IQVIA HOLDINGS (IQV)·Q4 2025 Earnings Summary

IQVIA Beats on Revenue and EPS as R&D Bookings Surge to 1.18x

February 5, 2026 · by Fintool AI Agent

IQVIA delivered a strong close to fiscal 2025, posting Q4 revenue of $4.36 billion (+10.3% YoY) and adjusted EPS of $3.42 (+9.6% YoY), beating consensus estimates on both metrics . The clinical research and healthcare intelligence company's R&D Solutions segment showed particular strength with quarterly bookings exceeding $2.7 billion and a book-to-bill ratio of 1.18x, signaling continued demand for clinical trial services despite a challenging biotech funding environment .

Did IQVIA Beat Earnings?

Yes, IQVIA beat on both revenue and EPS.

This marks IQVIA's fifth consecutive quarter of EPS beats, continuing a strong track record of execution. Revenue grew 10.3% on a reported basis and 8.1% at constant currency, the strongest quarterly growth rate of FY 2025 .

CEO Ari Bousbib attributed the beat to "expanded go-to-market strategy, operational discipline, and investments in AI innovations" that led to "clear differentiation and strong topline growth" across both commercial and clinical businesses .

What Did Management Say About AI?

The Q&A session was dominated by investor questions about AI disruption following recent market volatility tied to concerns about AI's impact on service businesses. CEO Ari Bousbib delivered an extensive defense of IQVIA's positioning :

"AI agentification is a positive, has been a positive, will continue to be a positive for us. IQVIA has the largest proprietary healthcare information assets in the world and is the foundation of our value to clients. That access is not available."

Bousbib outlined three requirements for AI agents and why IQVIA is well-positioned :

-

Proprietary data at scale: "Our data is not readily available on the web... it's sourced, de-identified, cleansed, curated, and integrated into data lakes. We do this at huge cost and on a massive scale, and we have been doing this for decades."

-

Domain expertise: "To build the algorithms required to develop AI agents, you need the ability to read, understand, and interpret these highly complex data sets in their proper context... This is what we've been calling healthcare-grade AI."

-

Technology stack: "The third one can be bought... we choose the model that's best suited to the task."

Key AI deployment metrics :

- 150+ agents deployed across clinical and commercial workflows

- 30+ use cases covered to date

- Partnership with NVIDIA for over a year building agents into workflows

- Strategic collaboration with AWS announced, naming AWS as preferred agentic cloud provider

On the distinction between IQVIA and horizontal AI models, Bousbib stated :

"Healthcare data is dynamic data. That is, it changes every moment, and it needs to be updated constantly. It's not like a legal case. It remains the same legal case forever. It's static... Do you really think that Germany is going to allow, let's call him Jean-Paul, to access and play around with individual healthcare data of their citizens?"

IQVIA was recognized by Everest Group as the only CRO to receive the #1 ranking for generative AI leadership in life sciences .

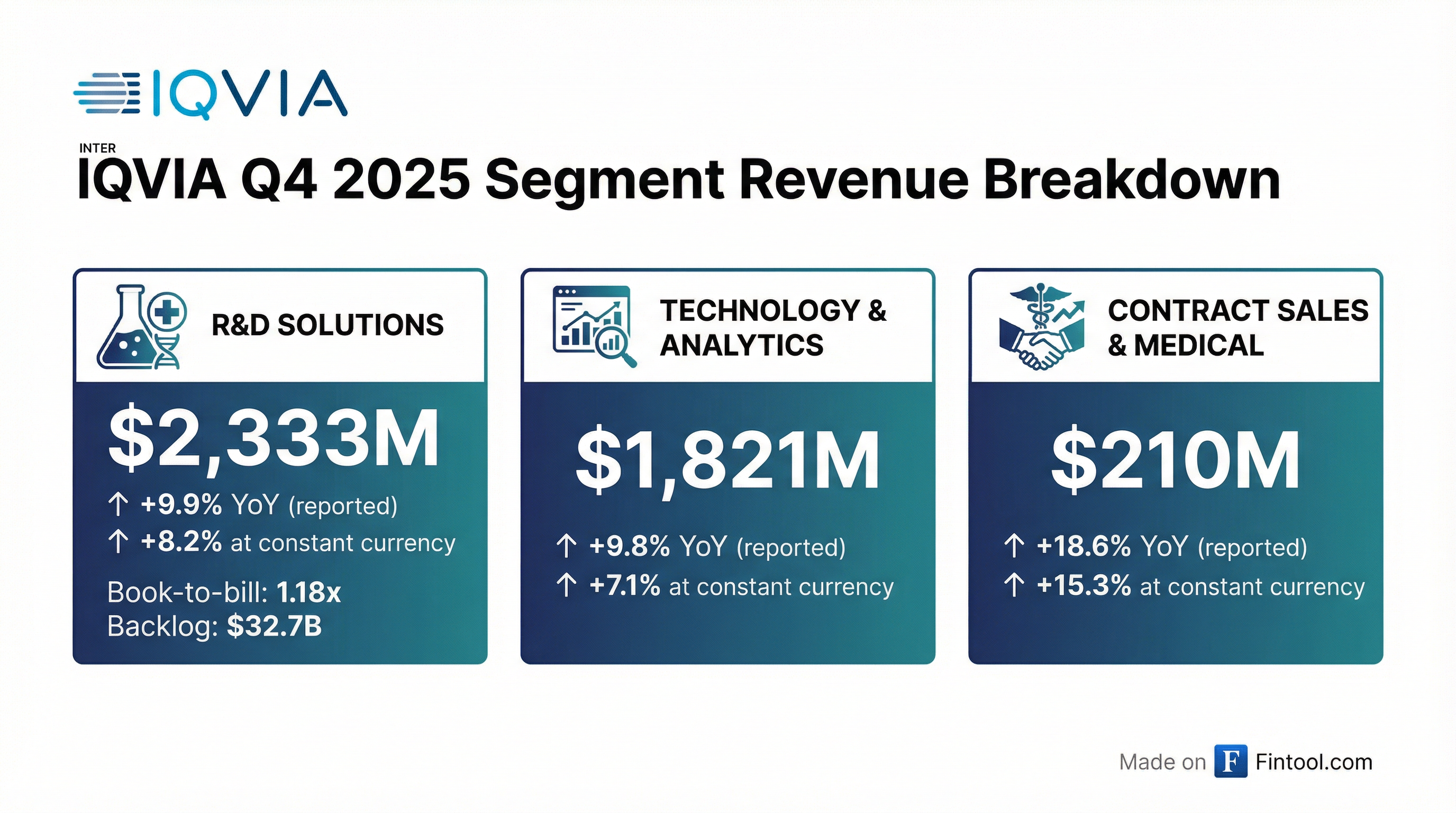

How Did Each Segment Perform?

All three business segments delivered near double-digit revenue growth on a reported basis :

R&D Solutions was the standout, with quarterly bookings exceeding $2.7 billion and a book-to-bill ratio of 1.18x . Contracted backlog grew to $32.7 billion, up 5.3% YoY (3.7% at constant currency), with approximately $8.3 billion expected to convert to revenue over the next twelve months .

Technology & Analytics benefited from sustained momentum in drug launches and strength in the broader commercial portfolio .

Contract Sales & Medical delivered the highest growth rate at 18.6%, fueled by large multi-year engagements spanning therapies and geographies .

What Did Management Guide for 2026?

IQVIA issued FY 2026 guidance slightly above street expectations on revenue but roughly in-line on EPS :

Q1 2026 Guidance :

The guidance includes approximately 150 bps of contribution from acquisitions and a ~100 bps tailwind from foreign exchange . However, management flagged a $80 million step-up in interest expense from annualization of 2025 financing activities and expected 2026 refinancing .

The slight EPS shortfall versus consensus reflects interest expense headwinds, but the revenue guide reinforces confidence in underlying demand. Q1 revenue guidance of $4.05B-$4.15B implies a modest sequential decline from Q4's $4.36B, consistent with typical seasonality.

What Changed From Last Quarter?

Several notable developments distinguish Q4 from Q3 2025:

-

Acceleration in R&D bookings: Book-to-bill improved to 1.18x in Q4 vs 1.12x trailing twelve-month, the strongest quarterly bookings of the year . However, cancellations were "slightly above the normal range due to specific idiosyncratic aspects of certain trials that had to be canceled"

-

Revenue growth acceleration: Q4 revenue grew 10.3% YoY vs 5.2% in Q3, marking the best quarter of FY 2025

-

Cedar Gate acquisition closed: Acquired Cedar Gate Technologies, a payer analytics platform, for approximately $125M revenue (2024) and ~$35M adjusted EBITDA . The deal expands IQVIA's payer/provider analytics presence in the U.S., with Cedar Gate managing 4 petabytes of data and ~60 million lives

-

Segment reorganization announced: Effective January 1, 2026, CSMS ($788M in 2025 revenue) merges into TAS (renamed "Commercial Solutions"), while Real-World Late Phase and certain other Real-World offerings ($674M) move from TAS to R&DS . On a recast basis, FY 2025 revenue was $6,740M for Commercial Solutions and $9,570M for R&D Solutions

-

CFO transition: Longtime CFO Ron Bruehlman announced transition to senior advisory role after three decades with the company . Mike Fedock, SVP of Financial Planning & Analysis, presented guidance

-

Strong FCF conversion: Full-year free cash flow of $2.05 billion represented 99% of Adjusted Net Income, demonstrating continued cash generation discipline

How Did the Stock React?

IQVIA shares traded at $202.54 as of February 5, down approximately 12% from the 52-week high of $247.05 reached in late 2025. The stock has declined amid broader market volatility, including a sharp drop on February 3 following an article about AI disruption in life sciences services that CEO Bousbib directly addressed on the call :

"An article was published a couple of days ago, and all of a sudden, it's the end of the world. I don't know why it was news to people. It certainly is not news to us."

The earnings beat may provide support as the market digests macro concerns, though shares remain well below recent highs.

Capital Allocation Update

IQVIA maintained an active capital return program while managing leverage :

As of December 31, 2025, IQVIA had $1.77 billion of share repurchase authorization remaining . The balance sheet shows gross debt of $15.7B and net debt of $13.7B, with gross leverage at 4.15x and net leverage at 3.63x trailing twelve-month Adjusted EBITDA .

Full-Year 2025 Summary

IQVIA closed FY 2025 with solid growth across all metrics :

By segment for FY 2025:

- TAS: $6,626M (+7.6% YoY)

- R&DS: $8,896M (+4.3% YoY)

- CSMS: $788M (+9.7% YoY)

Q&A Highlights

Beyond AI, analysts probed several key topics :

On large pharma AI initiatives and FSP seats:

"With respect to large pharma work on AI earlier in the process... 99% of what they mean is using AI simulation tools way upstream to try to sort through the molecules... That doesn't affect what our business is."

On margin trajectory and pass-throughs: Pass-through growth was "very strong" in Q4, the biggest driver of gross margin pressure. CFO Bruehlman noted pass-through growth will "moderate going into 2026" with guidance for flat overall EBITDA margins . SG&A margin continues to improve from productivity gains.

On book-to-bill trajectory: Bousbib pushed back on projecting specific book-to-bill ratios, but confirmed demand indicators remain "very strong" with double-digit growth in qualified pipeline and RFP flow across all customer segments . EVP funding reached $33 billion in Q4 according to Bioworld .

On productivity sharing with clients: Long-term productivity gains are shared with clients through procurement negotiations, but near-term improvements flow through to IQVIA's P&L .

Key Takeaways

-

Beat and raise (on revenue): Q4 beat consensus with the strongest quarterly growth of the year, and FY 2026 revenue guidance came in above street expectations

-

R&D momentum accelerating: Book-to-bill of 1.18x and $32.7B backlog signal continued clinical trial demand despite biotech funding headwinds

-

AI positioned as tailwind, not threat: Management forcefully defended IQVIA's AI positioning, citing proprietary healthcare data, 150+ deployed agents, and "healthcare-grade AI" domain expertise as competitive moats

-

Segment reorganization: January 2026 restructuring aligns segment reporting with operational reality, merging CSMS into Commercial Solutions

-

Cedar Gate acquisition expands payer analytics: New acquisition brings ~$140M revenue and 60 million lives of payer data to strengthen U.S. payer/provider analytics

-

Interest expense headwind: $80M higher interest expense in 2026 from financing activities weighs on EPS guidance relative to consensus

-

Strong cash conversion: 99% FCF conversion to Adjusted Net Income demonstrates disciplined working capital management

Source: IQVIA Q4 2025 8-K filed February 5, 2026