HARLEY-DAVIDSON (HOG)·Q4 2025 Earnings Summary

Harley-Davidson Misses EPS by 130% Despite Revenue Beat, Stock Drops 8%

February 10, 2026 · by Fintool AI Agent

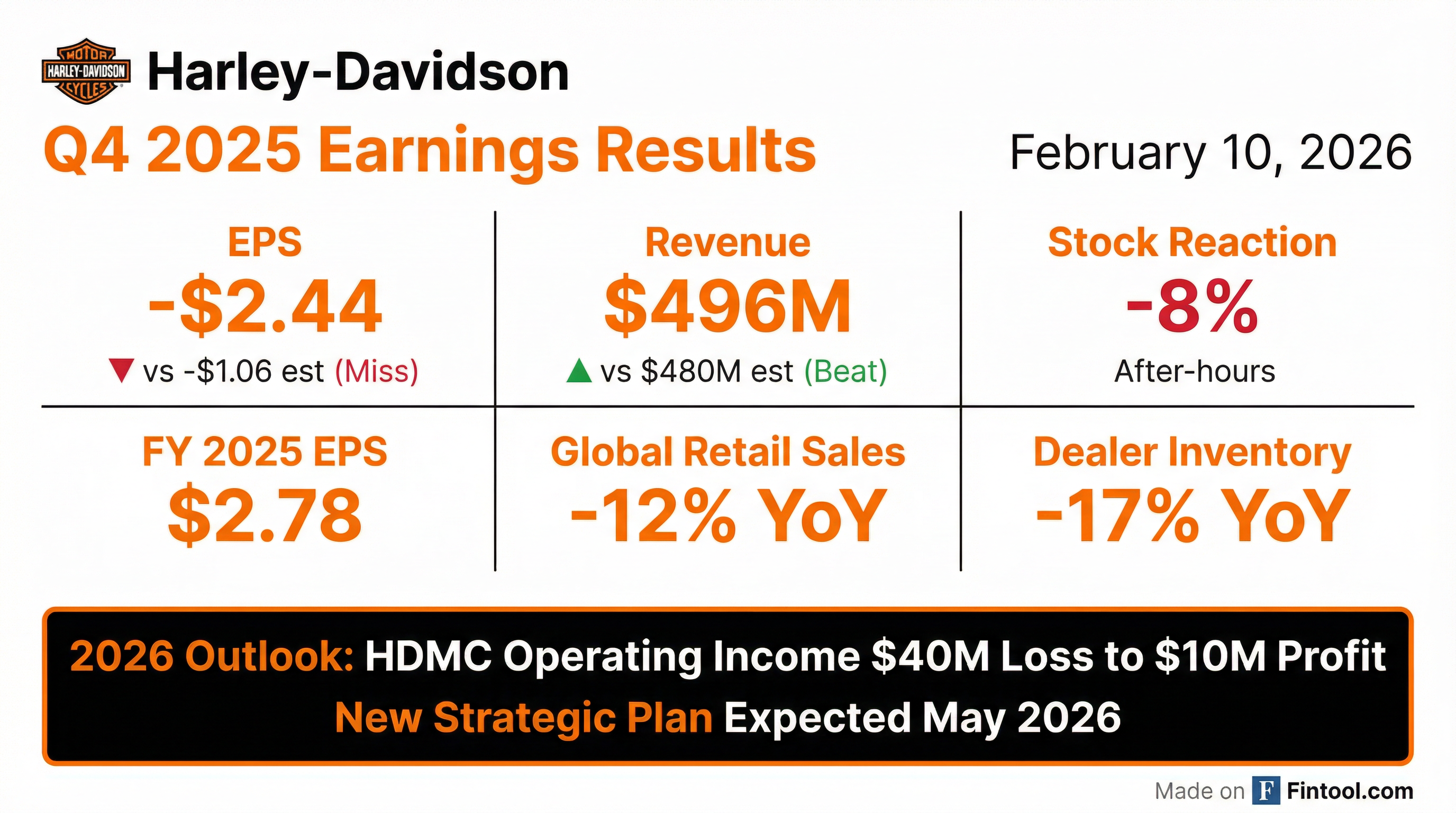

Harley-Davidson (NYSE: HOG) reported Q4 2025 results that sent shares tumbling 8% in after-hours trading. While revenue of $496 million beat expectations by 3.4%, the EPS loss of $2.44 was more than double the consensus estimate of -$1.06 . CEO Artie Starrs characterized the quarter as the end of "a challenging year" while emphasizing deliberate actions to "stabilize the business, restore dealer confidence, and align wholesale activity with retail demand" .

The quarter was marked by several significant developments: a strategic HDFS partnership with KKR and PIMCO that generated a $1 billion dividend to the parent company, continued dealer inventory reduction efforts, and the announcement that Jim Farley (Ford CEO) will not stand for re-election to the board .

Did Harley-Davidson Beat Earnings?

The headline numbers paint a mixed picture:

Full year 2025 results:

The severe EPS miss was driven by multiple factors: HDMC gross profit came in at a loss of $30 million (vs -$3 million prior year), operating expenses rose $19 million YoY to $230 million due to higher marketing spend, and tariff costs continued to weigh on margins .

CEO Artie Starrs framed Q4 as reflecting "deliberate actions" that don't "reflect the full potential of this company" . The intentional inventory reduction and promotional support for touring models positioned the business for what management views as a turnaround year.

What Drove the Massive EPS Miss?

The Q4 2025 loss was significantly worse than expected due to several compounding factors:

HDMC Full Year 2025 Operating Income Margin Bridge:

1. HDMC Operating Loss Widened HDMC reported an operating loss of $260 million vs -$214 million in Q4 2024 . Gross margin collapsed to -8.0% vs -0.8% in the prior year period, driven by:

- Increased tariff costs ($67M for full year, $22M in Q4 alone)

- Net pricing and incentive spending

- Lower volumes and negative operating leverage

2. HDFS Transaction One-Time Impacts While the HDFS partnership with KKR and PIMCO was strategically positive (generating $490 million operating income for the full year—a record), Q4 saw an operating loss of $82 million due to discrete liability management costs incurred to retire debt .

3. Continued Volume Pressure Global motorcycle shipments declined 4% YoY to 13,515 units , with HDMC revenue down 10% to $379 million .

How Did the Stock React?

HOG shares closed at $20.14 on February 9, then plunged to $18.50 in after-hours trading—an 8.1% decline.

Stock performance context:

- 52-week range: $19.33 - $31.25

- Current price vs. 52-week high: -41%

- Market cap: ~$2.4 billion

- P/E ratio (TTM): ~7.2x on FY 2025 EPS of $2.78

The stock is now trading near its 52-week lows, reflecting investor concerns about the turnaround timeline and near-term profitability challenges.

What Did Management Guide?

2026 guidance signals continued headwinds but with a path toward profitability:

Key guidance observations:

- Retail and wholesale shipments are expected to be roughly flat vs FY 2025's 132,535 retail / 124,477 wholesale units

- HDMC could break even at the high end of guidance, but wide range reflects uncertainty

- HDFS income drops significantly to $45-60M from $490M in FY 2025 (due to one-time transaction benefits in 2025)

- Critically, guidance "may be impacted by the new strategic plan expected to be announced in May 2026"

What Changed From Last Quarter?

Q3 2025 vs Q4 2025 sequential comparison:

The sequential drop is stark but reflects:

- Seasonality: Q4 is historically Harley's weakest quarter (motorcycle sales peak in spring/summer)

- Q3 HDFS benefit: Q3 2025 EPS of $3.10 was inflated by HDFS transaction gains

- Inventory alignment: Management deliberately pulled back wholesale to reduce dealer inventory

Dealer inventory down 17% YoY — a key strategic priority is being executed:

"We are taking deliberate actions to stabilize the business, restore dealer confidence, and align wholesale activity with retail demand." — CEO Artie Starrs

What Is Management's Turnaround Plan?

CEO Starrs outlined three immediate priorities and specific actions underway:

1. Restoring Dealer Health

- Reset relationship built on "mutual trust and respect, shared objectives, shared accountability, and shared success"

- Adjusted full facility model guidelines to balance global brand identity with local communities

- Shifted e-commerce strategy to drive dealership traffic rather than create "customer confusion and excessive discounting"

2. Reigniting Brand Momentum

"In recent years, our work has been too serious and at times too dark. That's not who our riders are. When they ride and gather, our riders are joyful, passionate, and community creators." — CEO Artie Starrs

Management signaled a return to optimistic, joyful brand advertising that celebrates the Harley community.

3. Reducing Costs

- $150 million annual run rate savings expected to impact 2027 and beyond

- End-to-end cost review underway with third-party specialists

- Acknowledged current overhead, manufacturing capacity, and operating expenses are "built for materially higher volumes than today's demand"

Cultural Reset: Return to Juneau Avenue All direct reports now working from Milwaukee headquarters, with formal office reopening planned for later this quarter. Management believes this improves "decision-making speed, cross-functional collaboration, and critically, accountability" .

Product Portfolio Acknowledgment

"The portfolio actions taken over recent years have put the brand out of reach for some existing and potential riders. To win, it's clear we need to sharpen our product focus." — CEO Artie Starrs

Management confirmed plans for more affordable motorcycles with focus on "critical price point motorcycles to help stoke demand" .

Global Retail Sales Breakdown

Retail performance showed regional divergence:

Notable observations:

- North America improved in Q4 (+5%), driven by Touring category strength

- EMEA weakened sharply (-24% in Q4), the worst performing region

- China remains weak but APAC improved from H1 2025 levels

- Latin America was the bright spot with positive growth in both Brazil and Mexico

U.S. Market Share (New 601+CC Segment):

Harley maintains dominant positions in Touring (76% Q4) and Cruiser (58% Q4) categories in the U.S., though full-year share declined modestly from prior year levels .

HDFS Transaction: Strategic Win Despite Q4 Loss

The HDFS partnership with KKR and PIMCO was the most significant development of 2025:

Transaction benefits:

- $1 billion dividend from HDFS to parent HDI in Q4 2025

- Transforms HDFS into "capital-light, de-risked business"

- Significantly reduced HDFS debt

- Improved ROE at HDFS

FY 2025 HDFS performance:

- Operating income: $490 million (record high)

- Revenue: $869 million (-16% YoY)

The Q4 operating loss of $82 million was due to discrete liability management costs to retire debt as part of the transaction . Looking forward, HDFS will generate steady but lower income ($45-60M guided for 2026).

HDFS Post-Transaction Business Mix:

Credit Quality Trends:

Credit losses have stabilized at 3.4% in FY 2025, only slightly higher than FY 2024. The 2020-2021 lows were influenced by federal stimulus payments and COVID-19 payment extensions .

Capital Allocation & Balance Sheet

Cash position strengthened significantly:

Operating Cash Flow declined significantly:

FY 2025 capital returns:

- Share repurchases: $347 million (13.1 million shares)

- Dividends paid: $86 million

- Total shareholder returns: $434 million

Accelerated Share Repurchase (ASR): On November 5, 2025, Harley entered a $200 million ASR with Goldman Sachs. Initial delivery was 6.3 million shares (80% of value), with final settlement expected by Q2 2026 .

Upcoming Debt Reduction: HDFS will further reduce debt with the maturity of a EUR 700 million medium-term note in Q2 2026 . Management is "being measured" on future share repurchases while finalizing the May strategic plan .

Multi-Year Capital Return History (2022-2025):

Since December 2021, Harley has repurchased 29% of shares outstanding (44.3M of 153.6M shares) . In July 2024, the company announced a plan to repurchase $1 billion of shares through 2026, of which $597M has been completed as of December 31, 2025 .

Board Change: Jim Farley Departing

Ford CEO James Duncan Farley Jr. notified the board he will not stand for re-election when his term ends at the upcoming annual meeting . The company stated his decision "was not due to any disagreement with the Company on any matter relating to its operations, policies, or practices."

The board is expected to decrease from nine to eight members .

LiveWire: Still Burning Cash, But Improving

LiveWire, Harley's electric motorcycle subsidiary, continues to operate at a loss but showed improvement:

Key highlights:

- #1 in U.S. retail sales of 50+hp EV street legal motorcycles for 2025

- Operating loss reduction driven by decreases in COGS and S&AE expense

- Reduced selling, administrative and engineering expense by $3M in Q4 and $27M for FY from continued cost focus

- S4 Honcho™ launch: Positive reaction at EICMA (Milan, Nov 2025), with production targeted to start Spring 2026

The 32% reduction in operating loss for FY 2025 was in-line with expectations. Harley renegotiated the LiveWire term loan, reducing principal from $100M to $75M, and LiveWire is now "working diligently to attract its own sources of capital" .

Tariff Exposure: Detailed Breakdown

Tariffs were a $67 million headwind in FY 2025 and are expected to increase to $75-105 million in 2026 :

2025 Tariff Impact by Quarter:

- Q1: $9M | Q2: $9M | Q3: $27M | Q4: $22M

2025 vs 2026 Estimated Tariff Costs by Source:

U.S.-Centric Manufacturing Footprint Provides Some Protection:

- 100% of core product (Touring, Trike, CVO, Softail) manufactured in U.S.

- ~95% of motorcycle revenue from U.S. customers comes from York, PA plant

- ~75% of U.S. sourcing from U.S.-based production facilities

- International assembly (APAC/EMEA) at Rayong, Thailand

Management noted: "H-D is grateful to the U.S. Administration and U.S. Congress for continuing to listen to input from the Harley-Davidson organization" .

Q&A Highlights

On HDFS Long-Term Earnings (Craig Kennison, Baird): CFO Jonathan Root clarified that the $45-60M 2026 HDFS guidance should eventually triple to ~$150M at steady state, though "it will probably take us 2.5, 3 years to get to that point" as the retail asset base rebuilds .

On 2026 Wholesale Cadence (Noah Zatzkin, KeyBanc): Management provided quarterly shipment guidance :

- Q1 2026: Down vs prior year (being "careful and considered")

- Q2 2026: Higher than prior year (positioning dealers for riding season)

- Q3 2026: Slightly lower (timing elements)

- Q4 2026: "Material" increase vs Q4 2025's depressed levels

On Touring Outlook (Robin Farley, UBS): Management expects Touring retail upside in 2026 driven by: (1) successful 2025 model year sell-down, and (2) excitement around the new Limited models with "sold orders" already building .

On Used vs New Pricing (Brandon Rolle, Loop Capital): Management noted stabilization and "nice improvement in used values" at both auction and retail. Used market insights are "informing some of the innovation" in product development .

On Long-Term Motor Company Margins (Jamie Katz, Morningstar): CEO Starrs deferred details to the May investor meeting but confirmed: "We don't think the current results reflect the full potential of the company. So a lot of upside" .

Key Risks & Concerns

1. Tariff Uncertainty Management withdrew 2025 guidance in Q1 citing tariff uncertainty . The Q1 2025 call noted direct tariff impact of $9 million in that quarter alone . With 2026 tariff exposure estimated at $75-105M (vs $67M in 2025), this remains a significant headwind .

2. Consumer Discretionary Pressure "Significant softness in high-ticket consumer discretionary spend" continues to weigh on demand .

3. International Exposure EMEA weakness (-24% Q4 retail) and lack of European manufacturing create vulnerability to retaliatory tariffs .

4. Strategic Clarity Delayed The "new strategic plan expected to be announced in May 2026" creates uncertainty—guidance could change significantly .

What to Watch Going Forward

-

May 2026 Strategic Plan: The biggest catalyst on the horizon. Management has signaled this will be a comprehensive reset.

-

Q1 2026 Retail Trends: Spring riding season will test whether dealer inventory right-sizing translates to improved sell-through.

-

Tariff Developments: Trade policy remains the wildcard—2026 tariff exposure estimated at $75-105M vs $67M in 2025 .

-

North America Touring Demand: The Touring category showed strength in Q4 (76% market share)—sustainability will be key .

-

HDFS Steady-State Earnings: With transaction benefits behind them, $45-60M guided income sets a new baseline.

-

LiveWire S4 Honcho Launch: Production targeted for Spring 2026 after positive EICMA reception .

Related Links: