HENRY SCHEIN (HSIC)·Q4 2025 Earnings Summary

Henry Schein Delivers Best Quarter in 15 Periods as EPS Jumps 13%

February 24, 2026 · by Fintool AI Agent

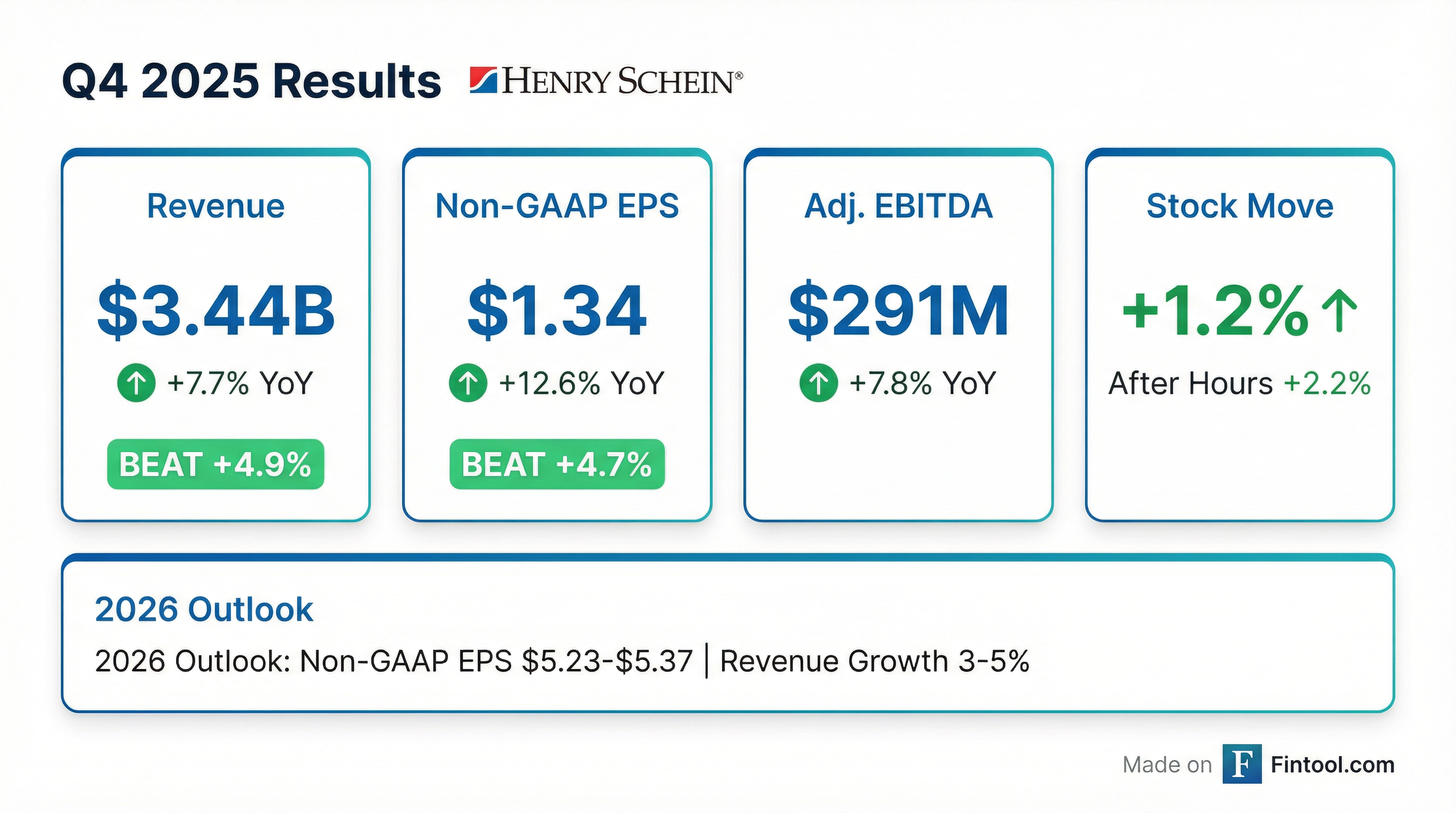

Henry Schein (NASDAQ: HSIC) reported Q4 2025 results that exceeded expectations across the board, delivering what management called the "highest sales growth in 15 quarters." The dental and medical distribution company posted revenue of $3.44B (+7.7% YoY) and non-GAAP EPS of $1.34 (+12.6% YoY), both comfortably ahead of consensus.

Shares rose ~1.3% during regular trading and added another 1.2% in after-hours, reaching $81.55.

Did Henry Schein Beat Earnings?

Yes — a double beat. Henry Schein exceeded both revenue and EPS expectations for Q4 2025:

This breaks a pattern of persistent revenue misses. Over the prior seven quarters, Henry Schein beat EPS estimates four times but missed revenue expectations in six of seven periods.

What Drove the Strong Results?

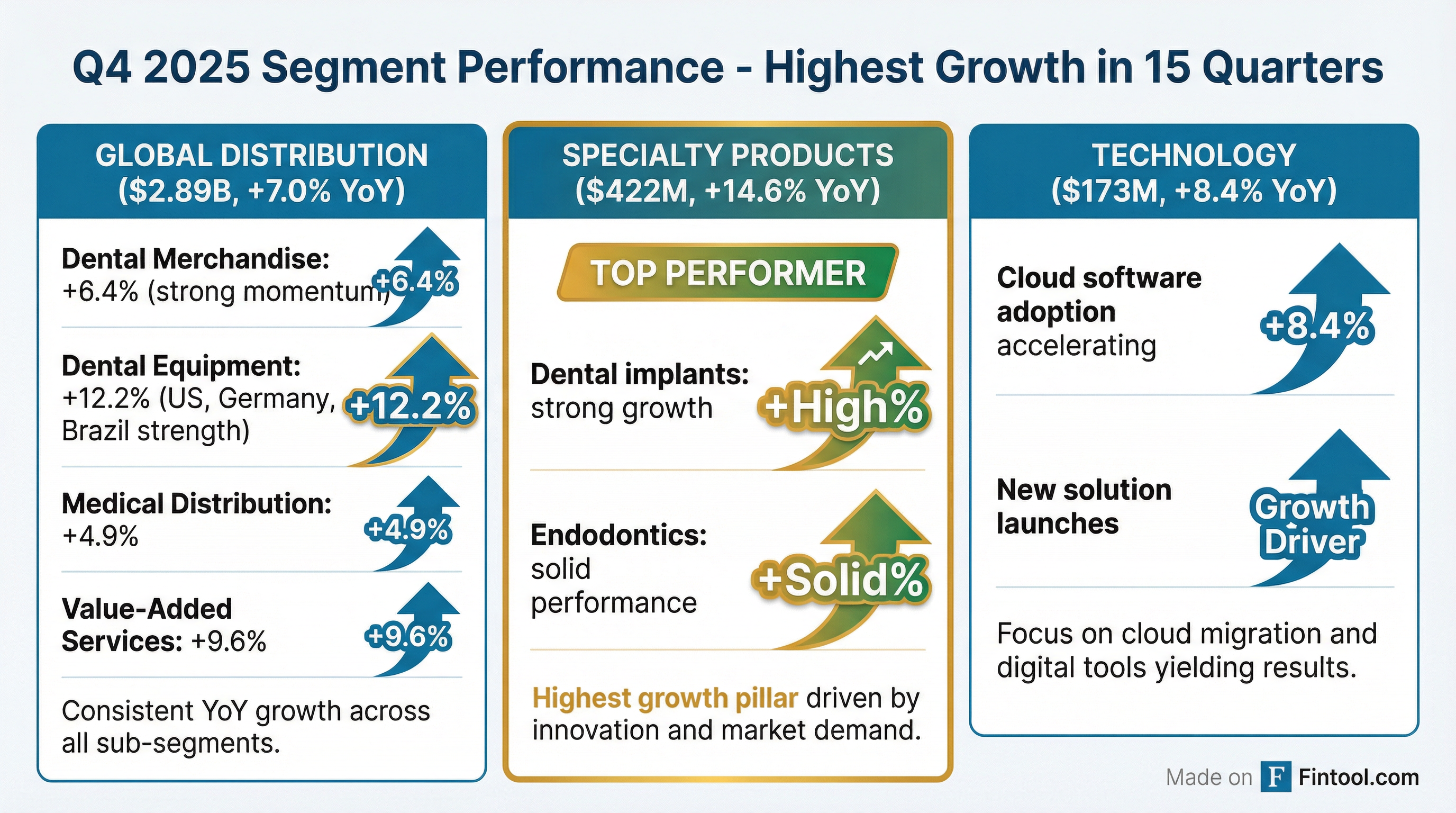

The standout performance came from equipment and specialty products:

Global Dental Equipment (+12.2% total, +9.1% CC) — The strongest segment. U.S. dental equipment grew 10.6% driven by traditional equipment and exclusive supplier-sponsored promotions. International grew 7.5% with particular strength in Germany, Brazil, Canada, and Australia.

Global Specialty Products (+14.6% total, +11.1% CC) — Strong performance in implants and biomaterials. Double-digit growth at BioHorizonsCamlog (Germany), S.I.N. (Brazil), and Biotech Dental (France). "We believe we continued to gain share across most markets."

Global Technology (+8.4% total, +7.6% CC) — Driven by practice management software. Double-digit growth in Dentrix Ascend and Dentally, the company's cloud-based systems.

Global Medical (+4.9% total, +4.8% CC) — Steady demand for medical products and pharmaceuticals, with continued strong performance in Home Solutions. Partially offset by lower comparative demand for respiratory products.

Full-year 2025 results showed steady improvement: total sales of $13.2B (+4.0% YoY), non-GAAP EPS of $4.97 (+4.9% YoY), and Adjusted EBITDA of $1.1B.

What Did Management Guide?

Henry Schein introduced 2026 financial guidance:

Earnings weighted to H2: Management noted that "given the implementation schedule for the value creation initiatives, we expect earnings growth to be weighted towards the second half of the year."

This guidance assumes stable dental and medical end-markets, foreign currency exchange rates remaining consistent with current levels, and that "the effects of tariffs can be mitigated."

What Changed From Last Quarter?

Revenue momentum accelerated. Q3 2025 delivered 4.0% total sales growth; Q4 jumped to 7.7%. Internal sales growth improved from 2.8% to 4.9%.

CEO transition imminent. Stanley Bergman announced that Fred Lowery will join as CEO "next week," marking the end of an era after 121 quarterly investor calls. Bergman will remain Chairman and expressed confidence that Lowery "will lead Henry Schein to even greater success."

Lowery, who joins from Thermo Fisher Scientific where he spent 20 years, outlined his priorities: "I've got a 100-day plan that includes a listening tour, so I'm gonna get out and meet some Team Schein members, some customers, and suppliers... I'm gonna dig in on the initiatives that are in place and validate the assumptions."

Bergman was direct about the cyber recovery: "I hope not to use the word cybersecurity. I hope our team doesn't use that again, because that incident's way behind us." He added: "We're back to where we were before October of 2023 when we had the cyber incident."

Aggressive buybacks continue. Henry Schein repurchased 12.1 million shares for $850 million in 2025, including 2.8 million shares ($200M) in Q4 alone. The company has $780 million authorized for future repurchases.

BOLD+1 Strategic Progress

Management highlighted significant progress on the 2025-2027 BOLD+1 strategic plan:

High-margin business mix improving: "2025 non-GAAP operating income from high-growth, high-margin businesses is approaching 50% of our total operating income. On-track to exceed goal of over 50% by the end of our strategic planning cycle in 2027."

Value creation initiatives on track: "Expect these initiatives to achieve annual run-rate operating income improvements of over $125 million by the end of 2026."

eCommerce platform rollout: Made substantial progress rolling out henryschein.com — expecting to complete the rollout to U.S. Dental and Canadian customers in Q1 2026, followed by U.S. Medical customers shortly thereafter, then global implementation.

Technology & AI Initiatives:

- AWS Partnership — Generative and agentic AI integration with Henry Schein One, including:

- Voice Notes — Real-time documentation assistant using AI to capture and summarize patient interactions

- Voice-activated charting, scheduling, and communications tools

- Image Verify — AI-powered quality assessment tool launched at Chicago Midwinter Show that evaluates clinical images at capture, "thereby helping reduce claims denials." Bergman: "Claims denials... is a real issue in the dental practice. This alone would attract customers to our system."

- New forms workflow — Captures insurance information from a photo of patient's card, "making patients' record entry faster and more accurate"

- Eligibility Pro enhancements — Faster response times and expanded payer connections

Cloud adoption momentum: Cloud-based customers increased by more than 20% YoY, with over 11,000 Dentrix Ascend subscribers — "the largest installed base in the world." The standard Dentrix Ascend subscription now covers basic practice management, revenue cycle management, imaging, and patient experience solutions.

New product launches:

- Curodont by Vvardis — Exclusive U.S. and U.K. distribution of a unique solution for detection and treatment of early-stage caries

- Cyto CBC — Exclusive agreement with CytoChip Inc. for a cartridge-based complete blood count analyzer providing lab quality results in ~8 minutes

Q&A Highlights

On Value Creation Cadence (Jeff Johnson, Baird): CFO Ron South confirmed the $125M run-rate improvement by year-end 2026 is "by no means linear," with benefits "more heavily weighted to the back half of the year." Regarding how much flows to the bottom line in 2027: "That remains to be seen... we'll have to see just where we are on the initiatives, what else is happening with the business."

On Implant Pricing (Allen Lutz, Bank of America): South noted there's "nothing unusual from a pricing perspective" in implants. The gross margin pressure is mix-driven as value implants (SIN, Biotech, Modentist) grow faster than premium lines. Bergman: "This is all a mix shift towards faster growth by these companies we've invested in."

On Dental Market Durability (Jason Bednar, Piper Sandler): Bergman was bullish: "The markets are stable, certainly in the US... leaning, I would say, positively." He attributed the strength to both stable patient traffic and Henry Schein's own execution: "We were hunkered down a little bit, a lot actually, on the cyber recovery. Our people were internally focused... In the second quarter, we felt very good that we dealt with the past, we started being aggressive."

On Equipment Promotions (Kevin Caliendo, UBS): Bergman pushed back on the idea of "massive promotions," calling it "a normal year-end" with standard tax-motivated buying. He noted certain manufacturers "had higher priced products per unit" with extra features that excited the sales force. "These were not promotions that pulled from one quarter to the other. Going into the first quarter... our backlog was good."

On U.S. Implant Market (Jonathan Block, Stifel): South was candid: "Inside the U.S., I don't think it's at 5%-8%. We're seeing still something probably less than, definitely less than 5% in terms of market growth in the U.S." The company launched the SynergeS Value Implant in Q4 and has "a lot of optimism" for its 2026 contribution.

On Tariffs (Brandon Vazquez, William Blair): Bergman's approach: "We anticipate passing on any tariff increases, if there are any, that we need to make to our customers." The company is also pursuing alternative sourcing from different countries. On the flat 15% tariff scenario: "We should be able to deal with that, at least in the short term."

On Remeasurement Gains (Kevin Caliendo, UBS): South confirmed guidance "assumes remeasurement gains will be lower in 2026 than it was in 2025." The company has "a couple of situations where we are contemplating transactions that could result in a range of remeasurement gain outcomes."

How Did the Stock React?

HSIC shares rose +1.3% during regular trading to $80.57 and added another +1.2% in after-hours to $81.55. The stock is now trading near its 52-week high of $82.80.

Context: The stock has rallied ~33% from its 52-week low of $60.56, reflecting improving fundamentals and the successful execution of the BOLD+1 strategic plan. The 50-day moving average is $77.23, and the 200-day is $71.36.

Capital Allocation

Henry Schein maintained an aggressive return of capital to shareholders while investing in growth:

The balance sheet shows $156M cash, $2.3B long-term debt, and $764M drawn on credit lines. Total debt increased during the year to fund buybacks. Debt-to-Adjusted EBITDA stands at 2.6x as of December 27, 2025.

Key Risks Flagged

Management's forward-looking statement disclosures highlight several risks:

- Tariff exposure — The company flagged "changes to laws and policies governing foreign trade, tariffs and sanctions" as a risk, including potential additional tariffs and retaliatory measures

- Cybersecurity — While insurance proceeds related to the Q4 2023 cyber incident have been recovered ($40M total), the company continues to highlight cybersecurity as an ongoing risk

- CEO transition — Leadership changes always carry execution risk, though Bergman's continued presence as Chairman provides continuity

- Competition from e-commerce — Third-party online commerce sites remain a competitive threat

- Geopolitical — The Ukraine war, Israel-Gaza conflict, and broader Middle East tensions are specifically mentioned

Looking Ahead

The Q4 beat and raised guidance suggest Henry Schein's BOLD+1 strategic plan is gaining traction. Management emphasized that "the growth we have achieved, especially over the second half of 2025, demonstrates the effective execution" of this strategy.

Key catalysts to watch:

- Fred Lowery's first earnings call (Q1 2026) — Will provide insight into strategic priorities under new leadership

- Equipment demand sustainability — Can the 12% equipment growth continue as interest rates remain elevated?

- Technology segment — Cloud adoption trends, AWS/AI integration with Henry Schein One, and new product launches

- Value creation execution — $125M run-rate operating income improvements expected by year-end 2026

- eCommerce platform — Henryschein.com rollout completion in H1 2026

- Capital deployment — $780M buyback authorization remaining; acquisition appetite under new CEO

The company will hold its earnings conference call at 8:00 AM ET on February 24, 2026.

Analysis generated by Fintool AI Agent on February 24, 2026. Updated with earnings call transcript Q&A highlights. Data sourced from company filings, earnings call transcript, and S&P Global.