GENUINE PARTS (GPC)·Q4 2025 Earnings Summary

Genuine Parts Misses Q4 Estimates, Stock Drops 7% as Company Announces Historic Spinoff

February 17, 2026 · by Fintool AI Agent

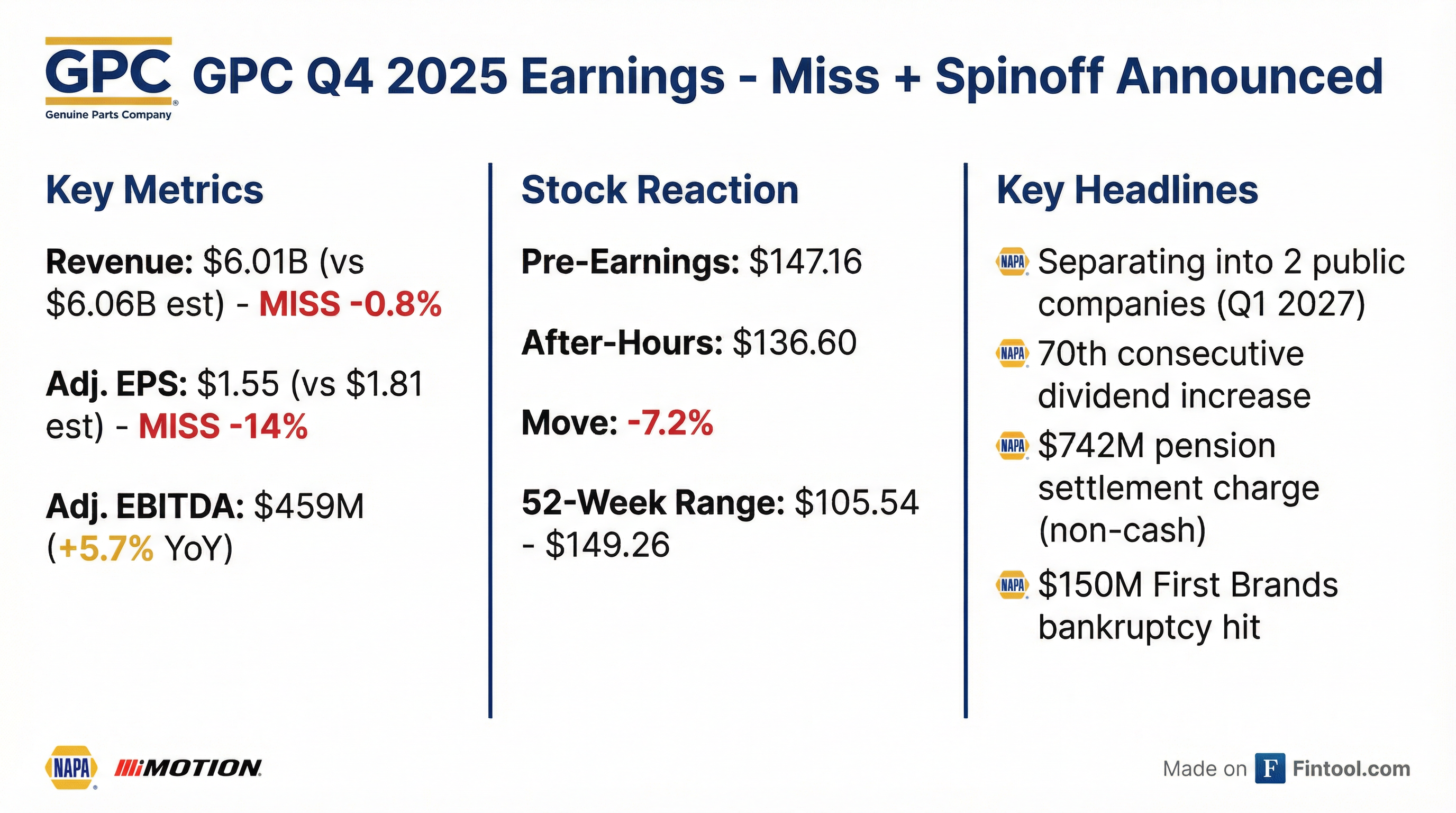

Genuine Parts Company (NYSE: GPC) reported Q4 2025 results that missed Wall Street expectations on both revenue and earnings, sending shares down over 7% in after-hours trading. The miss was compounded by several one-time charges, though the bigger story is the company's announcement to separate its Automotive and Industrial businesses into two independent public companies.

Did Genuine Parts Beat Earnings?

No. GPC missed on both metrics for the second consecutive quarter:

The GAAP numbers looked far worse due to multiple one-time charges: the company reported a net loss of $609 million ($4.39 per share) driven by a $742 million pension settlement charge, $150 million credit loss from the First Brands bankruptcy, and $103 million asbestos liability remeasurement.

How Did the Stock React?

GPC shares fell sharply after the earnings release:

The decline erases most of the stock's recent rally — shares had climbed from under $130 in late October to near all-time highs ahead of earnings. The double miss plus conservative 2026 guidance appears to have disappointed investors hoping for stronger execution.

What Changed This Quarter?

The big news: GPC is splitting up. The company announced its intention to separate into two independent, publicly traded companies:

1. Global Automotive (NAPA brand)

- Revenue: $15.4B annually

- EBITDA: $1.2B (8.0% margin)

- 10,000+ locations across North America, Europe, and Australasia

- Largest global automotive aftermarket network

- Targeting continued margin expansion through technology and supply chain investments

2. Global Industrial (Motion brand)

- Revenue: $8.9B annually

- EBITDA: $1.15B (12.9% margin)

- Market-leading industrial distributor

- Focus on mission-critical MRO and automation

- Positioned for reshoring and AI infrastructure tailwinds

The separation is targeted for completion in Q1 2027 and is expected to be tax-free for shareholders. The company will host separate investor days in H2 2026 for each business.

CEO Will Stengel explained the rationale: "Creating two focused, independent companies sharpens customer and market alignment, increases clarity and speed, simplifies operations and enables disciplined, business-specific investments to unlock long-term value."

How Did the Segments Perform?

Industrial was the clear winner, while Automotive struggled with margin compression:

Industrial highlights:

- Grew in excess of the market despite sluggish manufacturing economy

- E-Commerce represented ~45% of sales, up 800+ bps from 2024

- MRO business grew 3%+ with strength in both local and corporate accounts

Automotive challenges:

- North America margins compressed due to cost inflation and competitive pressures

- Europe saw negative comp sales (-3.1%) amid soft market conditions

- U.S. company-owned stores showed relative strength (+4% comp sales)

- Independent owner purchases down ~1% for the year; Q4 comp sales to independents were flat (down from 1% growth in Q3)

What Did Management Guide?

2026 guidance came in slightly below consensus expectations:

Segment-level guidance:

The midpoint of EPS guidance ($7.75) implies 5% growth — a modest recovery but below the double-digit growth some investors had hoped for given the restructuring benefits and spinoff announcement.

Key assumptions behind guidance:

- Flat underlying market growth (not planning for acceleration even with positive January PMI reading)

- ~2% pricing benefit including tariffs

- 40-60 bps gross margin expansion from sourcing and pricing initiatives

- $100M-$125M benefit from ongoing transformation activities (split between automotive and industrial)

- SG&A deleverage of 30-50 bps due to persistent cost inflation (wages, healthcare up high single digits)

What About Capital Allocation?

GPC extended its dividend streak to 70 consecutive years of increases:

- 2026 annual dividend: $4.25/share (+3.2% from $4.12)

- Quarterly dividend: $1.0625/share

- Dividend yield: ~3.1% (at $136.60 after-hours price)

Other capital deployment:

- 2025 CapEx: $470M (guiding $450-500M for 2026)

- 2025 M&A: $318M deployed (guiding $300-350M for 2026)

- ~7.5 million shares remain available for repurchase

What Transformation Initiatives Are Underway?

Management provided detailed commentary on ongoing transformation programs:

NAPA Supply Chain: Major investments in U.S. supply chain modernization, including new distribution centers in the UK, France, Germany, and Spain. These investments position the business for when European markets recover.

Sales Effectiveness: Initiatives at both NAPA and Motion focused on partnership with independent owners and company-owned store optimization. The company noted significant improvement in payroll efficiency at company-owned stores.

Technology: Investments in back office productivity, store technology, catalog and search improvements, and in-facility automation. IT investments are moving to cloud-based technology, which shifts costs from CapEx to SG&A.

Commercial Capabilities at Motion: Enhanced pricing tools and capabilities to be "smarter and sharper" on pricing.

The expected benefit from these transformation activities is $100M-$125M in 2026, with associated expenses of $225M-$250M. The benefits flow through both gross margin and SG&A productivity.

What Were the One-Time Charges?

Q4 2025 included an unusually high level of special items:

These items totaled $1.11 billion pre-tax in Q4 alone, explaining the stark difference between GAAP loss of $4.39/share and adjusted EPS of $1.55.

What Did Analysts Ask About?

Key themes from the Q&A session:

On North America Automotive margins (Scott Ciccarelli, Truist): CFO Bert Nappier attributed the 110 bps margin decline to wage pressure, US healthcare costs (up $32M for the year, $20M above expectations), rent, freight, and IT investments as they modernize cloud-based technology.

On company-owned vs independent stores: The stores are split 65% independent / 35% company-owned by count, with sales roughly 50/50. CEO Will Stengel noted company-owned stores had their best payroll percentage "ever" in Q4, with significant operational improvements.

On European performance (Brett Jordan, Jefferies): Particular weakness in UK, France, and Germany — the three largest markets. However, Spain and Portugal are bright spots where NAPA brand expansion has "essentially doubled that business" and "essentially doubled the EBITDA rate."

On 2026 inflation outlook (Greg Melich, Evercore): Management expects 2% total inflation for the year, with about half from tariffs. CFO noted tariff dynamics have "largely moderated" and commercial discussions with suppliers are back to "ordinary course."

On shape of the year (Chris Dankert, Loop Capital): Earnings growth expected to accelerate sequentially through 2026, with first half more muted due to European market conditions and prudent assumptions on independent owners. Interest expense headwind weighted more in H1.

On product categories (Kate McShane, Goldman Sachs): Non-discretionary repair grew mid-single digits in Q4, maintenance and service went from low to mid-single digits through the year, and discretionary went from flat to slightly positive. Combined, non-discretionary categories account for ~85% of U.S. automotive business.

What Are the Key Risks?

Execution risks from the spinoff:

- Management distraction during 12-month separation process

- Potential dis-synergies from splitting shared services

- Need to establish investment-grade credit at both entities

Automotive headwinds:

- Margin pressure in North America (-110 bps in Q4)

- Weak European market conditions (comp sales -3.1%)

- First Brands bankruptcy removes a key supplier

- Independent owners facing persistent cost inflation and elevated interest rates

Industrial exposure:

- Manufacturing economy remains sluggish

- End market growth only in 7 of 14 markets (vs 4 in 2024)

- January PMI above 50 for first time since February 2025 — encouraging but "one month doesn't make a trend"

What's the Investment Thesis Now?

Bull case:

- Spinoff could unlock significant value — sum-of-parts analysis suggests upside

- Industrial business (Motion) commands premium multiples as standalone

- 70-year dividend streak provides income floor

- Automotive transformation investments should drive margin recovery

Bear case:

- Consecutive EPS misses raise execution concerns

- Automotive margins trending wrong direction

- Conservative 2026 guidance suggests limited near-term upside

- Spinoff complexity adds uncertainty

The market's reaction suggests investors need to see cleaner execution before re-rating the stock higher. The spinoff announcement is strategically sound, but the path to value creation requires consistent operational improvement in the Automotive segment.

Full-Year 2025 Results

Related: GPC Company Profile | Q4 2025 Earnings Transcript | Q3 2025 Earnings