IDEAYA Biosciences (IDYA)·Q4 2025 Earnings Summary

IDEAYA Posts Q4 Loss But Narrows Full-Year Loss 59% as OptimUM-02 Readout Nears

February 17, 2026 · by Fintool AI Agent

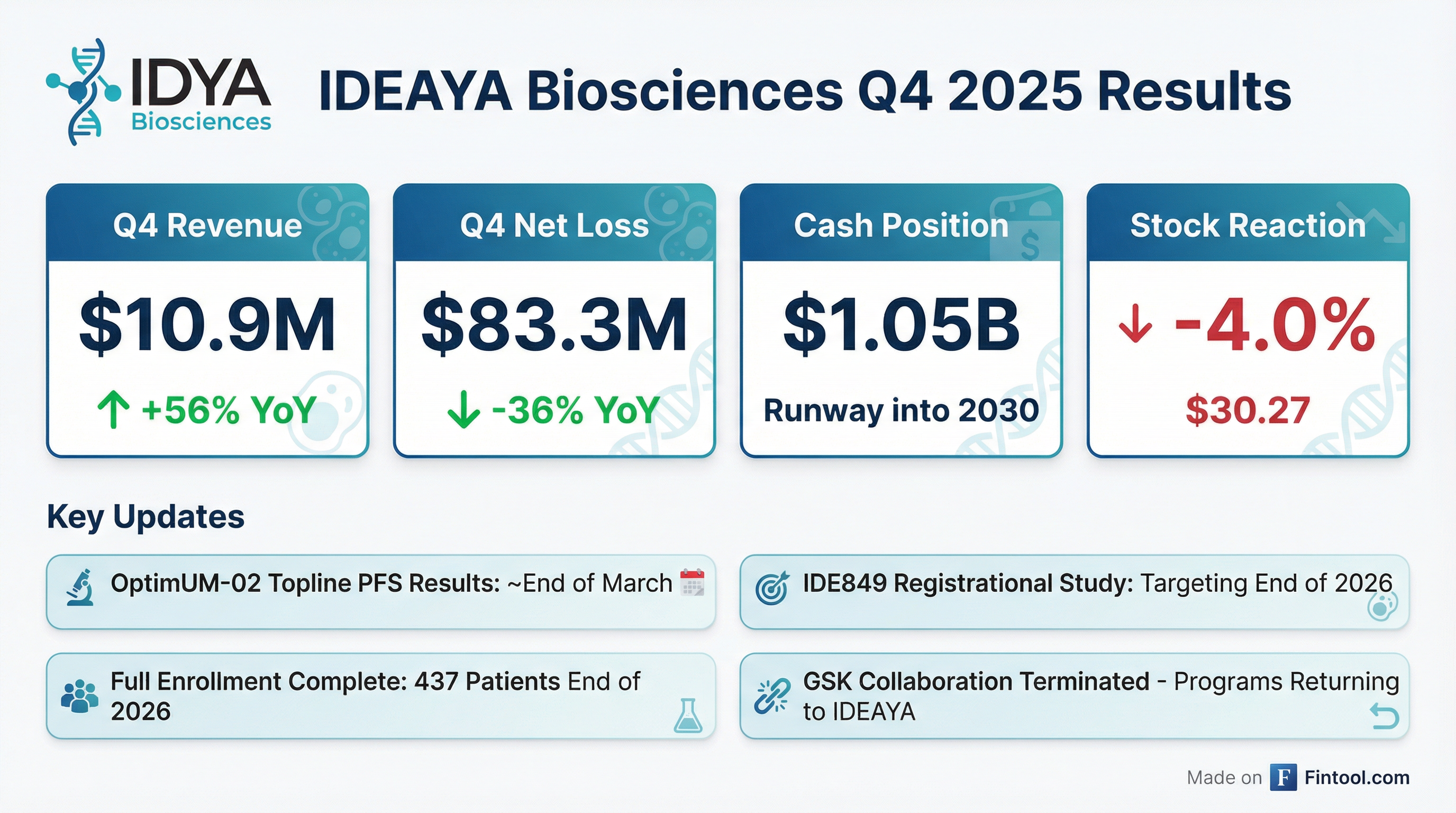

IDEAYA Biosciences (NASDAQ: IDYA) reported Q4 2025 results with a net loss of $83.3 million, a 36% improvement from the year-ago quarter, as the precision oncology company approaches a pivotal Phase 3 readout for its lead asset darovasertib. The stock fell 4.0% to $30.27 on the news, though investor focus remains squarely on the OptimUM-02 topline PFS results expected by approximately the last week of March.

Did IDEAYA Beat Earnings?

As a clinical-stage biotech without commercial products, IDEAYA's quarterly results are evaluated primarily on cash burn management and pipeline execution rather than traditional revenue/EPS metrics. Key financials:

The significant Q4 2024 R&D expense included a $75 million upfront payment to Hengrui Pharma for the IDE849 license agreement, which inflated the year-ago comparison.

For the full year 2025, IDEAYA generated $218.7 million in collaboration revenue (vs. $7.0 million in FY 2024) driven by the Servier exclusive license agreement for darovasertib. The full-year net loss narrowed dramatically to $113.7 million from $274.5 million in FY 2024.

What's the Cash Runway?

IDEAYA exited the quarter with approximately $1.05 billion in cash, cash equivalents, and marketable securities, down from $1.08 billion at the end of 2024. Management expects this to fund operations into 2030.

The $210 million upfront payment from Servier related to the darovasertib license agreement significantly extended the runway during 2025.

How Did the Stock React?

IDYA shares fell 4.0% to $30.27 on the earnings announcement. The stock trades:

- 12% below its 50-day moving average ($34.47)

- 10% above its 200-day moving average ($27.36)

- 23% below its 52-week high of $39.28

- 125% above its 52-week low of $13.45

The muted reaction reflects that investors are waiting for the OptimUM-02 PFS readout, which is the primary near-term catalyst.

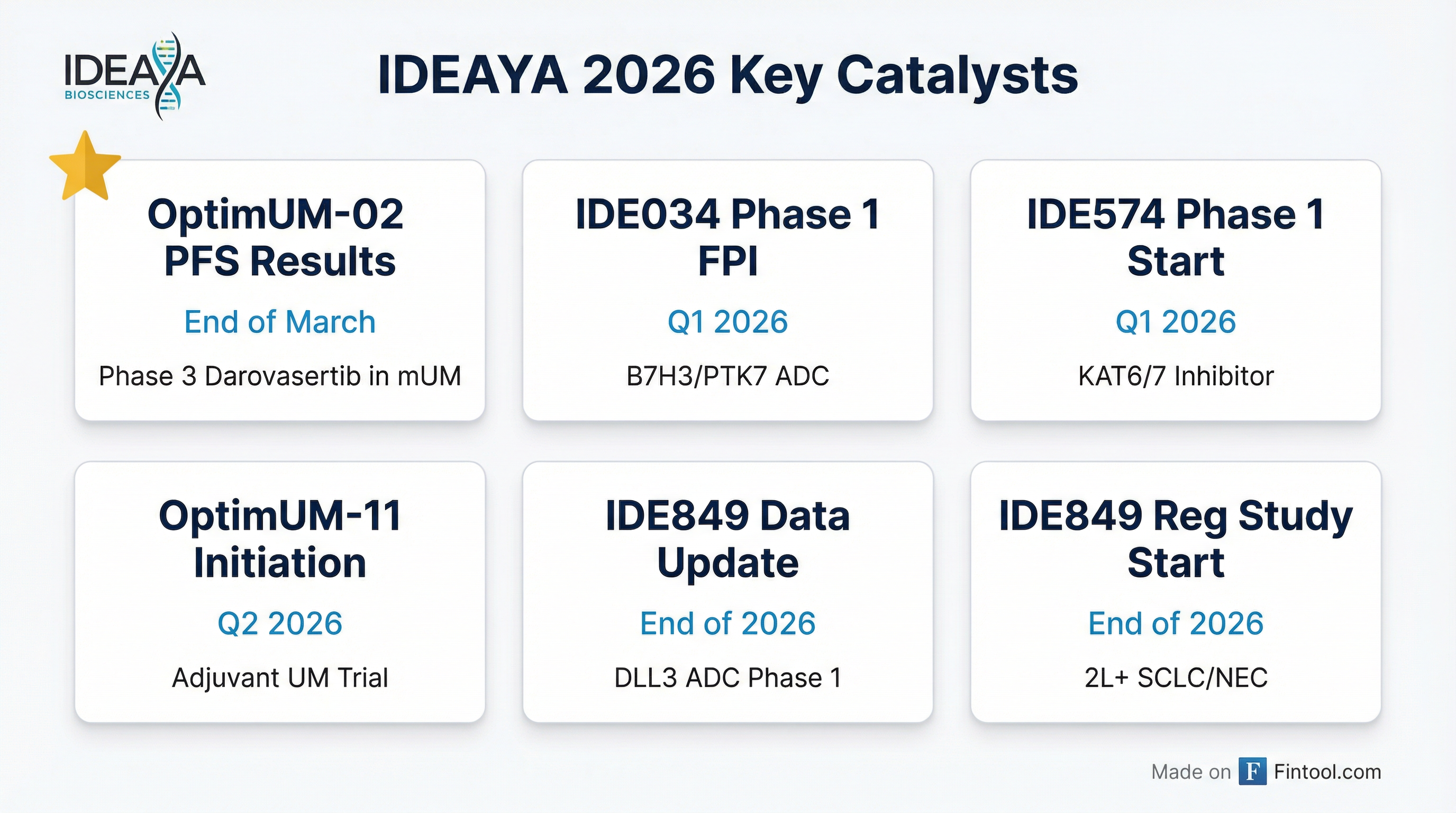

What Are the Key Upcoming Catalysts?

The most significant near-term event is the OptimUM-02 topline PFS results, expected by approximately the last week of March 2026.

OptimUM-02 Trial Details

- 130 PFS events have been confirmed by blinded independent central review (BICR)

- ~313 patients randomized 2:1 (treatment vs. control) in the Phase 2b/3 portion

- 437 patients total enrollment complete

- Positive topline PFS results would enable a potential accelerated approval filing in the U.S.

2026 Milestone Calendar

What Changed From Last Quarter?

GSK Collaboration Terminated

In December 2025, GlaxoSmithKline notified IDEAYA of its intention to terminate the Collaboration, Option and License Agreement dated June 15, 2020. GSK will transfer the Werner Helicase (IDE275) and Pol Theta (IDE705) clinical programs back to IDEAYA.

This is a significant development that returns two clinical-stage assets to IDEAYA's direct control but also increases future R&D burden.

Commercial Readiness Advancing

CEO Yujiro S. Hata highlighted continued build-out of the U.S. commercial organization in anticipation of the OptimUM-02 topline results:

"We had a strong quarter of clinical execution, clinical pipeline expansion and commercial readiness activities. The key highlights include completing full enrollment of 437 patients in OptimUM-02, our Phase 2/3 registrational trial in first line HLA*A2-negative mUM, submission of IND filings for IDE034, a potential first-in-class B7H3/PTK7 bispecific TOP1 ADC, and IDE574, a KAT6/7 dual inhibitor, and continued build out of our U.S. commercial organization in anticipation of our upcoming topline PFS results."

G&A Expense Increase

G&A expenses rose 71% YoY to $18.8 million, driven by higher personnel-related expenses and consulting/legal patent fees to support company growth and darovasertib commercial preparation activities.

What's the Investment Thesis?

Bull Case:

- OptimUM-02 positive results could lead to accelerated approval for the first targeted therapy in metastatic uveal melanoma

- Diversified pipeline with multiple shots on goal across uveal melanoma settings (metastatic, neoadjuvant, adjuvant)

- IDE849 (DLL3 ADC) provides optionality in the large SCLC market

- $1.05B cash runway into 2030 provides financial stability through multiple data readouts

Bear Case:

- Binary event risk with OptimUM-02 readout in ~6 weeks

- GSK collaboration termination increases future R&D burden

- Rising G&A expenses as company builds commercial infrastructure

- Pre-commercial biotech valuation entirely dependent on clinical success