4 2024.

The distortion came entirely from the $100M contribution to the Erie Insurance Foundation, a tax-exempt private charitable foundation formed in 2025. The after-tax impact was $80.6 million, or $1.54 per diluted share.

*Values retrieved from S&P Global

Adjusted for the charitable contribution, net income would have been approximately $144M — within striking distance of the prior year's $152M.

CEO Tim Nicastro Announces Retirement

The biggest news from the earnings call: CEO Tim Nicastro announced his intention to retire at the end of 2026.

"Having the opportunity to lead this company, especially during its hundredth year, has been the greatest privilege of my professional life. Erie is a special organization built on strong values, deep relationships, and an unwavering commitment to service."

Nicastro emphasized:

- Continuity: "We have an exceptional team in place"

- Focus: Strategy execution remains the priority over the next year

- Transition: Management is working to ensure "a thoughtful and seamless leadership transition"

No successor has been named. Investors should watch for board announcements on the CEO search process.

How Did the Erie Insurance Exchange Perform?

The real story in Q4 was the dramatic improvement in Exchange underwriting profitability. Erie Indemnity manages the Erie Insurance Exchange and earns fees based on premium volume — when the Exchange improves, Indemnity benefits.

Key takeaway: Despite catastrophe losses running 1 point higher than 2024, the rate actions implemented over the past several years are driving improved loss ratios. The Q4 combined ratio of 94.1% shows the underlying business is now comfortably profitable when cat losses are minimal.

Headwinds to watch:

- Policies in force declined 1.1% (still above 7 million)

- Retention fell to 88.4%

- Competitive market conditions continue

What Drove Operating Performance?

Operating income before taxes declined 5.7% to $157.7M despite revenue growth, as commission costs and non-commission expenses outpaced fee revenue growth.

Revenue Drivers:

- Management fee revenue (policy issuance) grew 4.2% to $727.6M, driven by premium growth at the Erie Insurance Exchange

- Management fee revenue (administrative services) increased 12.0% to $19.3M

Cost Pressures:

- Commissions increased $30.1M due to premium growth and higher agent incentive compensation from improved property and casualty underwriting profitability

- Non-commission expenses rose $10.4M, driven by IT costs (+$4.5M on personnel, hardware/software), administrative costs (+$5.8M on personnel), and community development initiatives

Full Year 2025: Underlying Strength

The full year picture tells a different story. Excluding the charitable contribution, Erie Indemnity's core business delivered solid growth:

Operating income grew 6.0% (~$41M) as management fee revenue from policy issuance increased 8.2%, reflecting strong premium growth at the Exchange.

Investment income also contributed, rising to $84.9M from $69.3M (+22.5%), with net investment income of $85.8M vs $70.2M in the prior year.

What's the Charitable Foundation Story?

In 2025, Erie Indemnity formed the Erie Insurance Foundation, a tax-exempt private charitable foundation designed to "create long-term sustainability for charitable contributions and grantmaking."

The $100M contribution in Q4 2025 was the initial funding of this foundation. This is a one-time event — the foundation is now established and future contributions should be normalized as part of ongoing operations.

Key context: Erie Insurance Group positions itself as community-focused (ranked 11th largest homeowners insurer, 12th largest auto insurer in the US), and this foundation likely formalizes what had previously been ad-hoc giving.

What's New in Products and Strategy?

Management highlighted several initiatives during the earnings call that position Erie for 2026:

Erie Secure Auto Rollout

This new product offers "more flexible and competitive rates" and is gaining traction:

- Ohio pilot (Fall 2025): "Impressive impacts" on submitted applications and direct written premiums

- West Virginia: Deployed late December 2025

- Virginia: Deployed February 2026

- More states: Expected in first half of 2026

Business Auto 2.0 Expansion

The commercial lines product improves quoting and servicing experience:

- North Carolina: Released late January 2026

- Total footprint: Now in 9 states

- More expansion: Expected before end of Q1 2026

Erie Strategic Ventures

Erie's venture capital arm (launched 2022) made two new investments:

- Atomic: Embedded brokerage and wealth management for financial institutions

- Feathery: AI-powered data intake platform for manual process automation

Recent Recognition

- J.D. Power 2025: #1 in U.S. Auto Claims Satisfaction — highest ranking in customer claim satisfaction among auto insurers

- J.D. Power (Sept 2025): #1 in Small Business Insurance Customer Satisfaction

- Newsweek: Named to America's Best Customer Service 2026 list

How Did the Stock React?

Badly. ERIE shares fell 3.5% on February 23 after the 8-K release, then fell another 2% on February 24 following the earnings call recording.

Two-day decline: -5.5% since earnings release. The stock is now trading well below both its 50-day ($282) and 200-day ($322) moving averages, confirming the bearish trend.

What Changed From Last Quarter?

Q4 2025 vs Q3 2025:

- Operating revenue down 10.8% sequentially ($951M vs $1,067M) — normal seasonality

- Operating income down 26.5% ($157.7M vs $214.6M) — mix of seasonality and cost timing

- Net income cratered due to $100M charitable contribution

The bigger change is capital allocation. The Erie Insurance Foundation represents a new, permanent structure for charitable giving that didn't exist before 2025. While the $100M was a one-time catch-up, investors should expect some level of ongoing contributions.

Dividend: A Bright Spot

The Board approved a quarterly dividend increase:

Key dates:

- Ex-Dividend: April 7, 2026

- Record Date: April 7, 2026

- Payment: April 21, 2026

The dividend increase signals management confidence in underlying cash generation despite the headline EPS decline.

Investment Income Strength

Investment income provided a tailwind, up 16.2% YoY in Q4:

For the full year, investment income totaled $84.9M vs $69.3M (+22.5%).

Balance Sheet Snapshot

The balance sheet remains healthy with strong liquidity and growing equity despite the charitable contribution.

Key Risks Flagged

Management's forward-looking statements highlighted several risk factors:

- Exchange Dependence — Erie Indemnity's business is entirely tied to the Erie Insurance Exchange's performance and the management fee agreement

- Catastrophe Exposure — Severe weather and catastrophic losses remain a key risk for the Exchange (which flows through to Indemnity via reduced premium growth)

- Technology & Cyber Risk — Investment in IT continues, but data/network security breaches remain a concern

- Regulatory & Litigation — Changes in insurance regulation could impact operations

- Economic/Social Inflation — Emerging claims and coverage issues in the industry

- CEO Succession — Leadership transition risk as Tim Nicastro prepares to retire

The Bottom Line

Strip out the noise: Erie Indemnity's core business is performing well. Operating income grew 6% for the full year, management fee revenue is up 8%+, and the dividend got hiked 7%. The $100M charitable contribution was a one-time event to establish the Erie Insurance Foundation.

The Exchange is healing. A Q4 combined ratio of 94.1% shows that when cat losses are minimal, the rate actions of the past few years are delivering profitability. Policyholder surplus grew $800M to $10.1B.

But uncertainty is rising. The stock has fallen 5%+ since earnings, now trading at $258 — down 43% from its 52-week high. Key concerns:

- CEO succession — Tim Nicastro retiring at end of 2026 with no successor named

- Policy retention declining — 88.4% retention and -1.1% policies in force

- Competitive headwinds — Market conditions contributing to slowdown

- Cat exposure — First half of 2025 included "costliest weather event in our history"

Catalyst watch: Erie Secure Auto rollout shows early promise in Ohio. If the product drives meaningful new business growth, it could help offset retention pressure.

Related: ERIE Company Page | Q4 2025 8-K Filing