Earnings summaries and quarterly performance for GLOBE LIFE.

Executive leadership at GLOBE LIFE.

Frank M. Svoboda

Co-Chairman and Chief Executive Officer

J. Matthew Darden

Co-Chairman and Chief Executive Officer

Christopher K. Tyler

Executive Vice President and Chief Information Officer

Dolores L. Skarjune

Executive Vice President and Chief Administrative Officer

Jennifer A. Haworth

Executive Vice President and Chief Marketing Officer

Michael C. Majors

Executive Vice President, Policy Acquisition and Chief Strategy Officer

R. Brian Mitchell

Executive Vice President, General Counsel and Chief Risk Officer

Rebecca E. Zorn

Executive Vice President and Chief Talent Officer

Robert E. Hensley

Executive Vice President and Chief Investment Officer

Thomas P. Kalmbach

Executive Vice President and Chief Financial Officer

Board of directors at GLOBE LIFE.

Alice S. Cho

Director

Cheryl D. Alston

Director

David A. Rodriguez

Director

James P. Brannen

Director

Linda L. Addison

Lead Independent Director

Marilyn A. Alexander

Director

Mark A. Blinn

Director

Mary E. Thigpen

Director

Matthew J. Adams

Director

Philip M. Jacobs

Director

Research analysts who have asked questions during GLOBE LIFE earnings calls.

Andrew Kligerman

TD Cowen

10 questions for GL

John Barnidge

Piper Sandler

10 questions for GL

Elyse Greenspan

Wells Fargo

8 questions for GL

Suneet Kamath

Jefferies

8 questions for GL

Thomas Gallagher

Evercore

8 questions for GL

Wesley Carmichael

Autonomous Research

8 questions for GL

Jimmy Bhullar

JPMorgan Chase & Co.

7 questions for GL

Ryan Krueger

KBW

7 questions for GL

Jack Matten

BMO Capital Markets

5 questions for GL

Mark Hughes

Truist Securities

5 questions for GL

Wilma Burdis

Raymond James Financial

5 questions for GL

Jamminder Bhullar

JPMorgan Chase & Co.

3 questions for GL

Wilma Jackson Burdis

Raymond James

3 questions for GL

Francis Matten

BMO Capital Markets

2 questions for GL

Jeff Schmitt

William Blair & Company, L.L.C.

2 questions for GL

Joel Hurwitz

Dowling & Partners Securities, LLC

2 questions for GL

Maxwell Fritscher

Truist Financial Corporation

2 questions for GL

Wes Carmichael

Wells Fargo & Company

2 questions for GL

Recent press releases and 8-K filings for GL.

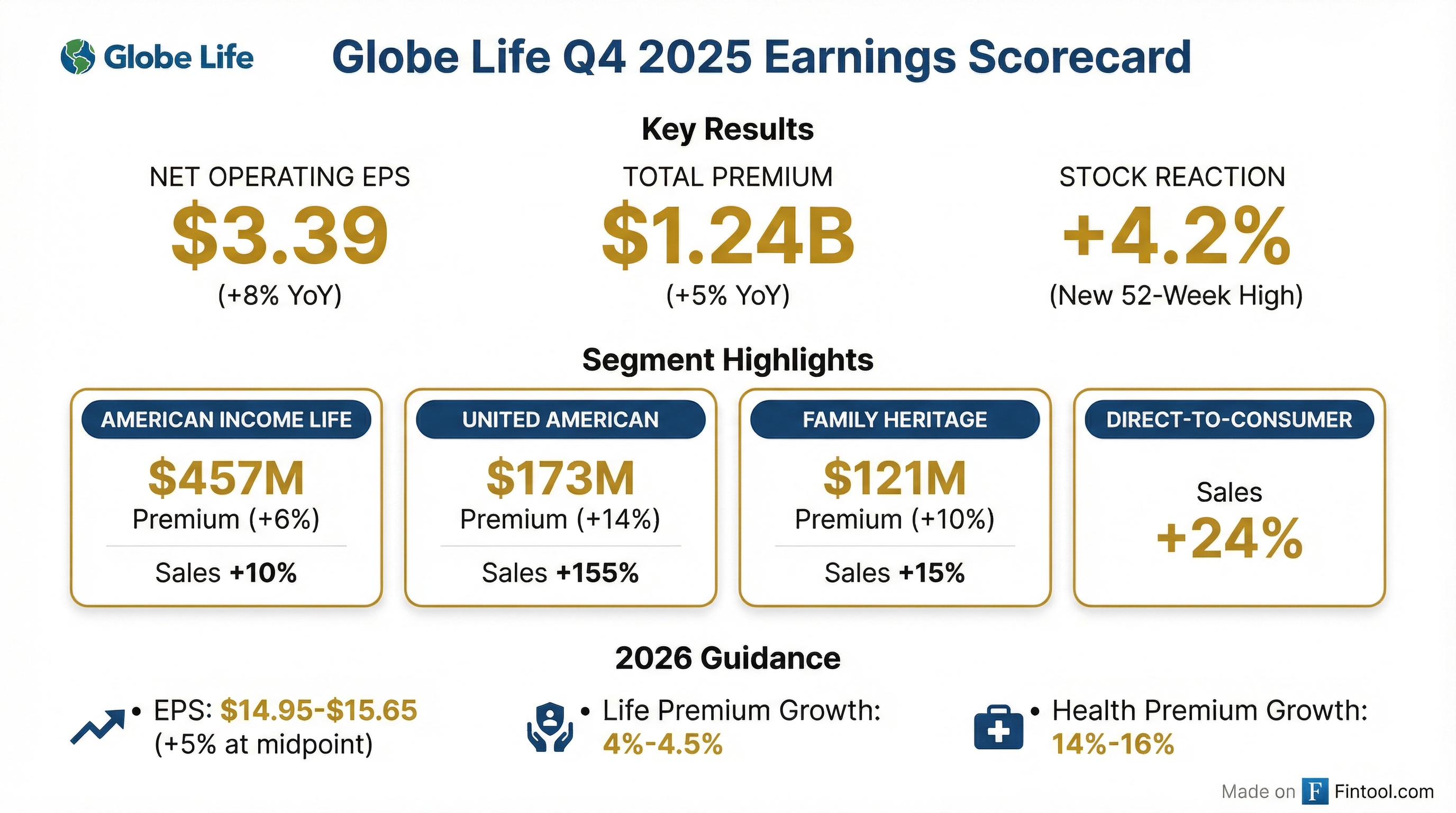

- In Q4 2025, net income was $266 million ($3.29 per share) and net operating income was $274 million ($3.39 per share), up 8% YoY; full-year net operating income was $14.52 per share, GAAP ROE 20.9% (16% ex-AOCI), and book value per share $96.16 ex-AOCI (+11% YoY).

- Fourth-quarter total premium revenue grew 5%, with life premiums of $850 million (+3%) and life underwriting margin $350 million (+4%), and health premiums of $392 million (+9%) and health underwriting margin $99 million (+9%).

- 2026 guidance: total premium growth of 7–8% (life 4–4.5%, health 14–16%), underwriting margins of 41.5–44.5% (life) and 23–27% (health), and net operating EPS of $14.95–$15.65 (+5% at midpoint).

- Net investment income was $281 million (flat) and excess investment income $31 million (down $8 million); invested assets totaled $21.7 billion with a 5.4% yield. 2026 planned investments: $900 M–$1.1 B in fixed maturities (avg. 5.9–6.0%) and $300 M–$400 M in non-fixed maturities (7–9%) for a blended 5.4–5.5% yield.

- In 2025, Globe Life repurchased 5.4 million shares for $685 million, parent excess cash flow was $620 million, with 2026 projections of $625–675 million (dividends $85–90 million; buybacks $535–585 million); also formed Globe Life Re Ltd. and reinsured $1.2 billion of reserves to Bermuda.

- Globe Life reported Q4 2025 net income of $266 million ($3.29/share) and net operating income of $274 million ($3.39/share); full-year 2025 ROE was 20.9% with book value per share of $74.17 (ex-AOCI $96.16).

- Total Q4 premium revenue grew 5%, with life premiums of $850 million (+3%) and a life underwriting margin of $350 million (+4%), and health premiums of $392 million (+9%) with a health underwriting margin of $99 million (+9%).

- 2026 guidance includes net operating EPS of $14.95–$15.65 (5% growth at midpoint); total premium growth of 7–8% (life 4–4.5%, health 14–16%); and expected underwriting margins of 41.5–44.5% (life) and 23–27% (health).

- Returned approximately $770 million to shareholders in 2025 via 5.4 million share repurchases (costing $685 million) and $85 million in dividends; Q4 buybacks were 1.3 million shares for $170 million.

- In Q4 the company generated $266 M in net income ( $3.29 EPS vs. $255 M or $3.01 EPS a year ago) and $274 M net operating income ( $3.39 EPS, +8% YoY); FY 2025 net operating income was $14.52 per share, GAAP ROE 20.9%, book value $74.17 per share.

- Insurance operations saw Q4 life premiums of $850 M (+3%) with life underwriting margin of $350 M (+4%), and Q4 health premiums of $392 M (+9%) with health underwriting margin of $99 M (+9%); 2026 guidance calls for 7–8% total premium growth (life 4–4.5%, health 14–16%) with margins of 41.5–44.5% (life) and 23–27% (health).

- Investment income in Q4 was $281 M (flat YoY) with $31 M excess investment income (down $8 M); fixed maturities yielded 5.29%, blended earned yield 5.4%, and invested assets totaled $21.7 B; 2026 net investment income is expected to grow 3–4%, required interest ~4%, and excess investment income flat.

- The parent repurchased 1.3 M shares for $170 M in Q4 and 5.4 M shares for $685 M in 2025, paid $85 M in dividends, returning $770 M to shareholders; ended 2025 with $80 M in liquid assets; 2026 excess cash flow is guided to $625–675 M, primarily for dividends ($85–90 M) and buybacks.

- For 2026 the company forecasts $14.95–$15.65 net operating EPS (≈5% growth) and normalized EPS growth of ~10%.

- In Q4 2025, Globe Life reported $3.29 per diluted share in net income (up from $3.01) and for the full year achieved $14.07 per diluted share in net income and $14.52 in net operating income, both up 8% YoY.

- The company repurchased 1.3 million shares in Q4 for $170 million (average $134.44), totaling 5.4 million shares for $685 million in 2025.

- For 2026, Globe Life increased its guidance to $14.95–$15.65 per diluted share in net operating income.

- Globe Life delivered Q4 net operating income of $3.39 per diluted share (up 8% y/y) and net income of $3.29 per diluted share (up 9% y/y).

- For full-year 2025, net operating income was $14.52 and net income was $14.07 per diluted share (both up 8%), with ROE of 20.9%.

- Q4 insurance underwriting income rose 6% to $359.7 million on total premium revenue of $1.242 billion (up 5%) driven by higher life and health sales.

- The company repurchased 1.3 million shares for $170 million in Q4 (5.4 million shares for $685 million in 2025) and is guiding 2026 net operating income of $14.95–$15.65 per diluted share.

- Globe Life Re Ltd. has been formed and licensed as a Bermuda Class C insurer to provide reinsurance support for Globe Life’s affiliate entities.

- The new affiliate will underwrite affiliated quota share reinsurance, assuming a proportional share of risk on specified insurance policies.

- Globe Life Re Ltd. has executed its first reinsurance transaction in line with its business plan.

- Globe Life Inc. is headquartered in McKinney, TX, employs over 16,000 agents and 3,600 corporate staff, and has more than 17 million policies in force.

- AM Best affirmed the Financial Strength Rating of A (Excellent) and Long-Term Issuer Credit Rating of A+ (Excellent) for Globe Life’s life/health subsidiaries, and BBB+ (Good) for Globe Life Inc., all with a stable outlook.

- The affirmations reflect Globe Life’s strong balance sheet, very strong operating performance, favorable business profile, and robust enterprise risk management framework.

- On a statutory basis, year-end 2024 capital and surplus increased, and investment income exceeded $1 billion, driven by improved bond net yields.

- Key debt ratings affirmed include BBB+ on $550 million 4.55% senior unsecured notes due 2028 and $400 million 2.15% notes due 2030, among other senior and subordinated instruments.

- Globe Life delivered $4.73 net income per diluted share (YoY +38%) and $4.81 net operating income per share (YoY +38%) for Q3 2025.

- Life underwriting margin rose 24% to $481.6 M and health underwriting margin increased 25% to $108.4 M in Q3 2025.

- Divisional performance included +5% life premiums at American Income Life & Liberty National, +13% health net sales and +10% health premiums at Family Heritage, and +13% life net sales at Direct to Consumer.

- Repurchased 840,242 shares at a total cost of $113 M, and raised 2025 net operating income per share guidance to $14.40–$14.60 (2026: $14.60–$15.30).

- The U.S. Attorney’s Office for the Western District of Pennsylvania has closed its investigation into Globe Life and American Income Life, with no enforcement action to be taken.

- The probe stemmed from subpoenas concerning sales practices by independent agents selling AIL policies.

- Globe Life, headquartered in McKinney, TX, employs 16,000 insurance agents, 3,600 corporate staff, and has over 17 million policies in force.

- Globe Life posted net operating income of $271 million ($3.27/share), a 10% increase year-over-year, and GAAP net income of $253 million ($3.50/share), with GAAP ROE of 18.8% and ex-AOCI ROE of 14.4% as of June 30.

- Q2 life premium revenue grew 3% to $840 million with a 6% rise in life underwriting margin to $340 million, while health premium revenue rose 8% to $378 million but health underwriting margin declined 2% to $98 million; full-year guidance: life premium +3.5%, life margin 43–45% of premium, health premium +8–9%, health margin 25–27% of premium.

- Distribution remains strong: average total agent count increased 6% sequentially to 17,621 agents, underpinned by robust recruiting and onboarding across exclusive agencies.

- Capital return: repurchased 1.9 million shares for $226 million at an average price of $121.13 and paid $22 million in dividends in Q2, totaling ~$250 million returned; full-year plan includes $600–650 million in buybacks and $80–90 million in dividends; parent liquidity ended Q2 at $105 million, and a $500 million 30-year contingent capital facility was secured.

- Submitted preliminary plan to Bermuda Monetary Authority to launch a reinsurance affiliate by year-end, aiming to cede up to 25% of statutory life reserves over time, with potential to unlock incremental annual cash flow of $200 million by 2027.

Quarterly earnings call transcripts for GLOBE LIFE.

Ask Fintool AI Agent

Get instant answers from SEC filings, earnings calls & more