ExlService Holdings (EXLS)·Q4 2025 Earnings Summary

EXL Beats Q4 Estimates as AI-Driven Data Services Fuel 13% Revenue Growth

February 24, 2026 · by Fintool AI Agent

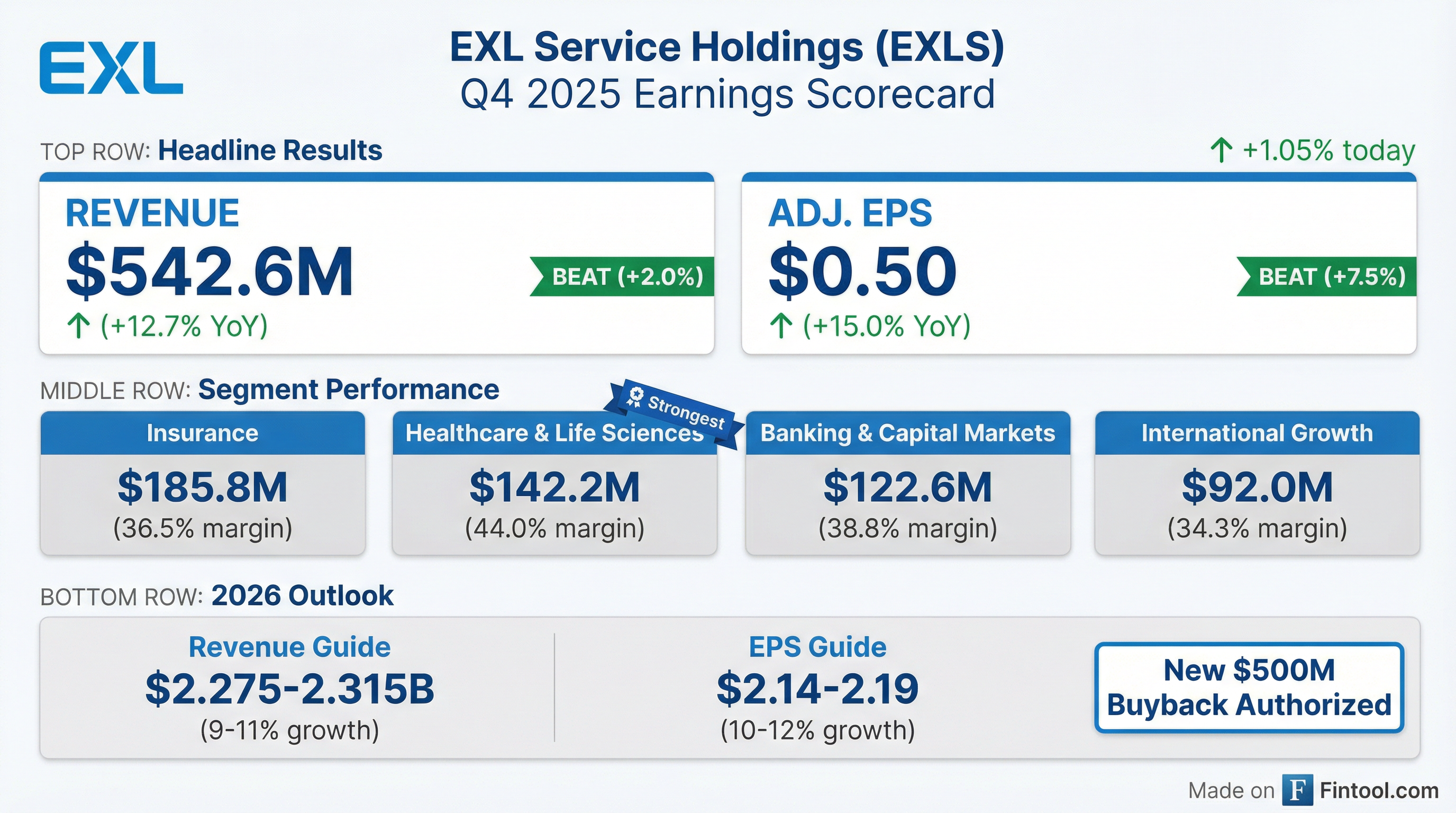

EXL Service Holdings delivered a solid Q4 2025, beating both revenue and earnings estimates as the data and AI services provider extended its streak of outperformance to eight consecutive quarters. Revenue grew 12.7% year-over-year to $542.6 million, while adjusted EPS increased 15.0% to $0.50. The company's Board authorized a new $500 million stock repurchase program, signaling confidence in the business trajectory despite broader market headwinds that have pressured the stock this year.

Did EXL Beat Earnings?

Yes — EXL beat on both revenue and adjusted EPS.

This marks EXL's eighth consecutive quarter of adjusted EPS beats, demonstrating consistent execution across its data and AI services portfolio.

Full Year 2025 Results:

What Did Management Guide for 2026?

EXL provided FY 2026 guidance reflecting continued confidence in its data and AI positioning:

Guidance assumptions include USD/INR at 90.0, GBP/USD at 1.34, and USD/PHP at 59.0.

Capital Return: The Board authorized a $500 million stock repurchase program effective February 28, 2026, for a two-year period. CFO Maurizio Nicolelli noted this "represents confidence in our ability to continue our growth trajectory and generate significant free cash flow."

What's Driving the Growth?

Healthcare & Life Sciences: The Standout Performer

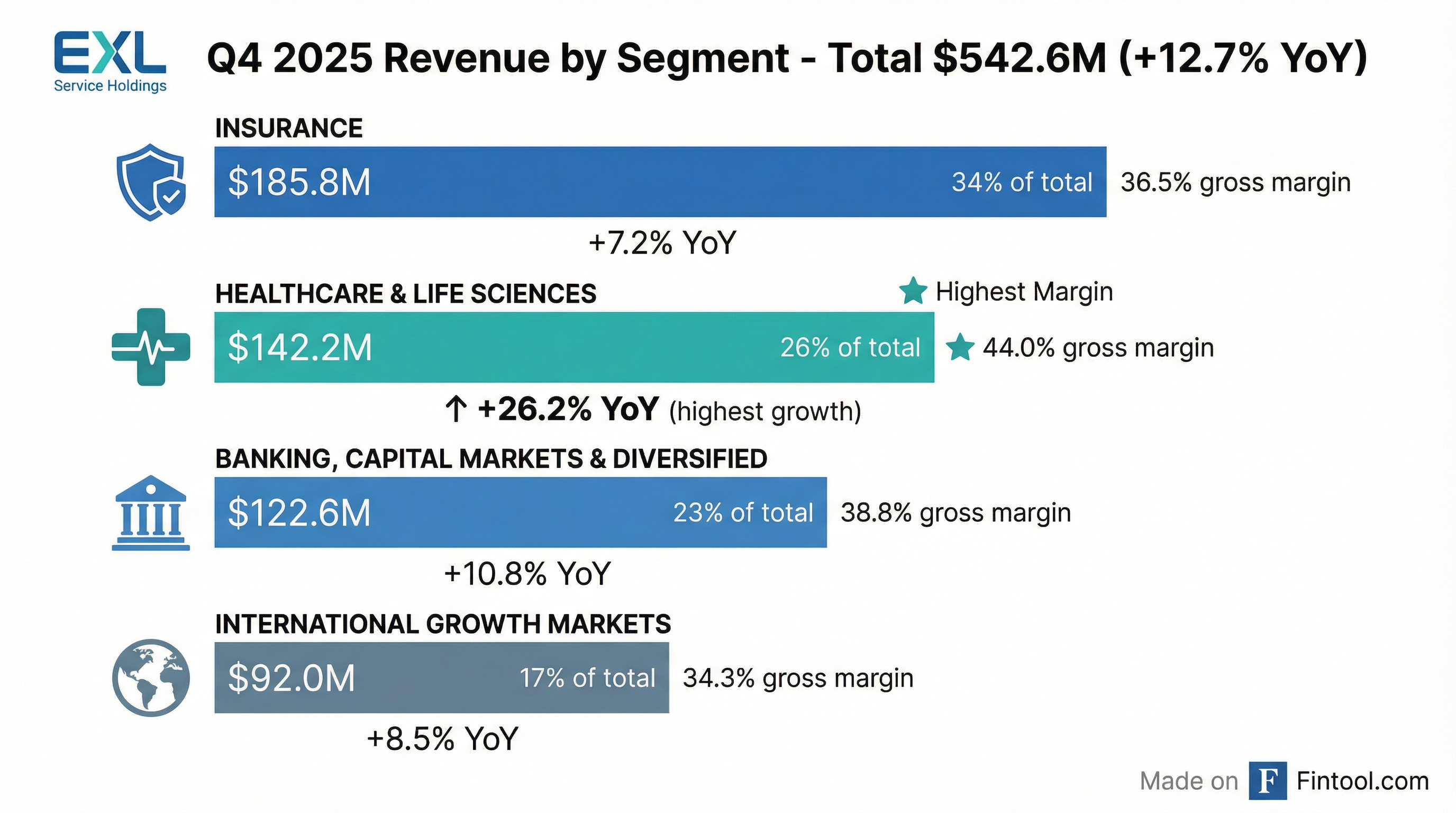

Q4 2025 Segment Performance:

Healthcare & Life Sciences stood out with 26.2% YoY growth and the highest gross margin at 44.0%, reflecting strong demand for EXL's data analytics and AI solutions in clinical operations and health plan services.

Strategic Highlights

- Won 21 new clients in Q4 2025 and 65 new clients for full year 2025

- Launched EXLdata.ai — a first-of-its-kind agentic AI-native suite of data solutions

- Insurance fraud platform collaboration announced with Insurance Council of Australia and Shift

- Named a Leader in ISG Provider Lens for Generative AI Services (Global) and Healthcare Digital Services (US)

CEO Rohit Kapoor emphasized: "EXL's recognized industry expertise and leadership in embedding AI in our clients' businesses are resonating strongly with the market and fueling our growth with new and existing clients."

How Did the Stock React?

Post-Earnings Reaction: EXLS stock rose +1.05% on earnings day to $28.75, a muted response despite the beat.

Context matters: The stock has been under significant pressure in 2026:

The stock's YTD decline appears driven by broader concerns around IT services spending and valuation compression in the sector, rather than company-specific issues. The new $500M buyback program may provide support at these depressed levels.

What Changed From Last Quarter?

Key delta: Adjusted operating margin dipped 60 bps sequentially to 18.8%, though this remained flat vs. Q4 2024. Healthcare margin expansion continued, while International Growth Markets saw margin compression from 35.8% to 34.3%.

Historical Beat/Miss Track Record

EXL has delivered consistent execution with 8 consecutive quarters of EPS beats:

Margin Trends

Margins have been stable with slight compression in Q4, likely reflecting seasonal factors and continued investment in AI capabilities.

The Bottom Line

EXL delivered a clean beat in Q4 2025, extending its streak of execution to 8 straight quarters. The standout was Healthcare & Life Sciences growing 26% with 44% gross margins — a clear indicator of AI-enabled services demand. FY 2026 guidance of 9-11% revenue growth and 10-12% EPS growth remains solid, supported by a new $500M buyback that signals management confidence.

The disconnect: Despite consistent beats, the stock is down 30% YTD and trades near 52-week lows. The valuation compression across IT services has created a situation where EXL trades at a significant discount to its historical multiple. For investors, the question is whether the market is pricing in a growth slowdown that hasn't materialized — or if there's deeper concern about AI-driven disruption to traditional BPO models that EXL has been adept at navigating.

Data sourced from EXL's Q4 2025 8-K filing and earnings press release dated February 24, 2026. Values retrieved from S&P Global where noted.