FIRST COMMONWEALTH FINANCIAL CORP /PA/ (FCF)·Q4 2025 Earnings Summary

First Commonwealth Posts Record Quarter as NIM Expansion Drives 23% Earnings Beat

January 28, 2026 · by Fintool AI Agent

First Commonwealth Financial Corporation (FCF) delivered a strong Q4 2025, beating both EPS and revenue estimates as net interest margin expansion continued to drive profitability higher. The Pennsylvania-based regional bank reported diluted EPS of $0.43, up 23% year-over-year and 10% sequentially, capping a record year for the company.

Did First Commonwealth Beat Earnings?

Yes — beat on both metrics.

This marks the seventh consecutive quarter of meeting or exceeding EPS estimates, with only Q3 2024 as a miss over the past two years. The beat was driven by:

- Net interest income (FTE) of $113.6M, up $2.1M from Q3 2025

- Core pre-tax pre-provision net revenue of $63.2M, up $11.8M YoY

- Lower provision expense of $7.0M vs $11.3M in Q3 2025

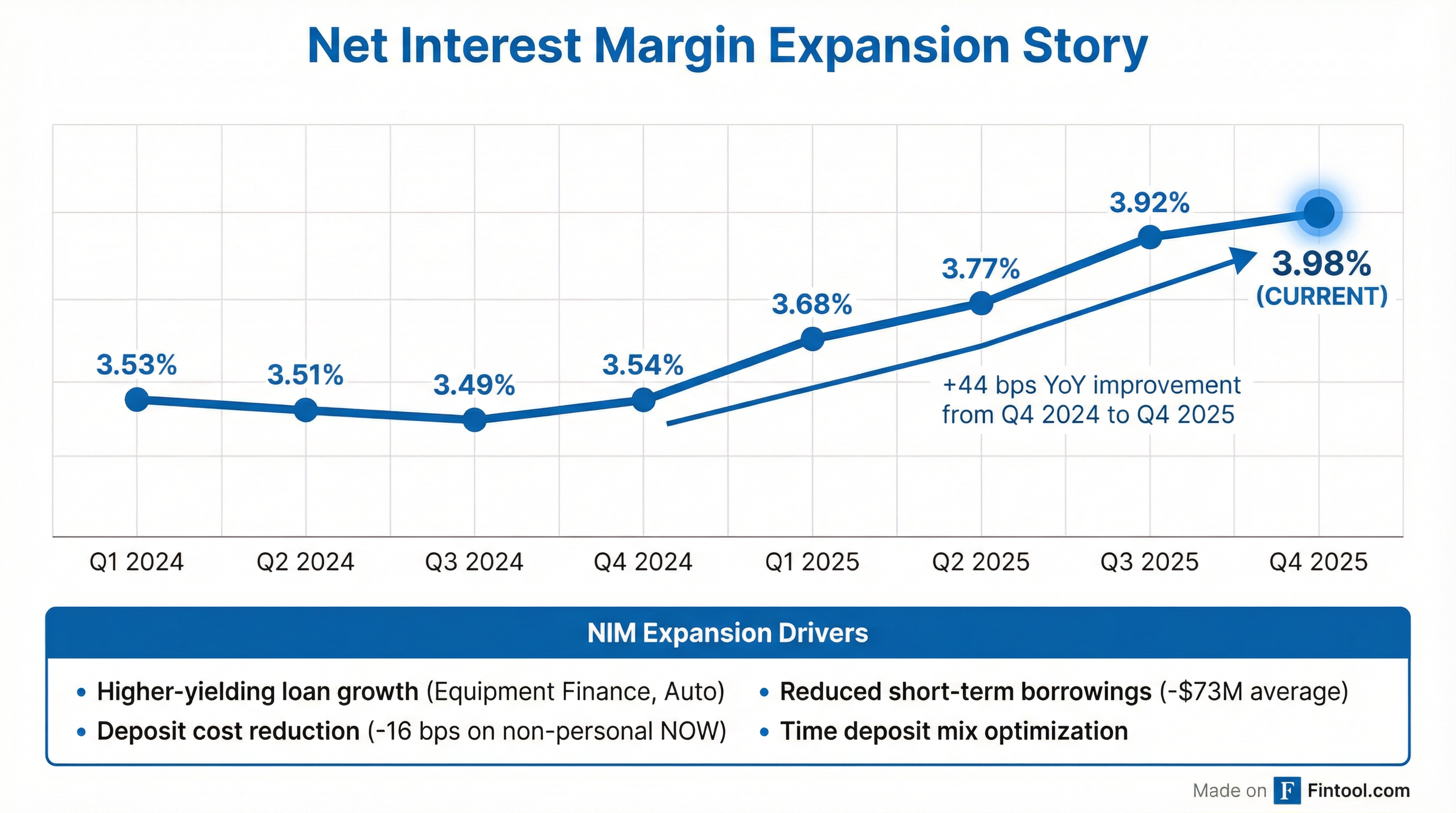

What's Driving the Margin Expansion?

The standout story remains net interest margin (NIM) — First Commonwealth's primary earnings engine continued its impressive expansion trajectory.

Key NIM drivers this quarter:

- Higher-yielding loan growth — Indirect auto loan yields increased 11 bps with $32.3M balance growth; equipment finance loans grew $51.5M

- Deposit cost reduction — Non-personal NOW account costs fell 16 bps

- Reduced wholesale funding — Average short-term borrowings down $73.4M

How Did Profitability Metrics Trend?

First Commonwealth's profitability metrics hit multi-year highs:

The 323 bps improvement in efficiency ratio YoY reflects operating leverage from revenue growth outpacing expense growth.

What Changed From Last Quarter?

Loan Portfolio

Total loans increased $28.6M (1.2% annualized) from Q3 2025, driven by:

- Equipment Finance: Continued strong growth

- Construction: Portfolio expansion

- Loans Held for Sale: Increased $208.9M as $225.4M of commercial loans were designated for sale

Deposit Trends

- Average deposits grew $72.0M (2.8% annualized) QoQ

- End-of-period deposits declined $19.6M (0.8% annualized)

- Loan-to-deposit ratio: 95.4% for FY 2025 vs 93.4% in FY 2024

Noninterest Income

Noninterest income (excluding securities gains) of $24.3M decreased $0.2M from Q3 2025:

Full-year noninterest income declined $3.0M due to the Durbin amendment impact on card interchange ($6.3M headwind), partially offset by growth in wealth fees, mortgage gains, and swap income.

Expenses

Noninterest expense (excluding merger costs) of $74.3M increased $1.7M from Q3 2025:

- Salaries and benefits: +$1.5M

- Software expense: +$0.7M

- PA shares tax adjustment: -$0.9M (favorable)

Full-time equivalent staff: 1,567 at quarter-end vs 1,548 in Q3 2025.

How Is Credit Quality Trending?

Asset quality showed mixed signals — charge-offs improved while criticized loans increased:

Key observations:

- Provision expense of $7.0M decreased $4.3M QoQ, primarily due to a $4.4M dealer floorplan provision in Q3 2025

- Nonperforming loans increased $3.1M to $91.8M

- Reserve build was negative ($3.8M release) as charge-offs exceeded provisions

- Net charge-off breakdown: Commercial loans drove $7.2M of the $11.3M total

The uptick in criticized loans (+$19M QoQ) and NPLs bears watching, though the allowance coverage ratio of 137% remains adequate.

What Did Management Announce?

Capital Return

Dividend increased 3.9% — declared $0.135/share (vs $0.13 in Q4 2024), payable February 20, 2026 to shareholders of record February 6, 2026. At the January 26, 2026 closing price of $17.53, this represents a 3.1% annualized yield.

$25M additional share repurchase authorized in January 2026. In Q4 2025, the company repurchased 1,451,296 shares at a weighted average price of $15.94.

Executive Transitions

- Jane Grebenc, Bank President and Chief Revenue Officer, retiring at the end of March 2026. CEO Mike Price noted she "has left an indelible mark on First Commonwealth" and "played a pivotal role in the strategic transformations that have helped position First Commonwealth as a top quartile performer."

- Norman Montgomery, Executive Vice President and Business Integration Group Manager, retiring effective May 1, 2026

CEO Commentary

"Our fourth quarter results capped off a strong year for First Commonwealth, highlighted by solid loan and deposit growth, continued expansion of our net interest margin, and stable capital levels. We delivered improved profitability this quarter while maintaining sound credit quality and strengthening our balance sheet through core deposit growth."

— T. Michael Price, President and CEO

How Did the Stock React?

FCF shares rose +1.9% following the earnings release, trading at $18.04 and approaching the 52-week high of $18.42.

The stock is up 33% from its 52-week low and trading at a 7% premium to the 200-day moving average.

Full Year 2025 Summary

What's the Capital Position?

First Commonwealth maintains a strong capital position well above regulatory requirements:

The bank-level Total Regulatory Capital ratio of 13.4% represents $348M in excess capital above the 10% "well capitalized" threshold.

Key Risks and Concerns

-

Credit deterioration watch — NPLs at 0.94% are up 26 bps YoY; criticized loans up 19% YoY

-

Durbin amendment headwind — Full-year impact of $6.3M on interchange income will persist

-

Rate sensitivity — Further Fed rate cuts could pressure the NIM expansion story

-

Loan portfolio reshuffling — $225.4M of commercial loans moved to held-for-sale as part of Philadelphia market exit (confirmed as strategic, not credit-driven)

-

Executive transitions — Two senior leaders (Jane Grebenc, Norman Montgomery) retiring in 2026 may impact institutional knowledge

-

Spread compression — Commercial real estate spreads compressed due to aggressive agency/insurance markets; management maintaining discipline on structure and recourse

Forward Catalysts

- Q1 2026 earnings — expected late April 2026

- Completion of commercial loan sales — impact on capital and earnings mix

- Continued NIM trajectory — room for further expansion if deposit costs continue declining

- Potential M&A — strong capital position supports deal capacity

Q&A Highlights

Key themes from analyst questions on the earnings call:

NIM Outlook

CFO Jim Reske provided detailed margin guidance:

"The amount of the dip we think is anywhere from 5-10 [basis points]... And then it drifts upward around 5 basis points a quarter. It ends up... around 4%."

— Jim Reske, CFO

Key drivers of NIM trajectory:

- Fed rate cuts not fully reflected in SOFR-based loans yet — will hit Q1

- Macro swaps rolling off in 2026 (big chunk in May) will support margin

- Q4 NIM benefited ~3 bps from NPL recoveries (non-recurring)

Credit Quality Details

On the dealer floor plan resolution:

"We ended the year with a $2.5 million outstanding balance, so we're nearing resolution with just a number of cars left in the liquidation process."

— Brian Sohocki, Chief Credit Officer

- Charge-off guidance: 25-30 basis points going forward

- Reserve philosophy unchanged: Comfortable at 1.32%, slightly ahead of peers

Philadelphia Loan Sale

Management confirmed this is a one-off strategic exit, not a recurring credit cleanup:

"Philadelphia is a great market. It's also very competitive, and... the investment to really compete the way we would like would be too great. That money can be used in other markets for producers, physical locations, where we already have really good presence."

— Mike McCuen, Chief Lending Officer

- $225M portfolio designated held-for-sale

- Proceeds to be reinvested in securities at ~4.5% (1.5% rate differential)

- Ancillary benefits: improved liquidity and capital ratios

Loan Growth Outlook

"We feel good about our commercial pipelines, commercial real estate and elsewhere. Our construction portfolio... is going to build and add probably $20+ million of drawdowns a month."

— Mike Price, CEO

- 2026 loan growth guidance: Mid-single digits

- Commercial real estate spreads compressed due to agency/insurance market competition

- Construction portfolio up ~$120M over the past year

Capital Deployment

On buyback activity:

"We intend to use the authority and be fairly aggressive with it overall, but there's still a price sensitivity to it."

— Jim Reske, CFO

- $22.7M remaining under prior program + $25M new authorization

- Capacity of ~$25-30M per quarter, subject to price sensitivity

- Generating far more capital than needed to fund mid-single-digit loan growth

Deposit Strategy

"We're probably two-thirds of our peers in terms of the deposit beta over the last year... We've done that on purpose, we've really kept them a little higher than we could because we wanted the growth."

— Jim Reske, CFO

- Loan-to-deposit ratio in low 90s after loan sale — room to be less aggressive on deposit pricing

2026 Guidance Summary

Conference Call

First Commonwealth hosted its Q4 2025 earnings call on January 28, 2026 at 2:00 PM ET.

- Webcast: fcbanking.com/InvestorRelations

- Replay: Available approximately one hour after conclusion

- View Full Transcript

Data sourced from First Commonwealth Financial Corporation 8-K filed January 28, 2026 and Q4 2025 earnings call transcript. Stock data from market feeds. Estimates from S&P Global.