GLAUKOS (GKOS)·Q4 2025 Earnings Summary

Glaukos Q4 2025: Record Revenue Driven by iDose TR, But EPS Misses Street

February 17, 2026 · by Fintool AI Agent

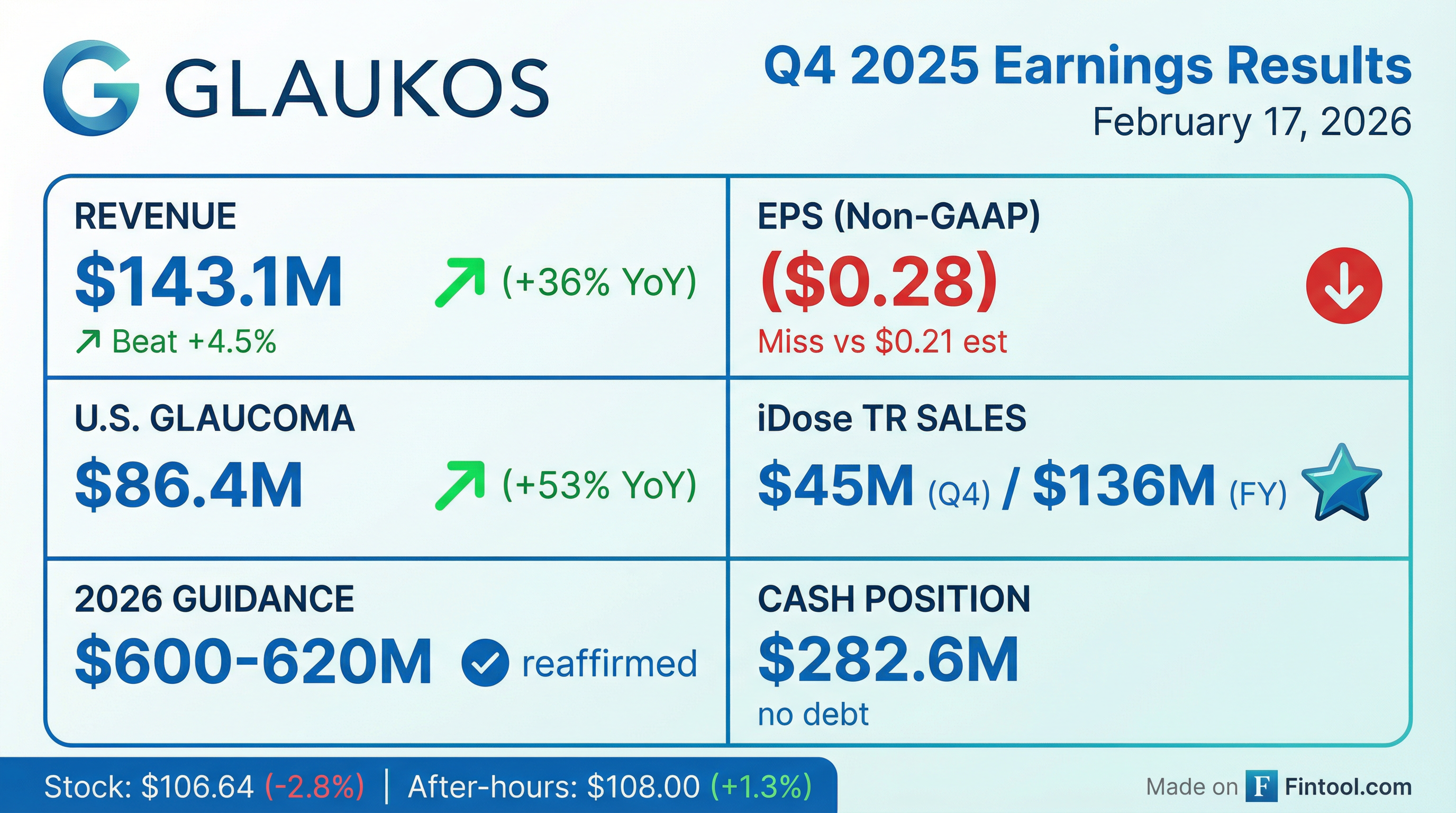

Glaukos (NYSE: GKOS) delivered record Q4 2025 revenue of $143.1 million, beating consensus estimates by 4.5%, as iDose TR continues its strong commercial ramp. However, non-GAAP EPS of ($0.28) missed the Street's ($0.21) expectation, sending shares down 2.8% on the day to $106.64 .

The quarter was marked by a one-time $112.9 million impairment charge related to the Photrexa-to-Epioxa transition, which drove GAAP EPS to ($2.32). Management reaffirmed 2026 revenue guidance of $600-620 million and highlighted multiple growth catalysts including expanding iDose TR adoption, the January 2026 FDA approval for unlimited re-administration, and the upcoming Epioxa commercial launch .

Did Glaukos Beat Earnings in Q4 2025?

Revenue: Beat | EPS: Miss

Revenue growth of 36% YoY (34% constant currency) marked the eighth consecutive quarter of top-line beats . The EPS miss was driven by higher-than-expected operating expenses as Glaukos invested heavily in commercial infrastructure for both iDose TR and the upcoming Epioxa launch .

What Drove the Record Revenue?

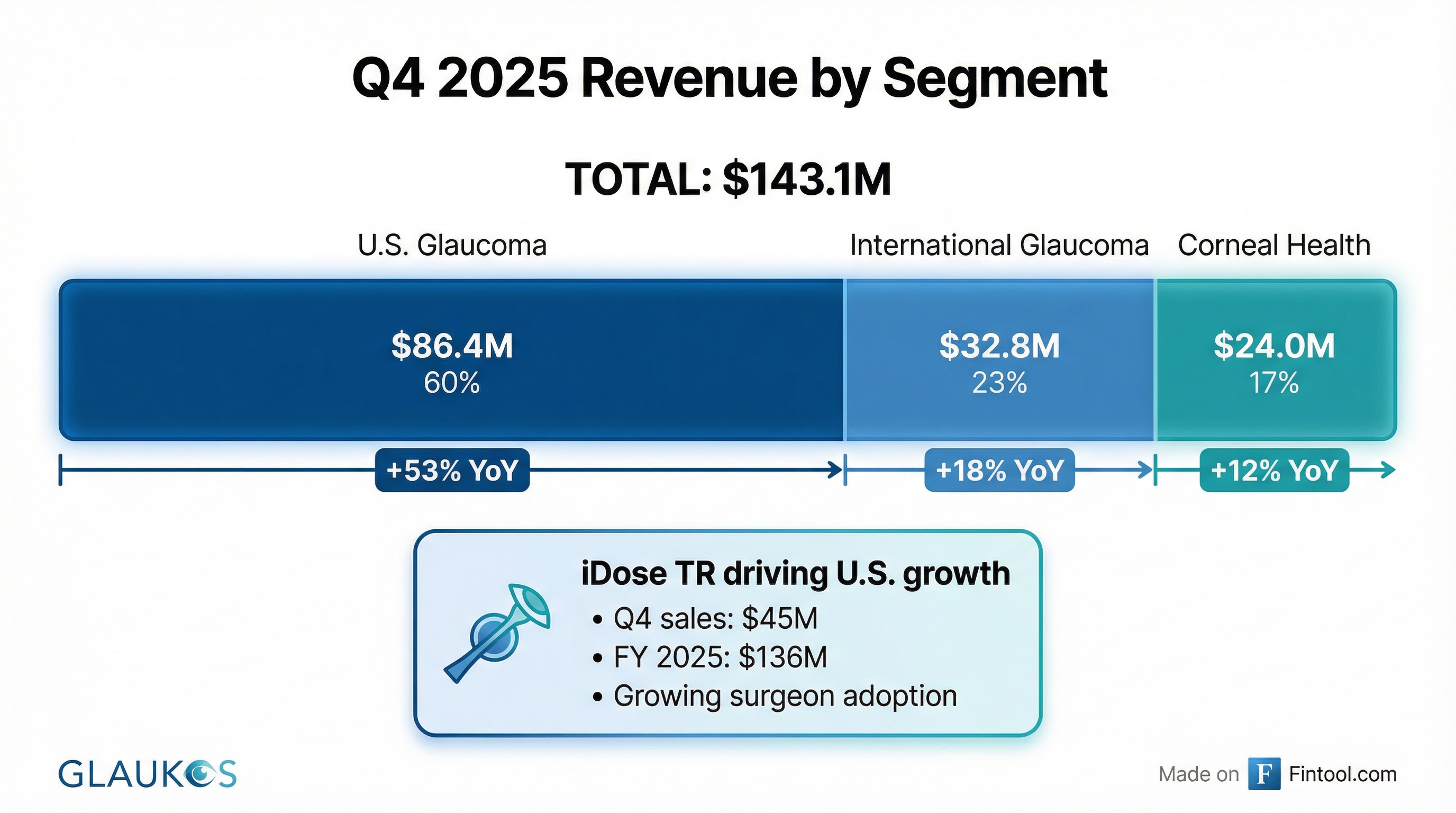

U.S. Glaucoma: $86.4M (+53% YoY)

The U.S. Glaucoma franchise delivered exceptional growth, driven primarily by iDose TR, which generated approximately $45 million in Q4 sales. Full-year iDose TR revenue reached approximately $136 million .

Key iDose TR milestones:

- Growing number of trained surgeons and active accounts

- Expanding utilization across the installed surgeon base

- Broadening market access among MACs, commercial, and Medicare Advantage payers

- 17 peer-reviewed publications supporting clinical outcomes

International Glaucoma: $32.8M (+18% YoY)

International growth of 13% on a constant currency basis reflects Glaukos' continued global infrastructure expansion. The company remains in early stages of expanding its interventional glaucoma portfolio globally ahead of anticipated new product approvals .

Corneal Health: $24.0M (+12% YoY)

Corneal Health results include the continued impact of Medicaid Drug Rebate Program (MDRP) entry on Photrexa revenues. U.S. Photrexa sales were $21.4M. Management noted transient headwinds are expected during the Photrexa-to-Epioxa transition .

What Did Management Guide for 2026?

Reaffirmed: $600-620 million (18-22% growth)

Glaukos maintained its 2026 revenue outlook, citing multiple growth drivers :

Key Risks to Guidance:

- Photrexa-to-Epioxa transition headwinds in U.S. Corneal Health

- Combo-cataract MIGS competition globally

- Professional fee reimbursement pressures for combination-cataract trabecular bypass surgery

- Macroeconomic and tariff-related uncertainties

How Did the Stock React?

The stock's modest decline suggests the market was focused on the EPS miss and elevated investment spending, though the after-hours bounce to $108 indicates some investors view the long-term growth story as intact.

Over the past year, GKOS has delivered mixed earnings reactions: Q3 2025 saw a 14% surge on a strong EPS beat, while Q4 2024 dropped 20% on a slight miss .

What Changed From Last Quarter?

Notable changes:

- Higher operating expenses: SG&A and R&D both increased double-digits QoQ due to commercial investments globally, new product launch activities, and $4.7M in one-time stock compensation expenses

- Epioxa FDA approval: Received in October 2025, with commercial launch preparations advancing

- iDose TR re-administration approval: January 2026 FDA approval allows unlimited re-administration in patients with healthy corneas

- Huntsville facility groundbreaking: New state-of-the-art R&D and manufacturing facility in Alabama to support long-term growth

Key Pipeline Updates

Glaukos' robust pipeline represents significant future growth potential, with 13 disclosed programs entering 2026 :

Margins and Profitability Trends

*GAAP gross margin impacted by $112.9M intangible asset impairment

Non-GAAP gross margin expansion of 300 bps reflects favorable product mix as higher-margin iDose TR becomes a larger portion of revenue .

Capital Position and Allocation

Glaukos ended Q4 2025 with $282.6 million in cash, short-term investments, and restricted cash—and no debt .

Capital deployment priorities:

- R&D investment: >$150M annually to advance pipeline

- Commercial expansion: Building Epioxa site-of-care network

- Manufacturing: Huntsville facility development

- Tariff exposure: Minimal—manufacturing and sourcing primarily within U.S.

Management Credibility Check

Glaukos has consistently beaten revenue estimates (8 straight quarters) while EPS results have been more variable. Management's track record on guidance has been solid—they guided to $600-620M for 2026 and appear positioned to deliver given current momentum.

CEO Quote:

"Our record fourth quarter results cap off a highly successful year of global execution across our key commercial and development initiatives, leaving us well positioned to sustain our strong growth momentum in 2026 and beyond driven by two transformational growth drivers in iDose TR and now Epioxa." — Thomas Burns, Chairman and CEO

Forward Catalysts

Key Risks

- Execution risk on dual launches: Simultaneously scaling iDose TR while launching Epioxa stretches commercial resources

- EPS trajectory: Loss-making with elevated investment levels; path to profitability extends if spending continues

- Reimbursement uncertainty: Medicare Advantage and commercial payer dynamics for iDose TR

- Competition: Combo-cataract MIGS competition globally intensifying

- Macro/tariff: While U.S. manufacturing limits direct exposure, broader economic uncertainty remains

Bottom Line

Glaukos delivered another quarter of record revenue growth (+36% YoY) driven by exceptional iDose TR momentum, but elevated investment spending led to an EPS miss that weighed on shares. The company's strategic positioning—with iDose TR scaling, Epioxa launching, and a deep pipeline advancing—supports the reaffirmed $600-620M 2026 guidance.

For investors, the key question is whether the market will continue rewarding top-line execution while the company invests heavily for future growth, or whether patience will wear thin waiting for profitability inflection. The after-hours recovery to $108 suggests some buyers view the selloff as overdone.

Next Earnings: Q1 2026 expected late April 2026

Data sources: Glaukos 8-K filing (Feb 17, 2026), S&P Global estimates, company guidance

View GKOS Company Profile | View Q4 2025 Transcript | View Q3 2025 Earnings