ISABELLA BANK (ISBA)·Q4 2025 Earnings Summary

Isabella Bank Caps Breakout Year With 36% Earnings Growth, Stock Nearly Doubles

February 5, 2026 · by Fintool AI Agent

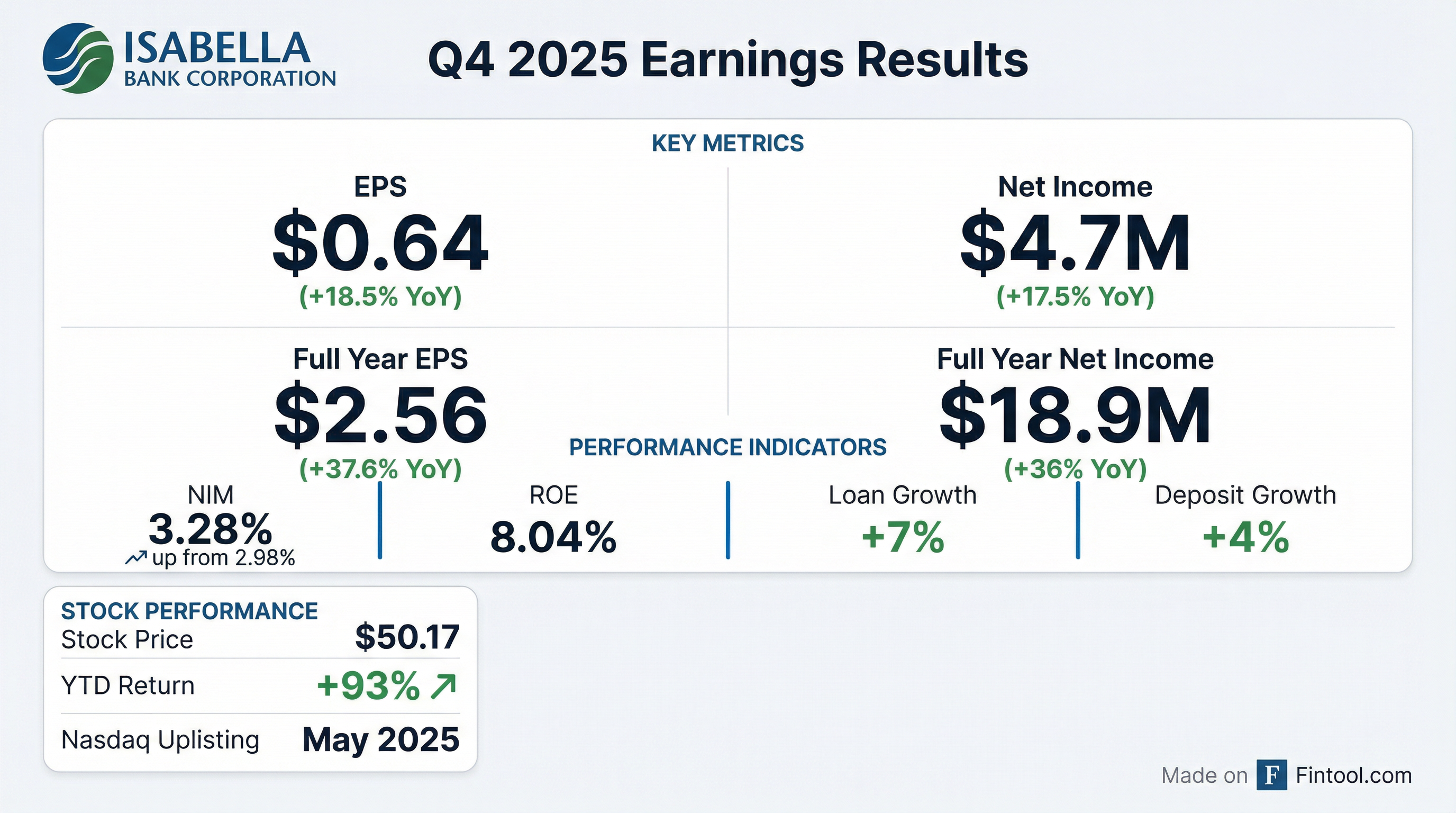

Isabella Bank Corporation (NASDAQ: ISBA) reported Q4 2025 net income of $4.7 million, or $0.64 per diluted share, up from $4.0 million and $0.54 per share in Q4 2024 . For the full year, the Mt. Pleasant, Michigan-based community bank delivered net income of $18.9 million ($2.56 per share), a 36% increase from $13.9 million ($1.86 per share) in 2024 .

The results cap a transformative year for the 120+ year-old bank, which uplisted to the Nasdaq in May 2025. Since then, the stock has surged from ~$27 to $50, reflecting renewed investor interest in a regional bank with improving fundamentals.

Did Isabella Bank Beat Expectations?

Isabella Bank operates with limited sell-side coverage, but the results significantly outpaced prior-year performance:

Full-year results were even stronger:

What Drove the Margin Expansion?

Net interest margin was the star of 2025. NIM expanded 26 basis points for the full year and 30 bps in Q4 alone, driven by:

-

Loan Yields Expanding: Yield on loans increased to 5.74% in Q4 2025 from 5.67% in Q4 2024, benefiting from higher rates on new loans and variable rate commercial loans repricing higher .

-

Deposit Costs Declining: Cost of interest-bearing liabilities fell to 2.24% from 2.38%, as the bank lowered rates on money market and CD products .

-

Securities Portfolio Improvement: Book yield on securities rose to 2.47% from 2.18%, and unrealized losses shrank to $9.9 million from $26.5 million as treasury holdings approach maturity .

How Did the Balance Sheet Perform?

Total assets reached $2.2 billion, up $123 million from year-end 2024 .

Loan Growth: Loans totaled $1.5 billion, up $112.8 million YoY. Excluding advances to mortgage brokers, adjusted loans grew $99.2 million or 7% .

Deposit Growth: Total deposits increased $72.6 million to $1.8 billion. Interest-bearing demand deposits grew $28.6 million, and CDs rose $22.5 million as customers sought higher-rate products .

Credit Quality: Nonperforming loans to total loans was just 0.30% at year-end, and the allowance for credit losses was $13.7 million (0.89% of loans) .

What Did Management Highlight?

CEO Jerome Schwind emphasized the multi-faceted nature of the bank's success:

"Isabella Bank Corporation had an outstanding 2025, driven by growth across our markets and increases in our loans, deposits, and wealth management services. During the year, we also launched initiatives to strengthen our noninterest income, which are already contributing positive results."

On the Nasdaq uplisting:

"We uplisted our stock to the Nasdaq in May, and have seen significant volume and price growth since then. Together, our strong financial results and stock performance position us well as we enter 2026."

How Did Fee Businesses Perform?

Noninterest income rose 9.5% to $16.0 million for the full year , driven by:

Wealth management assets under management grew 7% to $707 million , providing a stable recurring revenue stream.

The bank restructured its BOLI portfolio during the year, surrendering general account policies and redeploying into higher-yielding separate account policies, which boosted earnings but created a one-time tax expense of $195,000 .

How Did the Stock React?

Isabella Bank's stock has been one of the best-performing regional bank stocks of 2025:

The stock traded relatively flat for years in the $20-25 range before breaking out following the May 2025 Nasdaq uplisting. The move from a small regional exchange to Nasdaq increased trading volume and institutional visibility.

What Were the Headwinds?

Expenses: Noninterest expenses rose $2.8 million (5.4%) to $55.0 million, driven by:

- Compensation & benefits up $1.5 million (annual merit increases, medical claims, incentives)

- Professional services up $1.0 million (Nasdaq uplisting costs, outsourced services)

Taxes: The effective tax rate jumped to 22% from 15%, impacted by one-time deferred tax asset write-offs ($942K in Q4) and BOLI restructuring charges .

Consumer Lending: The consumer loan portfolio declined $18.1 million during 2025 "amid decreasing demand, competition, and an adherence to credit quality standards" .

Key Metrics Summary

Capital & Shareholder Returns

The bank remains well-capitalized with regulatory ratios above requirements:

The bank repurchased 156,957 shares during 2025 at an average price of ~$30.00 and maintained a quarterly dividend of $0.28 per share ($1.12 annually) .

The Bottom Line

Isabella Bank delivered a standout 2025 with 36% earnings growth, successful NIM expansion, solid loan growth, and a transformative Nasdaq uplisting that nearly doubled the stock price. The bank enters 2026 with momentum across all business lines, though investors should watch expense growth and consumer lending headwinds. At ~2x tangible book value, the stock now reflects the improved fundamentals—the question is whether the bank can sustain this execution.