Empire State Realty Trust (ESRT)·Q4 2025 Earnings Summary

Empire State Realty Trust Q4 2025: Revenue Beats as NYC Transformation Completes

February 18, 2026 · by Fintool AI Agent

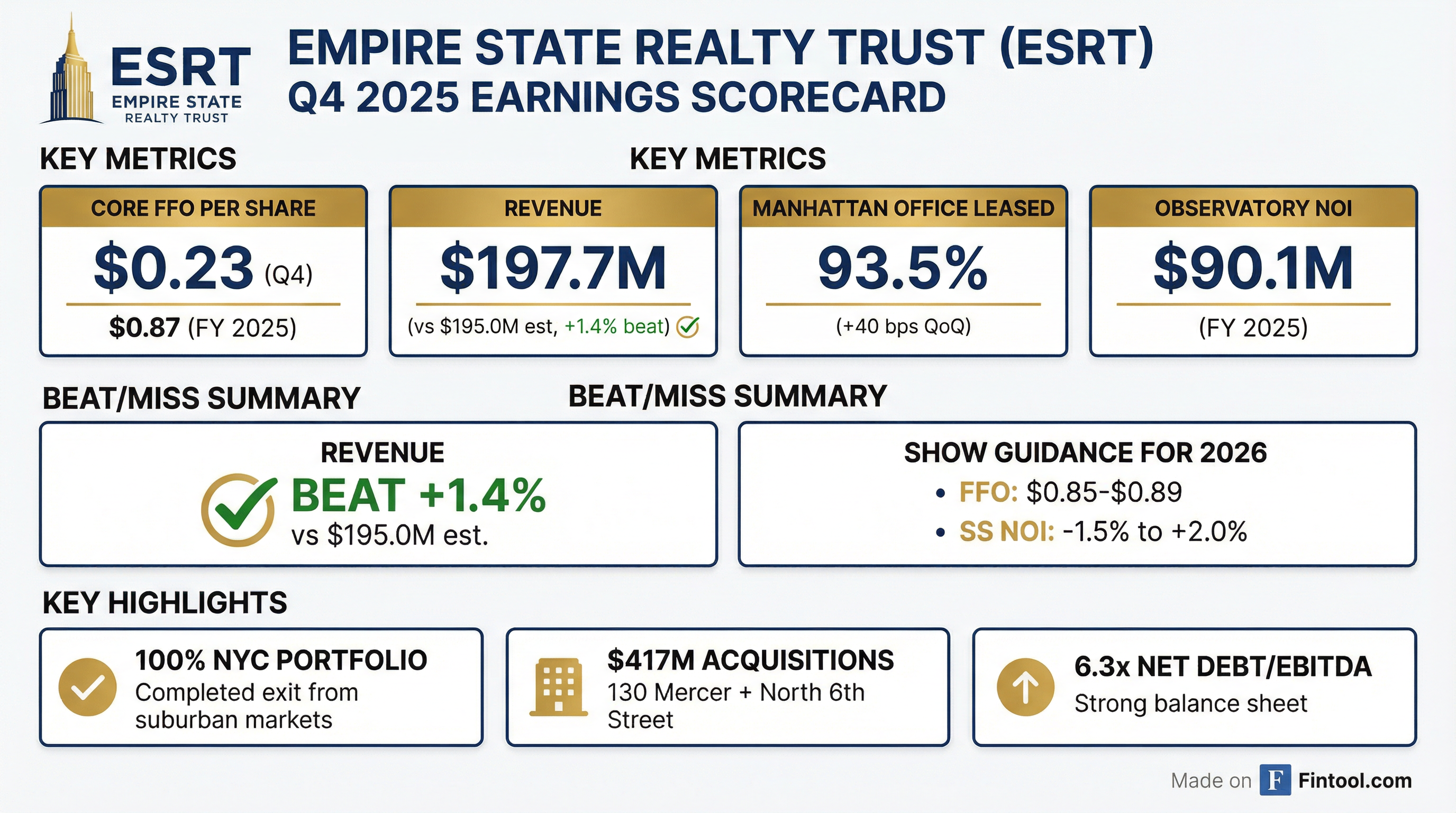

Empire State Realty Trust reported Q4 2025 results that topped revenue expectations while completing its strategic pivot to a pure-play NYC portfolio. Revenue of $197.7M beat consensus by 1.4%, driven by continued leasing momentum in the Manhattan office segment. Core FFO of $0.23 per share brought full-year 2025 FFO to $0.87, though 2026 guidance suggests modest near-term headwinds from a temporary FDIC lease expiration.

The stock has struggled over the past year, trading near 52-week lows at $6.39 versus a high of $9.27, reflecting broader REIT sector challenges and elevated interest rates.

Did ESRT Beat Earnings?

Revenue beat by 1.4%. ESRT reported Q4 revenue of $197.7M versus consensus expectations of $195.0M. For the full year, revenue totaled approximately $627M.*

*Values retrieved from S&P Global

For a REIT, the key metric is Funds From Operations (FFO), not GAAP EPS. ESRT delivered Core FFO of $0.23 per share in Q4, consistent with prior quarters, bringing full-year 2025 Core FFO to $0.87.

Beat/miss context: ESRT has now beaten revenue estimates in 3 of the last 4 quarters:

*Values retrieved from S&P Global

What Did Management Guide?

2026 guidance implies flat FFO with meaningful headwinds from a temporary lease expiration:

Key guidance detail: Management flagged a ~$0.03 FFO headwind and ~270 bps same-store NOI impact from temporary downtime related to a previously disclosed FDIC lease expiration, which has already been re-leased.

G&A cost reduction: ESRT expects to exit 2026 with run-rate G&A down 5-10% versus the 2025 baseline, demonstrating expense discipline.

How Did the Stock React?

ESRT shares have been under pressure, trading near 52-week lows:

The stock's underperformance reflects several factors: higher interest rates pressuring REIT valuations, the Observatory's tourism-dependent revenue facing international visitation headwinds, and broader concerns about office sector fundamentals.

What Changed From Last Quarter?

1. Portfolio Transformation Complete

ESRT has now fully exited suburban commercial markets and transitioned to a 100% NYC portfolio. In 2025, the company:

- Completed disposition of Metro Center in Stamford, CT (final suburban asset)

- Executed $417M in all-cash acquisitions: 130 Mercer Street/Scholastic Building and 86-90 North 6th Street

- Achieved this transition in a tax-efficient manner through 1031 exchanges, recognizing no taxable gain

Management projects these acquired NYC assets will generate approximately $90M of cumulative property-level incremental cash flow in 2025-2030 versus the suburban assets sold.

2. Strong Office Leasing Momentum

Manhattan office fundamentals continue to improve:

The 18 consecutive quarters of positive mark-to-market on office leases is a standout metric, demonstrating ESRT's pricing power in a challenging market.

3. Observatory Pressured by International Tourism

The Empire State Building Observatory—responsible for 22% of NOI—delivered $90.1M in 2025 NOI, impacted by reduced budget-conscious international visitation.

Management is taking a disciplined approach with cost management and price execution, positioning for growth when international demand recovers.

Balance Sheet and Capital Allocation

ESRT maintains one of the strongest balance sheets among NYC REITs:

Q4 capital markets activity:

- Executed $420M of financings: $175M unsecured notes + $245M term loan recast

- Repurchased $6M of shares in Q4, $8M for full year 2025 (>$300M since 2020)

The 100% owned asset portfolio with limited secured debt and high-quality unencumbered assets (including 130 Mercer and North Sixth Street Collection) provides significant capital structure optionality.

Key Property Highlights

130 Mercer Street ($386M Acquisition)

ESRT's largest 2025 acquisition offers embedded upside:

- Location: Prime SoHo mixed-use (368K sf office + 28K sf retail)

- In-place yield: Unlevered mid-5% at 70% occupancy

- Anchor tenants: 15-year Scholastic office lease (222K sf) + fully leased retail (Sephora, Capital One)

- Upside: 110K+ sf vacant office block with large floor plates (~37K sf) in supply-constrained market

North Sixth Street Collection ($250M Portfolio)

Four key street corner retail assets in Williamsburg, Brooklyn:

- Unencumbered with strong leasing since acquisition

- High-foot traffic, strong local demographics (49% households earn $100K+)

- Significant mark-to-market potential over time

Embedded Growth: Office Mark-to-Market

ESRT's office portfolio has significant embedded rental upside through lease expirations:

Additionally, incremental cash NOI from signed leases not commenced (SLNC) and free rent burn-off is projected to add:

Management Priorities

CEO Anthony Malkin and the leadership team outlined three priorities for 2026:

- Lease space: Maximize occupancy in the Manhattan office portfolio following +600 bps lease-up since 2021

- Manage the balance sheet: Maintain flexibility for opportunistic capital deployment while assessing share repurchases

- Sell Observatory tickets: Position for growth when international demand recovers with disciplined cost management

Forward Catalysts

Bullish:

- Observatory recovery when international tourism rebounds

- Continued office mark-to-market gains as leases roll

- 130 Mercer office lease-up (110K+ sf opportunity)

- Interest rate cuts benefiting REIT valuations

- Share repurchases at depressed valuations

Bearish:

- Prolonged weakness in international tourism

- FDIC lease downtime impacting near-term results

- Higher-for-longer interest rates

- NYC office sentiment remains challenged

Key Takeaways

- Revenue beat: Q4 revenue of $197.7M topped consensus by 1.4%

- Portfolio transformation complete: Now 100% NYC-focused with superior growth profile

- Office momentum continues: 93.5% leased, 18th consecutive quarter of positive spreads

- Guidance implies temporary headwinds: 2026 FFO of $0.85-$0.89 reflects FDIC lease transition

- Strong balance sheet: 6.3x leverage, lowest among NYC peers, providing optionality

This analysis was generated by Fintool AI Agent based on ESRT's Q4 2025 earnings presentation filed February 18, 2026.