HELIX ENERGY SOLUTIONS GROUP (HLX)·Q4 2025 Earnings Summary

Helix Energy Solutions Crushes Q4 as Free Cash Flow Surges, Stock Hits 52-Week High

February 24, 2026 · by Fintool AI Agent

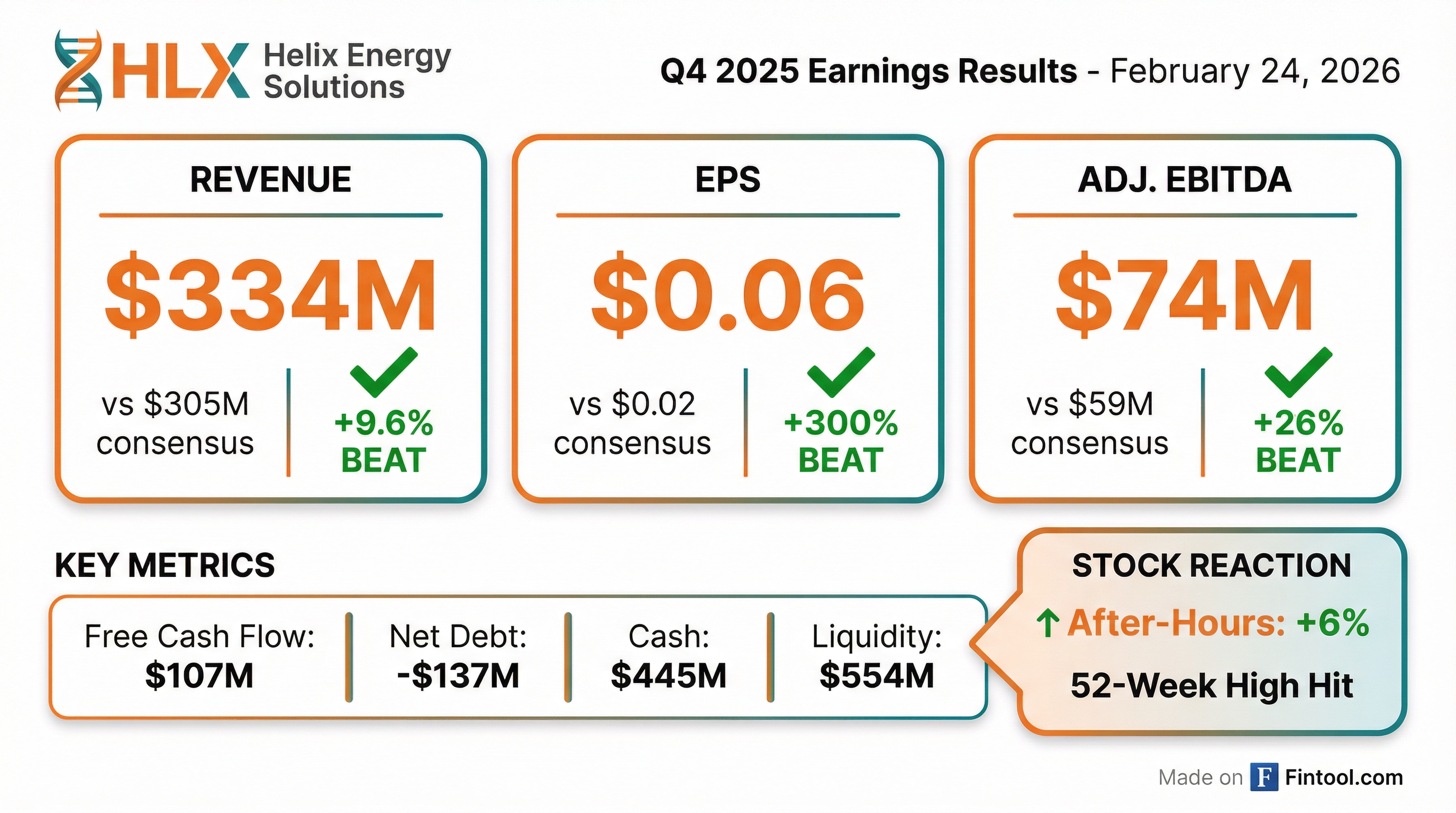

Helix Energy Solutions delivered a triple beat in Q4 2025, with revenue, EPS, and EBITDA all exceeding consensus expectations. The offshore energy services company generated $107 million in free cash flow during the quarter, driving its net debt position further negative to -$137 million. The stock surged 6% in after-hours trading, hitting a new 52-week high.

CEO Owen Kratz's take: "Our team delivered $74 million of EBITDA, our highest fourth quarter EBITDA since 2013. We generated Free Cash Flow of over $100 million during the quarter, delivering $120 million of Free Cash Flow for the full year 2025. We have amassed a substantial cash balance, $445 million at year end, providing significant optionality for its deployment."

Did Helix Beat Earnings?

Yes — across the board. Q4 2025 marked one of Helix's strongest quarters in recent years, with all key metrics exceeding Street expectations:

The strong performance was driven by late-season utilization in Shallow Water Abandonment (including the Epic Hedron heavy lift barge at 92% utilization) and the successful transition of the Sea Helix 1 to its new three-year Petrobras contract.

Full Year 2025 Results:

While full-year results declined YoY, the company maintained strong profitability with a 21% EBITDA margin and generated over $120 million in free cash flow despite challenging market conditions in the UK North Sea and Gulf of Mexico shelf.

2025 Revenue by Market Strategy:

- Decommissioning: 56%

- Production Maximization: 30%

- Renewables: 12%

- Other: 2%

How Did the Stock React?

HLX stock surged 6% in after-hours trading to $9.60, hitting a new 52-week high.

The stock has rallied approximately 65% from its 52-week low, reflecting improved execution, the strong balance sheet position, and increasing visibility on 2026 contracts.

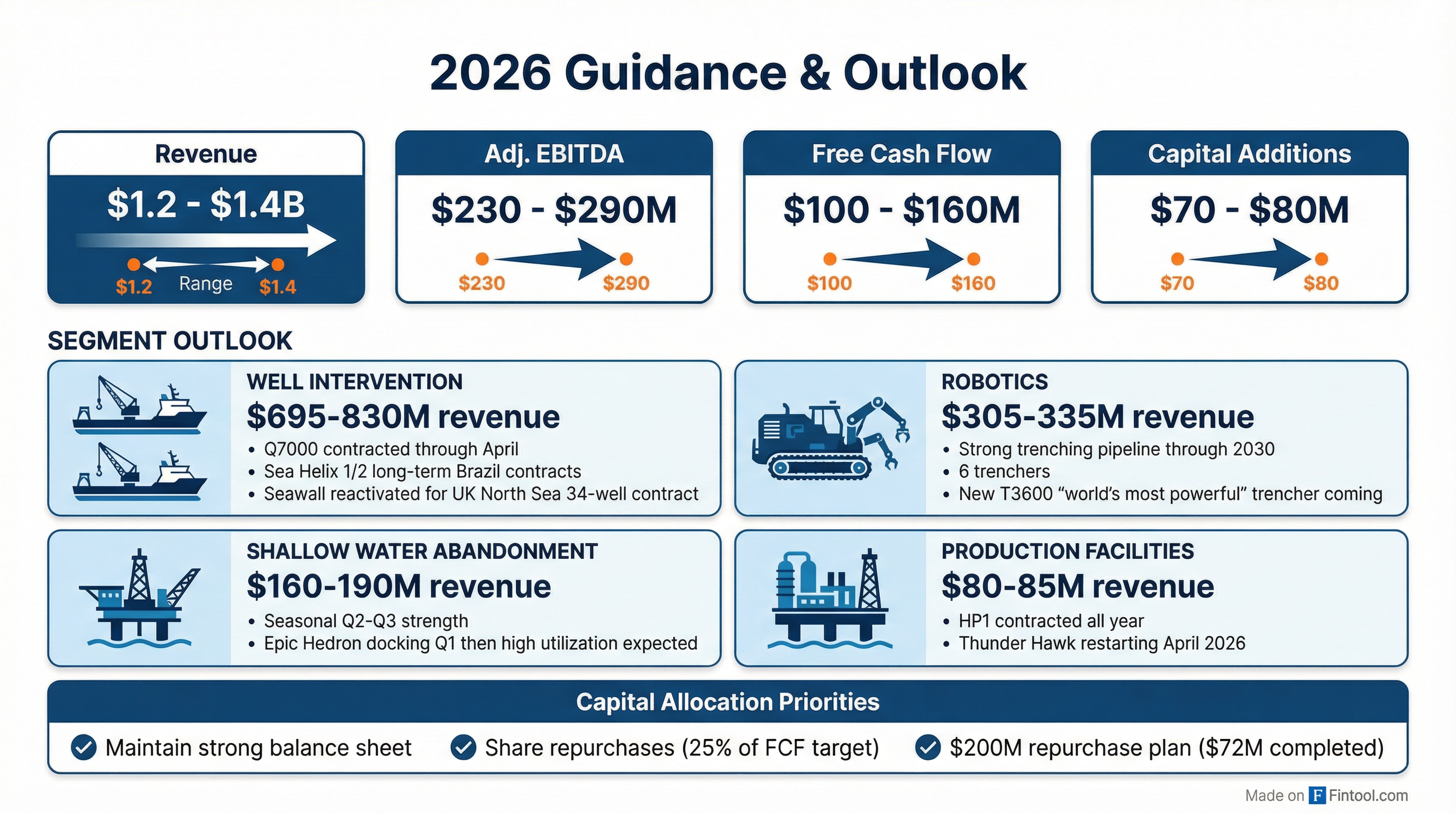

What Did Management Guide?

Helix provided 2026 guidance that implies a potential range around 2025 levels, with meaningful upside if spot market conditions improve:

Key 2026 guidance drivers:

- Well Intervention: Q4000 second-half utilization, Q7000 post-Shell Brazil, overall Brazil operating efficiency

- Robotics: Seasonal vessel utilization in North Sea and Asia Pacific

- Shallow Water Abandonment: Strength of oil & gas property reversions from bankruptcies, seasonal Gulf of Mexico shelf utilization

- Free Cash Flow: Seasonality and timing of receivables collections

The guidance range is wider than typical, reflecting the call-off nature of much of the business and seasonal variability.

What Changed From Last Quarter?

Positive Developments:

-

UK North Sea Contract Win: Secured a multi-year contract with a major operator for riserless P&A operations on up to 34 subsea wells. The Seawell was reactivated and commenced operations in February 2026.

-

Balance Sheet Strengthened Further: Net debt improved to -$137 million (vs -$31M in Q3 and -$53M in Q4 2024), representing one of the strongest balance sheet positions in the company's history.

-

Brazil Contracts Performing: Three vessels now on long-term contracts in Brazil with Petrobras and Shell at higher rates.

-

New Commercial Wins: During 2025, entered into ~$600 million in new contracts for 2026 and beyond, including:

- Renewables trenching contract for Hornsea 3 Offshore Wind Farm (300+ days beginning 2026)

- Four-year minimum 800-day trenching contract with NKT for the T3600 trencher

- Well Intervention contract in Gulf of America (minimum 150 days over 3 years)

- Three-year framework agreement with Exxon for Gulf of America shelf decommissioning

Headwinds:

-

YoY Revenue Decline: Q4 2025 revenue of $334M was down 6% from Q4 2024 ($355M), primarily due to lower Well Intervention activity in the North Sea.

-

Impairment Charge: Q4 2025 net income included an $18 million non-cash impairment loss related to Thunder Hawk oil and gas properties.

-

North Sea Market Recovering: COO Scotty Sparks noted "much better activity in 2026 than we did in 2025" with a "sizable change towards decommissioning." Both the Seawell and Well Enhancer are expected to have "very active seasons" with visibility into 2027.

Segment Performance

Well Intervention ($181M revenue, down from $226M YoY)

Robotics ($87M revenue, up from $82M YoY)

Strong performance with all six trenchers working and high vessel utilization (91% fleet average). Key activity:

- 134 integrated vessel trenching days on renewables and oil & gas projects

- 137 days stand-alone trenching on third-party vessels

- 100 days utilization on IROV boulder grabs

Shallow Water Abandonment ($58M revenue, up from $38M YoY)

Significant YoY improvement driven by the Epic Hedron heavy lift barge (92% utilization).

Production Facilities ($17M revenue)

Helix Producer I operated at full rates. Thunder Hawk field remained shut in, though management expects it to resume production in early April 2026 following a February workover.

Balance Sheet & Capital Allocation

Helix's balance sheet is exceptionally strong heading into 2026:

Capital Allocation Priorities:

- Maintain sufficient liquidity and low net debt

- Regulatory certification maintenance (~$40-45M in 2026)

- Strategic capital for growth opportunities (~$30-35M capex)

- Shareholder returns: Targeting 25% of free cash flow for share repurchases; $72M repurchased to date under $200M authorization

Cash Projection: Management expects the cash balance could approach $600 million by the end of 2026, creating "conditions that mean 2026 could be a year to consider meaningful M&A activities or capital investments."

Forward Catalysts

Near-Term (2026):

- Thunder Hawk production restart (April 2026)

- Seawell UK North Sea 34-well P&A campaign ramp

- Hornsea 3 offshore wind trenching contract commencement

- Epic Hedron return from Q1 drydock with strong seasonal utilization expected

Medium-Term (2026-2027):

- T3600 "world's most powerful trencher" deployment under NKT contract

- UK North Sea abandonment acceleration as regulatory deadlines approach

- Gulf of Mexico shelf decommissioning rebound from "boomerang" properties

- Potential acquisition opportunities given strong balance sheet position

Management Outlook: On guidance, CFO Erik Staffeldt noted: "Absent these events [Thunderhawk workover and SH1 docking], and despite the fact that various macro challenges from 2025 continue into 2026, we nonetheless see an environment that is better than 2025."

CEO Kratz added: "We could see a full year in 2026 with similar overall results as 2025, as we get set for what we anticipate will be a stronger 2027 all around."

CEO Succession & Governance

Owen Kratz announced his retirement in December 2025. The longtime CEO has led Helix for over 25 years, building the company into a market leader in well intervention and robotics.

COO Scotty Sparks noted: "He has been a pioneer in intervention, providing leadership and vision to build Helix and drive long-term value creation."

The board is actively working on succession with a long-established plan and outside advisors. Kratz will remain engaged during the transition. On the Q&A, Kratz noted that any major M&A decisions will involve "buy-in and participation with the new CEO."

Q&A Highlights

On M&A Opportunities:

"There are actionable opportunities. Right now, I'd say that the board management, myself, are all collaborating on looking at all the options." — Owen Kratz

Management indicated the company is at a "crossroads" with the next phase of growth focused on becoming more of a "solutions provider" rather than a commoditized service provider, plus potential geographic expansion.

On Competition Dynamics:

- Well Intervention: Competition is "generally minimal" — mainly competing against rig white space. As drillers expect high utilization in late 2026/2027, operators should shift intervention work back to Helix.

- Shallow Water Abandonment: More competitive as contractors position for the expected stronger 2027 market.

On Q7000 Utilization: The Q7000 will finish its Shell Brazil contract in April-May 2026. Management is pursuing opportunities in Brazil with smaller clients and is "very close to a larger contract" in Nigeria. Angola is also a new target market.

On 2027 Rate Expectations:

"As the drillers increase [rates], we tend to increase slightly as well. I think we'll see improved rates in the U.S. Gulf of Mexico. The North Sea, we should see more decommissioning work that should lead to slightly improved rates." — Scotty Sparks

On Q1 2026 Modeling:

CFO Erik Staffeldt clarified that the Thunderhawk workover expense ($16M) is a Q1 event, while the Sea Helix 1 docking ($20M+ impact) is expected in Q2 (possibly slipping to Q3). Analysts should haircut consensus Q1 EBITDA ($47M) by the Thunderhawk impact.

On 2027 Headwinds: The Sea Helix 2 has a docking scheduled for early 2027. The Seawell and Well Enhancer will also have maintenance periods in 2027, but in the off-season with no EBITDA impact.

Key Risks

- Seasonal Volatility: Q1 and Q4 typically weaker due to North Sea and Gulf of Mexico weather

- Customer Deferrals: Well intervention work can be deferred in soft commodity environments; oil prices declined nearly 20% YoY

- Rate Pressure: Competition in shallow water abandonment; well intervention competes mainly with rig white space

- Brazil Operations: Sea Helix 1 45-day docking mid-2026; Sea Helix 2 docking early 2027

- CEO Transition: Owen Kratz retiring; new CEO selection underway

The Bottom Line

Helix delivered an impressive Q4 2025 with a triple beat and exceptional free cash flow generation. The company enters 2026 with the strongest balance sheet in years (-$137M net debt), a robust contracted backlog (~$600M added in 2025), and improved visibility across key segments. While the guidance range is wide, the midpoint suggests stable to improving results, with meaningful upside if spot markets strengthen. The stock's 6% after-hours move reflects the market's recognition of improved fundamentals.