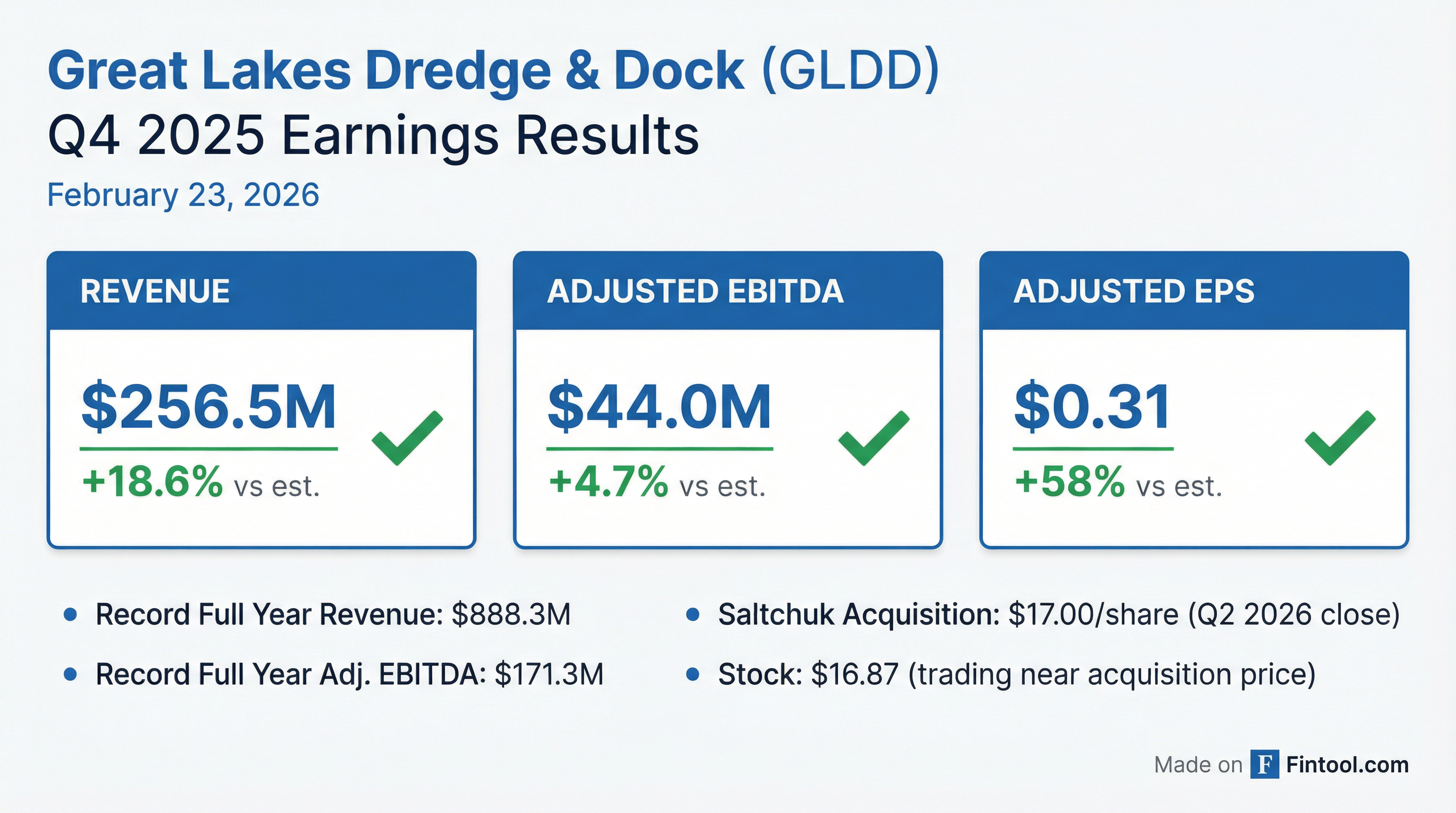

Great Lakes Dredge & Dock (GLDD)·Q4 2025 Earnings Summary

Great Lakes Dredge Beats Q4 on All Metrics as Saltchuk Deal Nears Close

February 23, 2026 · by Fintool AI Agent

Great Lakes Dredge & Dock (NASDAQ: GLDD) delivered a strong beat on all metrics in Q4 2025, capping a record-breaking year for the largest U.S. dredging services provider. Revenue of $256.5 million crushed consensus by 18.6%, while adjusted EPS of $0.31 exceeded expectations by 56%. The company also announced two new international offshore energy contracts that will keep its Acadia vessel utilized through 2027.

This marks the final quarterly report before the expected Q2 2026 close of Saltchuk Resources' $1.5 billion acquisition of the company at $17.00 per share.

Did Great Lakes Dredge Beat Earnings?

Yes — decisively on all metrics. Q4 2025 represented one of GLDD's strongest quarterly performances:

GAAP net income was $12.6 million, lower than adjusted due to an $8.1 million one-time charge (net of tax) from the extinguishment of second lien notes. Excluding this charge, the quarter showed significant improvement.

Full Year 2025 also set records:

The full year beat consensus on revenue by 4.7% ($888.3M vs $848.2M estimate) and adjusted EBITDA by 1.2% ($171.3M vs $169.3M estimate).

What Drove the Revenue Beat?

Q4 revenue increased $53.7 million (+26.5%) year-over-year from Q4 2024's $202.8 million. Key drivers:

- Amelia Island hopper dredge — First full quarter of utilization after August 2025 delivery

- Higher capital and offshore energy revenue — Major port deepening projects plus offshore wind rock installation work

- Strong project execution — Continued momentum from complex port deepening and coastal restoration projects

Full Year Revenue by Segment:

Offshore energy is a new revenue stream for GLDD, contributing $30.2 million in its first year. This segment supports offshore wind development with rock installation services for subsea infrastructure protection.

What's Happening with the Saltchuk Acquisition?

On February 11, 2026, Great Lakes announced a definitive agreement for Saltchuk Resources to acquire the company in an all-cash transaction:

Key conditions:

- Hart-Scott-Rodino Act waiting period expiration

- Tender of shares representing majority of outstanding common stock

- Customary closing conditions

Upon completion, GLDD will operate as a standalone business within Saltchuk's family of companies, and the stock will no longer be listed on Nasdaq.

No earnings call was hosted due to the pending transaction.

How Did the Stock React?

GLDD closed at $16.87 on February 23, 2026, essentially flat on the earnings release day.

The muted reaction is expected given the stock is trading just below the $17.00 acquisition price, with limited upside beyond deal certainty. Key price milestones:

Total return since Jan 2024: +121% — GLDD shareholders have seen exceptional appreciation, culminating in the acquisition premium.

What's in the Backlog?

Backlog declined year-over-year but remains robust with strong offshore energy growth:

The dredging backlog decline reflects the completion of a major port deepening cycle that drove 2023-2025 performance. Management previously guided that the next wave of port deepening projects (New York/New Jersey, Tampa, New Haven, Baltimore) would commence in 2027.

Offshore energy is the growth story. The company announced two new international contracts with a major offshore wind developer that will keep the Acadia vessel utilized in Europe for the majority of 2027.

Additional pending awards and options total ~$203 million ($200.2M dredging + $2.9M offshore energy), not included in backlog.

What Changed From Last Quarter?

Q3 2025 → Q4 2025 comparison:

Revenue surge driven by full utilization of Amelia Island and higher offshore energy activity. Margin compression was expected due to increased drydocking expenses during Q4.

Key developments since Q3:

- Saltchuk acquisition announced (Feb 11, 2026)

- Two new international offshore energy contracts secured

- Acadia delivery remains on track for Q1 2026

Balance Sheet Position

The company enters the acquisition with a clean balance sheet:

In October 2025, the company refinanced its revolver, increasing capacity to $430 million and extending maturity to 2030. It also repaid the $100 million second lien term loan, reducing annual interest expense by ~$6 million.

Capital Expenditures

Full year 2025 CapEx totaled $143.9 million:

- Acadia construction: $69.1M

- Amelia Island completion: $32.3M

- Support equipment: $13.7M

- Maintenance and growth: $28.8M

With the newbuild program substantially complete, CapEx is expected to normalize significantly in 2026 and beyond.

Key Takeaways

-

Strong finish to a record year — Q4 beat on revenue (+18.6%), EBITDA (+4.7%), and EPS (+56%). Full year 2025 set records for revenue ($888.3M) and adjusted EBITDA ($171.3M).

-

Acquisition on track — Saltchuk's $17/share deal expected to close Q2 2026. Stock trading at $16.87 reflects deal certainty with minimal spread.

-

Offshore energy emerging — New segment contributed $30M in year one. Two new international contracts extend Acadia utilization through 2027.

-

Backlog transition — Dredging backlog down 36% as port deepening cycle completes, but offshore energy backlog up 178%. Next wave of port projects expected in 2027.

-

No earnings call — Due to pending acquisition, management did not provide forward guidance or take Q&A.