HALOZYME THERAPEUTICS (HALO)·Q4 2025 Earnings Summary

Halozyme Q4: Record $1.4B Year But Surf Bio Write-Down Spooks Investors

February 17, 2026 · Updated with Q&A highlights · by Fintool AI Agent

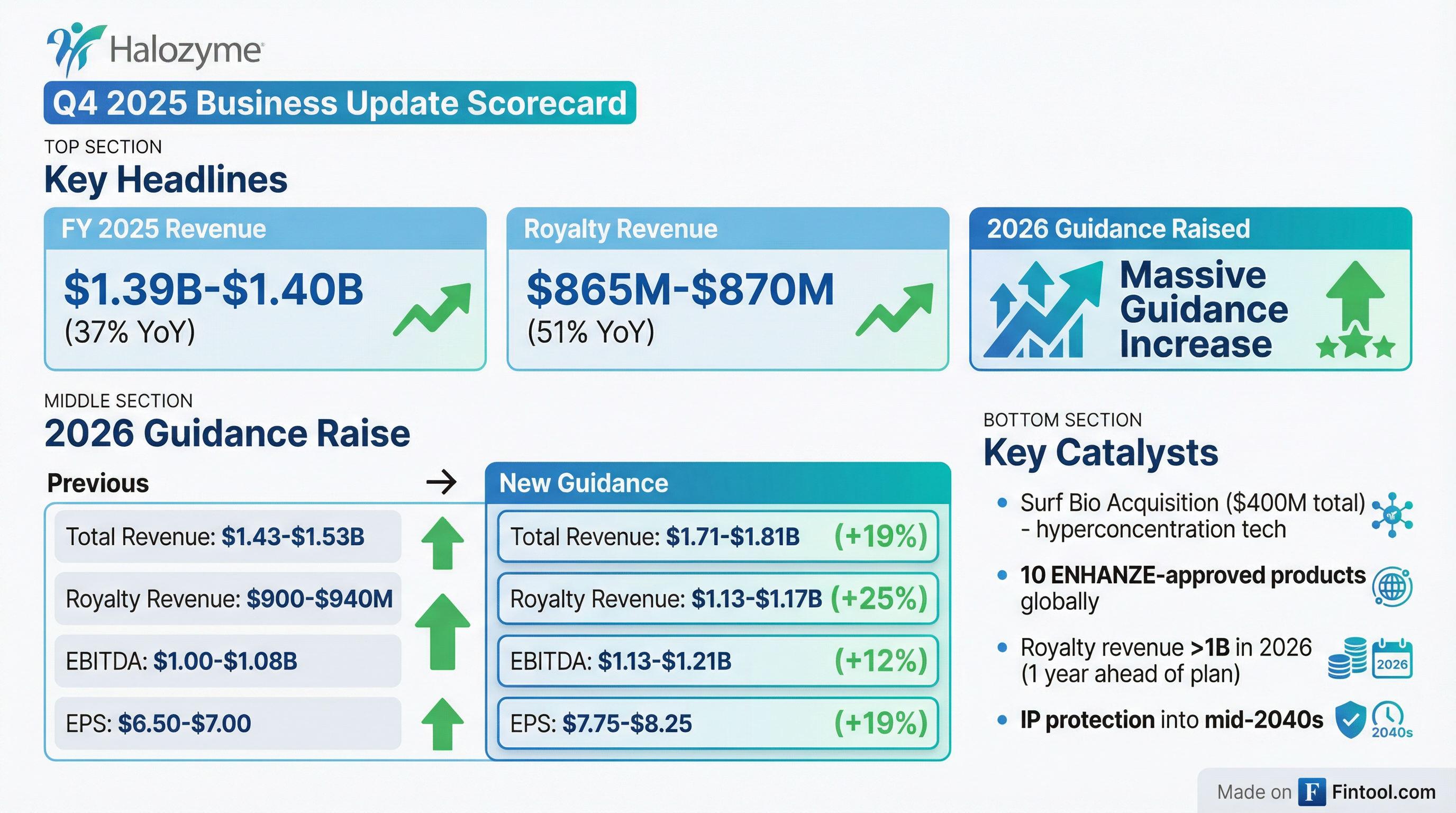

Halozyme Therapeutics (NASDAQ: HALO) reported record full-year 2025 results today, with total revenue reaching $1.397 billion (+38% YoY) and royalty revenue hitting $868 million (+52% YoY) — confirming the preliminary figures shared in January. However, the stock fell ~4% after-hours as investors digested a $285 million acquired IPR&D write-down from the Surf Bio acquisition that drove a Q4 net loss of $142 million.

The headline: Record revenue and royalty momentum, but a messy Q4 from M&A accounting that masked the underlying earnings power.

Did Halozyme Beat Earnings?

Mixed results. Revenue came in essentially in-line while EPS missed due to the Surf Bio IPR&D charge:

*EPS consensus was set before the Surf Bio IPR&D charge was known. Excluding the $2.30/share IPR&D impact, underlying EPS would have been ~$6.45, roughly in-line.

Q4 2025 Quarterly Results

Important context: The Q4 net loss and EBITDA collapse were entirely driven by the $284.9 million acquired IPR&D expense from the Surf Bio acquisition, which represents a Day 1 write-off under GAAP. The SEC requires companies to include IPR&D in Non-GAAP results, so even adjusted metrics took a hit.

Beat/Miss Track Record

Halozyme has consistently beaten estimates, though this quarter's IPR&D charge breaks the EPS streak:

*Values retrieved from S&P Global. Q4 2025 EPS miss due to Surf Bio IPR&D charge.

What's Driving Royalty Growth?

The three blockbuster franchises delivered exceptional 2025 performance:

DARZALEX Subcutaneous (J&J)

DARZALEX is now J&J's largest pharmaceutical product. Management projects sales exceeding $18 billion by 2028.

PHESGO (Roche)

Roche raised its conversion goal from 50% to 60% after surpassing the initial target. Analysts project CHF 3.6B by 2028.

VYVGART Hytrulo (argenx)

The prefilled syringe launch for gMG and CIDP has expanded the prescriber base and accelerated adoption. This is "just the beginning" with multiple expanded indications in development.

Newer Launches ($30B Opportunity)

Four recently launched subcutaneous products represent an approximately $30 billion combined opportunity by 2028:

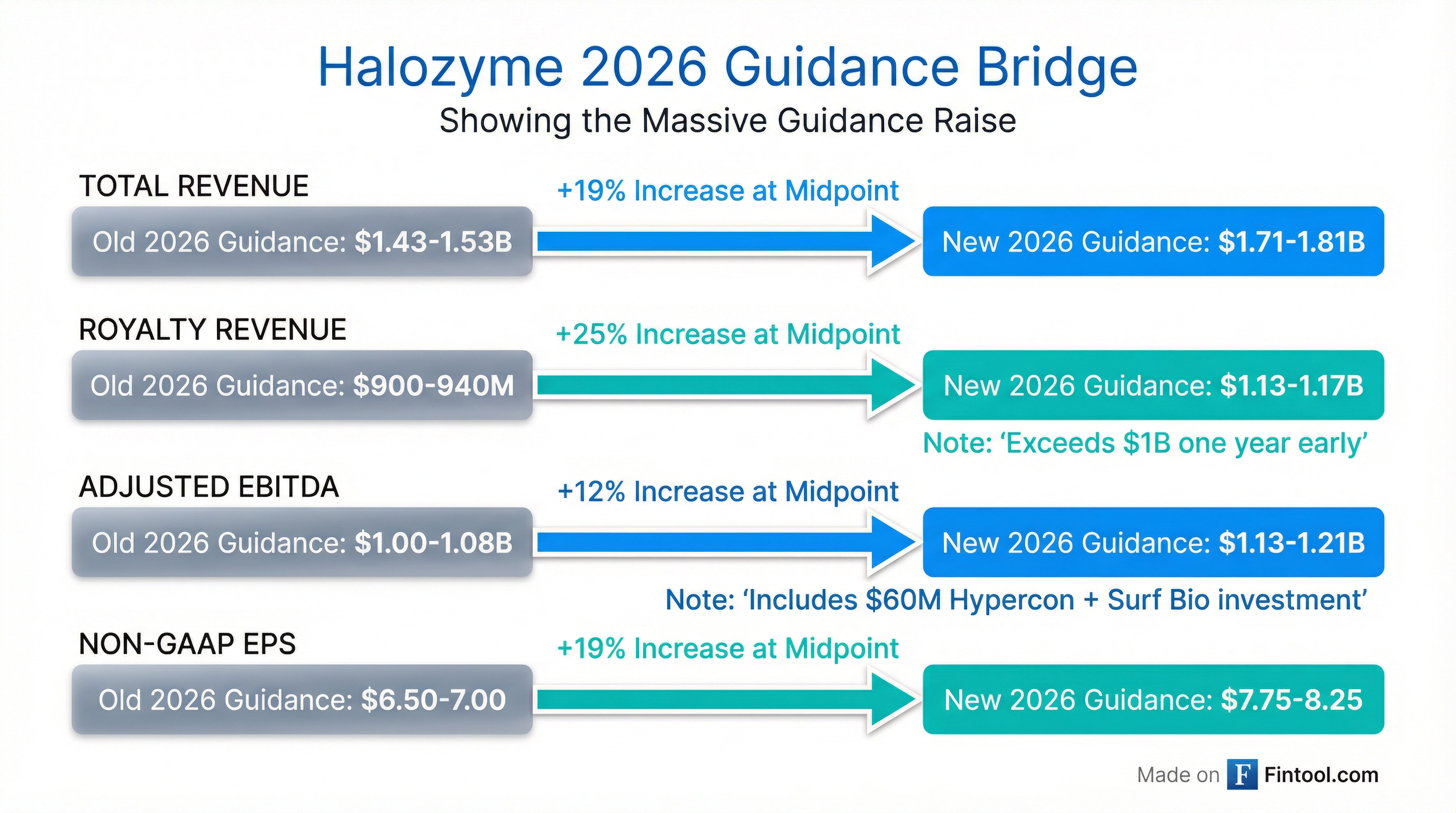

What Did Management Guide for 2026?

Management reiterated the strong 2026 guidance first announced on January 28, signaling confidence in the underlying business despite the Q4 noise:

*FY 2025 EPS includes $2.30 unfavorable IPR&D impact.

2026 Guidance vs. Street Consensus

*Values retrieved from S&P Global

The street is at the high-end of management's EPS guidance range. The key variable: Will royalty revenue accelerate enough to drive operating leverage, or will Hypercon/Surf Bio investments pressure margins?

Royalty revenue exceeding $1 billion in 2026 remains the marquee milestone — one year ahead of the original timeline.

Quarterly Cadence for 2026

Management provided important modeling guidance:

- Q1 royalties expected 5-10% below Q4 2025 due to annual contractual rate resets, with sequential growth thereafter

- No milestones expected in Q1 — milestones weighted to H2 2026

- This means Q1 total revenue will decline sequentially from Q4's $452M

What Changed From Last Quarter?

1. Surf Bio Write-Down ($285M IPR&D Charge)

The Surf Bio acquisition, completed in December 2025 for $300M upfront plus $100M in milestones, triggered a $284.9 million acquired IPR&D charge that hammered Q4 earnings. This is a GAAP requirement for early-stage R&D assets.

What Surf Bio brings:

- Hyperconcentration technology enabling formulations up to 500 mg/mL

- Polymer-based approach for subcutaneous delivery of biologics

- IP protection extending into the mid-2040s

- Meaningfully expands the addressable market beyond ENHANZE

2. German Court Blocks Merck's Keytruda SC

In December 2025, a German court granted Halozyme's request for a preliminary injunction ordering Merck to stop distributing Keytruda SC in Germany. This is significant — it validates Halozyme's patent position and could have broader implications for the Keytruda SC launch in other markets.

3. Elektrofi Acquisition Completed

Halozyme closed the Elektrofi acquisition (Hypercon™ technology) in November 2025, adding microparticle technology that enables hyperconcentration of biologics. Combined with Surf Bio, Halozyme now has three drug delivery platforms with IP extending into the 2040s.

4. Partner Product Approvals Accelerated

Q4 was a banner quarter for partner approvals:

- DARZALEX FASPRO — FDA approved for newly diagnosed multiple myeloma (D-VRd combination)

- DARZALEX FASPRO — FDA approved as single treatment for high-risk smoldering myeloma

- RYBREVANT FASPRO — FDA approved for EGFR-mutated NSCLC

- RYBREVANT — Approved in China and Japan for first-line NSCLC

5. New Partnerships Signed

- Takeda — Global license for vedolizumab (ENTYVIO) SC for inflammatory bowel disease

- Skye Bioscience — ENHANZE license for nimacimab (obesity treatment)

- Merus — ENHANZE license for petosemtamab (head and neck cancer)

- Roche — New undisclosed non-exclusive target nomination

New Growth Vector: ENHANZE for Antibody Drug Conjugates (ADCs)

Chief Scientific Officer Chris Wahl unveiled preclinical data supporting ENHANZE for ADCs — a potentially significant new addressable market. This was the first detailed disclosure of this opportunity.

The ADC Problem

ADCs (antibody + linker + cytotoxic payload) have been difficult to convert to subcutaneous delivery due to:

- Injection site toxicity concerns from cytotoxic payloads

- Dose-limiting adverse events associated with peak blood concentration (Cmax), including interstitial lung disease and cardiac toxicities

Halozyme's Preclinical Results

Testing two approved ADCs with ENHANZE vs. IV and subcutaneous alone:

The Investment Thesis

"The data supports not only the ability to deliver ADCs subcutaneously, but the potential for improvements in the benefit-risk profile." — Dr. Chris Wahl, Chief Scientific Officer

Key implications:

- Higher doses may be possible subcutaneously due to lower Cmax

- Could reduce dose-limiting toxicities (ILD, cardiac)

- Multiple pharma/biotech discussions ongoing

- Regulatory pathway expected to mirror traditional ENHANZE (PK non-inferiority studies for approved ADCs)

This opens ENHANZE to a rapidly growing $15B+ ADC market where conversion to subcutaneous has been limited.

Q&A Highlights

J&J DARZALEX Agreement Extension

The ENHANZE licensing agreement with J&J ends in 2032, but management expects to extend it:

"We absolutely expect to enter into discussions with Johnson & Johnson closer to the time... to extend our agreement and our supply of API. We do not expect J&J to take the risk of going to get another source of API." — Dr. Helen Torley

Hypercon Phase 1 Timing

Two Hypercon programs remain on track for Phase 1 starts in Q4 2026:

- Both are existing blockbuster mechanisms of action (confidential partners)

- Clinical scale-up batches being completed

- IND filings in progress

- Studies expected to be posted on ClinicalTrials.gov when starting

Management projects Hypercon will generate ~$1 billion in royalty revenue within 5 years of first launches (mid-2030s).

Merck/Alteogen Litigation Update

- The IPR filed against Alteogen in December is separate from the Merck district court case

- Discovery ongoing — Halozyme has access to the Merck-Alteogen agreement and Keytruda SC for testing

- Both parties expected before district court in June

- German preliminary injunction remains in effect

Portfolio Expansion Target

Management expects the combined portfolio to nearly double from 19 products today to 36 by 2028 across ENHANZE, Hypercon, and Surf Bio platforms.

Key Management Quotes

"2025 was one of the most significant and value-creating years in Halozyme's history. We showcased our ability to execute across every dimension — strategically, operationally, and financially."

— Dr. Helen Torley, President and CEO

"Together, in hands, our auto-injectors, Hypercon and Surf Bio, position Halozyme as the one-stop shop for the biopharma industry for subcutaneous drug delivery."

— Dr. Helen Torley

"We are building a future that's defined by innovation, durability, and high-margin royalty that extends throughout the next two decades."

— Dr. Helen Torley

Financial Trends

Full Year Revenue Momentum

Quarterly Revenue Trend

Margin Profile (FY 2025 vs FY 2024)

SG&A growth was driven by litigation costs (Merck patent dispute), M&A transaction costs, and diligence expenses.

Balance Sheet Highlights

Key changes:

- Cash declined due to Elektrofi/Surf Bio acquisitions and share repurchases

- Debt increased with $1.5B in new convertible notes (2031 and 2032 maturities)

- Intangible assets nearly tripled from acquisitions

- Revolving credit facility expanded from $575M to $750M

How Did the Stock React?

*Values retrieved from market data

The stock has rallied +69% from its 52-week low but gave back gains after-hours as investors processed the Q4 loss and balance sheet changes from M&A. The after-hours drop of ~4% suggests the market is concerned about the IPR&D charges and cash burn from acquisitions.

Valuation at current levels:

- P/E (2026E): 9.5x (using guidance midpoint of $8.00)

- EV/EBITDA (2026E): 8.4x

- Price/Sales (2026E): 5.4x

Forward Catalysts

Near-Term (2026):

- Q1 2026 earnings (expected May 2026) — clean quarter without IPR&D noise

- 6 new ENHANZE programs and 2 Hypercon programs entering Phase 1

- 1-3 new ENHANZE licensing agreements + 1-2 new Hypercon agreements expected

- Royalty revenue crossing $1 billion milestone

- Keytruda SC litigation: District court appearance in June

Medium-Term (2027-2030):

- ADC partnership announcements — multiple discussions ongoing

- First Hypercon approvals projected 2030-2031

- Portfolio expansion to 36 products by 2028 (from 19 today)

- Surf Bio clinical readiness in late 2027 or 2028

Long-Term:

- IP protection into mid-2040s across all three drug delivery platforms

- Management targets $2 billion+ in total revenue by 2028

- Hypercon projected to generate ~$1 billion in royalties within 5 years of first launches (mid-2030s)

Risks and Concerns

- Balance Sheet Stress: Cash fell to $145M while debt rose to $2.1B; leverage has increased materially

- M&A Integration: $1.15B+ deployed on Elektrofi and Surf Bio requires successful commercialization

- Partner Concentration: DARZALEX, Phesgo, and VYVGART drive majority of royalty growth

- Litigation Costs: Merck patent dispute driving elevated SG&A; June court date pending

- Clinical Risk: Hypercon™ and Surf Bio technologies still need partner clinical validation

- IPR&D Risk: Future acquisitions could trigger similar write-downs

- ADC Opportunity Still Preclinical: ADC data is promising but requires clinical validation and partner commitments

Bottom Line

Halozyme delivered what it promised: record revenue of $1.4 billion (+38%) and royalty revenue of $868 million (+52%). The underlying ENHANZE business is executing flawlessly, with partner approvals accelerating and new partnerships signed. The Keytruda SC injunction in Germany is a significant win.

The big news from this call: Preclinical data supporting ENHANZE for antibody drug conjugates (ADCs) — a potentially significant new addressable market. Lower peak concentrations and strong injection site tolerability could open ENHANZE to the rapidly growing $15B+ ADC market.

However, the Q4 optics were ugly. The $285 million Surf Bio IPR&D charge drove a quarterly net loss. The balance sheet has also stretched — cash is down to $145M while debt has grown to $2.1B.

The bull case: Royalty revenue crosses $1B in 2026, one year early. EBITDA nearly doubles to $1.2B. ADC partnerships could be a major new growth vector. Hypercon projected to add ~$1B in royalties by mid-2030s. At 9.5x forward EPS, the stock is cheap for a high-visibility royalty compounder with 20+ years of IP runway.

The bear case: Leverage concerns mount. M&A execution risk is real. The litigation with Merck is expensive and uncertain. Partner concentration remains a risk. ADC opportunity is still preclinical.

Watch for: Q1 2026 earnings to show a clean quarter without M&A noise, ADC partnership announcements, and the two Hypercon Phase 1 starts in Q4 2026.

Related: