Earnings summaries and quarterly performance for INTERNATIONAL PAPER CO /NEW/.

Executive leadership at INTERNATIONAL PAPER CO /NEW/.

Andy Silvernail

Chief Executive Officer

Clayton Ellis

Senior Vice President, Global Cellulose Fibers

James Royalty

Senior Vice President, Containerboard and Recycling

Joseph Saab

Senior Vice President, General Counsel and Corporate Secretary

Joy Roman

Senior Vice President, Chief People and Strategy Officer

Lance Loeffler

Chief Financial Officer

Timothy Nicholls

Executive Vice President and President, DS Smith

Tom Hamic

Executive Vice President and President, North American Packaging Solutions

Board of directors at INTERNATIONAL PAPER CO /NEW/.

Ahmet Dorduncu

Director

Anders Gustafsson

Director

Anton Vincent

Director

Christopher Connor

Lead Independent Director

Clinton Lewis Jr.

Director

David Robbie

Director

Jacqueline Hinman

Director

Jamie Beggs

Director

Kathryn Sullivan

Director

Scott Tozier

Director

Research analysts who have asked questions during INTERNATIONAL PAPER CO /NEW/ earnings calls.

Mark Weintraub

Seaport Research Partners

7 questions for IP

Charlie Muir-Sands

BNP Paribas

5 questions for IP

Matthew McKellar

RBC Capital Markets

5 questions for IP

Michael Roxland

Truist Securities

5 questions for IP

Philip Ng

Jefferies

5 questions for IP

George Staphos

Bank of America

4 questions for IP

Gabe Hajde

Wells Fargo & Company

3 questions for IP

Anojja Shah

UBS Group AG

2 questions for IP

Anthony Pettinari

Citigroup Inc.

2 questions for IP

Detlef Winckelmann

JPMorgan Chase & Co.

2 questions for IP

Mike Roxland

Truist Securities

2 questions for IP

Phil Ng

Jefferies Financial Group Inc.

2 questions for IP

Matt McKellar

RBC Capital Markets

1 question for IP

Recent press releases and 8-K filings for IP.

- The global market is set to grow from $4.02 billion in 2024 to $4.67 billion in 2025—a 16.4% CAGR—and is forecast to hit $8.46 billion by 2029.

- Growth is driven by skyrocketing internet use, widespread smartphone adoption, cloud-based application demand, video streaming surges, telecom infrastructure investments, and enterprise bandwidth requirements.

- Key technological trends include 400G coherent optics, flexible grid DWDM systems, modular pluggable transceivers, software-defined networking, and quantum cryptography for optical transmission.

- Leading players are Huawei Technologies, Cisco Systems, HPE, Fujitsu, and Ericsson; notably, HPE’s $14 billion acquisition of Juniper Networks in July 2025 aims to double its networking business.

- North America led the market in 2024, while Asia-Pacific is projected to be the fastest-growing region through 2029.

- In 2025, the global rigid paper containers market reached USD 83.9 billion and is projected to grow to USD 119.5 billion by 2035.

- Major industry moves include the USD 12.7 billion Smurfit WestRock merger and International Paper’s USD 7.2 billion acquisition of DS Smith to expand its European footprint.

- Key market drivers are sustainability and eco-friendly packaging, with rising demand for biodegradable and recyclable containers.

- North America leads due to strong regulatory support and consumer awareness, while Asia-Pacific is the fastest-growing region driven by urbanization and e-commerce expansion.

- CEO Andy Silvernail reaffirmed IP’s shift to an exclusive packaging business, having exited a $700 million cost base and committing to spend ~50% more per mil in North American converting plants during 2025–27 to modernize capacity.

- Announced a planned spin-off of the EMEA business, targeting the exit of $250–300 million of costs, impacting ~4,000 employees across ~30 facilities, and absorbing ~$40 million in pre-spin charges (60% severance, 40% capex) to reshape its cost curve.

- North America will aggressively modernize mills and converting sites, pursuing $300–400 million of latent mill productivity through greenfield/brownfield investments and equipment upgrades.

- Outlined a capital allocation framework for each NewCo with conservative balance sheets, reviewed dividend levels to ensure reinvestment capacity and predictability, and maintained flexibility for share buybacks or acquisitions.

- Confirmed a $70/ton containerboard price increase effective March 1, to be passed through to box pricing despite recent RISI index volatility, leveraging IP’s ~80% market integration.

- International Paper will split into two standalone regional packaging businesses and spin off its EMEA NewCo by late 2026 or early 2027 to unlock value in each market.

- EMEA cost-reduction program will exit $250 million–$300 million of costs, close ~30 facilities and affect ~4,000 jobs ahead of the spin-off.

- North America will invest 50 % more per ton in converting capacity during 2025–2027 versus the prior three-year run rate and target $300 million–$400 million of latent mill productivity gains.

- IP expects North American packaging demand to grow 0 %–1 % in 2026 (industry), with the company forecasting to outperform by a few points; Q1 storms will add ~$40 million–$50 million of natural-gas costs.

- Each NewCo will launch with conservative balance sheets and dividends aligned to cash flows, prioritizing predictable dividend growth and capital flexibility post-spin.

- Spinning off regional powerhouses: IP will separate its integrated North American and EMEA packaging businesses into standalone companies to "liberate" regional focus and capital allocation, with the EMEA spin expected later this year or early next year.

- $250–$300 million cost reduction in EMEA with 4,000 job impacts: The first wave will eliminate $250–$300 million of cost in Europe, closing ~30 facilities and affecting ~4,000 employees to reshape the cost curve before the spin-off.

- Accelerated capex and productivity focus in North America: IP plans to invest ~50% more per ton in converting facilities in 2025–2027 versus the prior three-year run rate and unlock $300–$400 million of latent mill productivity through modernization.

- Price increase and market outlook: A $70/ton containerboard price increase takes effect March 1, and IP expects North American market growth of 0–1% in 2026, with the company projecting to outperform the industry by a few points.

- International Paper will separate into two independent, publicly traded companies—one for North America and another for EMEA—with a spin-off of the combined EMEA Packaging business planned within 12–15 months.

- The move follows the 2025 acquisition of DS Smith and $23.6 billion in 2025 sales, but the company swung to a net loss due to transaction and integration costs.

- Andy Silvernail will remain chair and CEO of the North American unit, while Tim Nicholls will lead the EMEA packaging company, chaired by David Robbie.

- Investors reacted cautiously: shares fell 1.1% to 3,030 pence in London and rose 1.1% to $41.96 in New York pre-market; the stock is down 28% over the past 12 months and the market cap is about $21.9 billion.

- International Paper will spin off its EMEA Packaging business within 12–15 months, with a planned dual listing in London and New York; the transaction structure and tax treatment depend on final terms, and IP will retain a meaningful ownership stake (Tim Nicholls to serve as EMEA CEO).

- Pro forma FY 2025 standalone North America Packaging Solutions achieved net sales > $15 billion and adjusted EBITDA ≈ $2.3 billion.

- Q4 2025 North America adjusted EBITDA was $560 million, reflecting volume headwinds of $87 million, maintenance/outages of $41 million, and input cost benefits of $24 million.

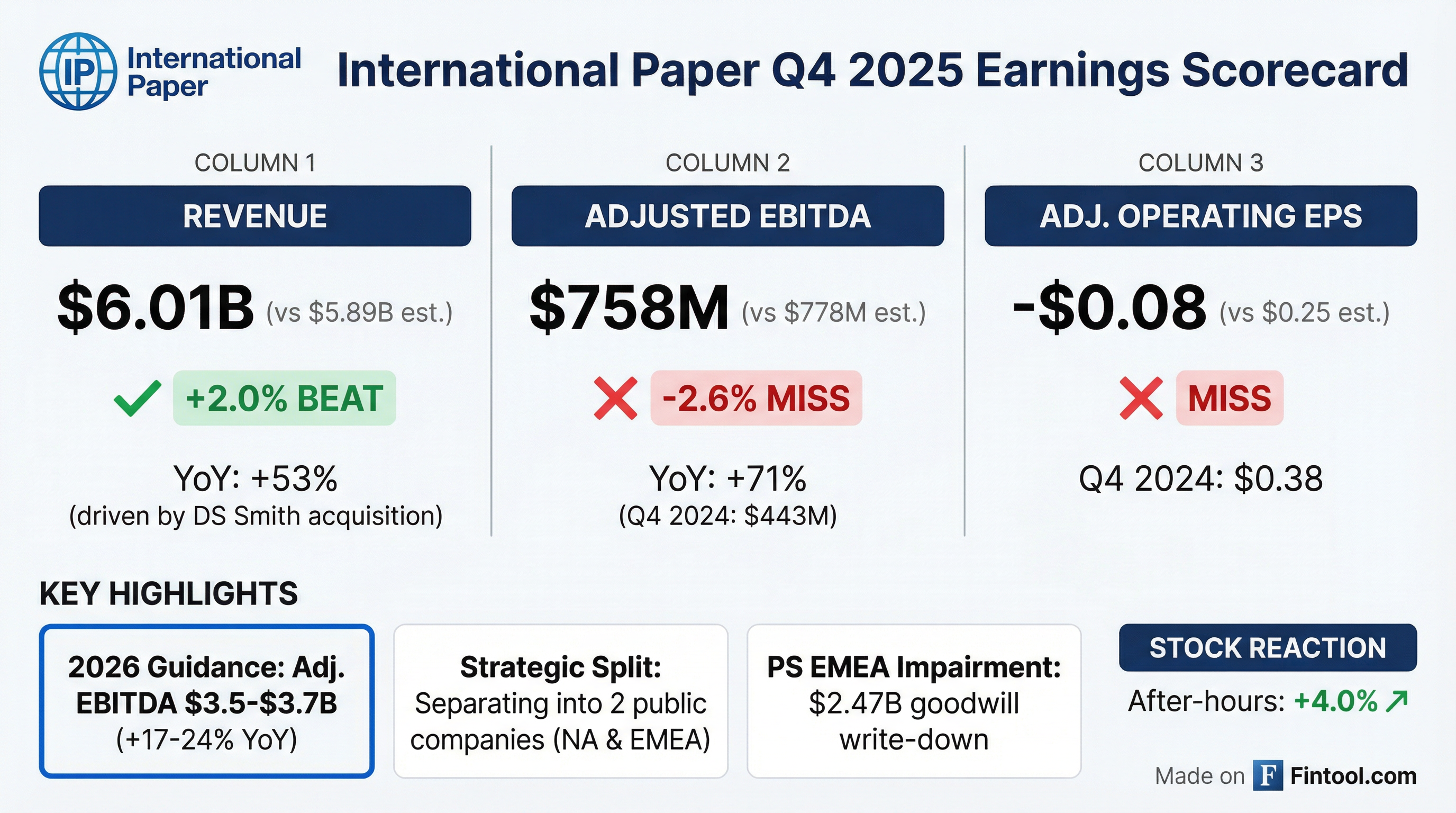

- 2026 enterprise guidance targets net sales of $24.1 billion–$24.9 billion, adjusted EBITDA of $3.5 billion–$3.7 billion, free cash flow of $300 million–$500 million, and Q1 adj EBITDA of $740 million–$760 million.

- International Paper will spin off its EMEA Packaging business into a separate publicly traded company within 12–15 months, with IP retaining a meaningful stake and listings planned on the London and New York Stock Exchanges.

- Pro forma FY 2025 net sales: North America packaging > $15 billion and ~$2.3 billion of Adjusted EBITDA; EMEA packaging ~$8.5 billion net sales and ~$800 million of Adjusted EBITDA.

- Q4 2025 performance: North America Packaging Solutions delivered $560 million of Adjusted EBITDA (impacted by non-strategic exits, fewer shipping days, and maintenance outages) ; EMEA Packaging achieved $19 million of sequential EBITDA growth.

- 2026 outlook: enterprise net sales of $24.1–$24.9 billion, Adjusted EBITDA of $3.5–$3.7 billion, and free cash flow of $300–$500 million, excluding incremental pricing effects.

- International Paper to create two independent public packaging companies in North America (2025 net sales $15.2B) and EMEA (2025 net sales $8.5B)

- Enterprise FY25 net sales $23.6B, adj. EBITDA $3.0B (12.6% margin), free cash flow $(159)MM; Q4 sales $6.0B, adj. EBITDA $758M (12.6% margin)

- North America Packaging delivered $2.3B adj. EBITDA (15.7% margin) on $15.2B net sales, up 37% YoY

- 2026 targets: total net sales $24.1–24.9B, adj. EBITDA $3.5–3.7B, and free cash flow $300–500MM

- International Paper will spin off its EMEA Packaging business into a separate publicly traded company (expected within 12–15 months), potentially tax-free, with listings on the London and New York Stock Exchanges.

- North America delivered 37% year-over-year adjusted EBITDA growth in 2025 and expanded its adjusted EBITDA margin by 340 basis points, while enterprise adjusted EBITDA margin grew by 230 basis points amid transformational investments.

- Pro forma standalone 2025 results show Packaging Solutions North America with net sales >$15 billion and $2.3 billion Adjusted EBITDA, and EMEA Packaging with net sales ~$8.5 billion and $800 million Adjusted EBITDA.

- For full year 2026, International Paper targets enterprise net sales of $24.1 billion–$24.9 billion, Adjusted EBITDA of $3.5 billion–$3.7 billion, and free cash flow of $300 million–$500 million, with Q1 Adjusted EBITDA guidance of $740 million–$760 million (excluding price actions).

Fintool News

In-depth analysis and coverage of INTERNATIONAL PAPER CO /NEW/.

Quarterly earnings call transcripts for INTERNATIONAL PAPER CO /NEW/.

Ask Fintool AI Agent

Get instant answers from SEC filings, earnings calls & more