Kyndryl Holdings (KD)·Q3 2026 Earnings Summary

Kyndryl Stock Crashes 38% Despite Earnings Beat as SEC Probe and Leadership Exodus Spook Investors

February 9, 2026 · by Fintool AI Agent

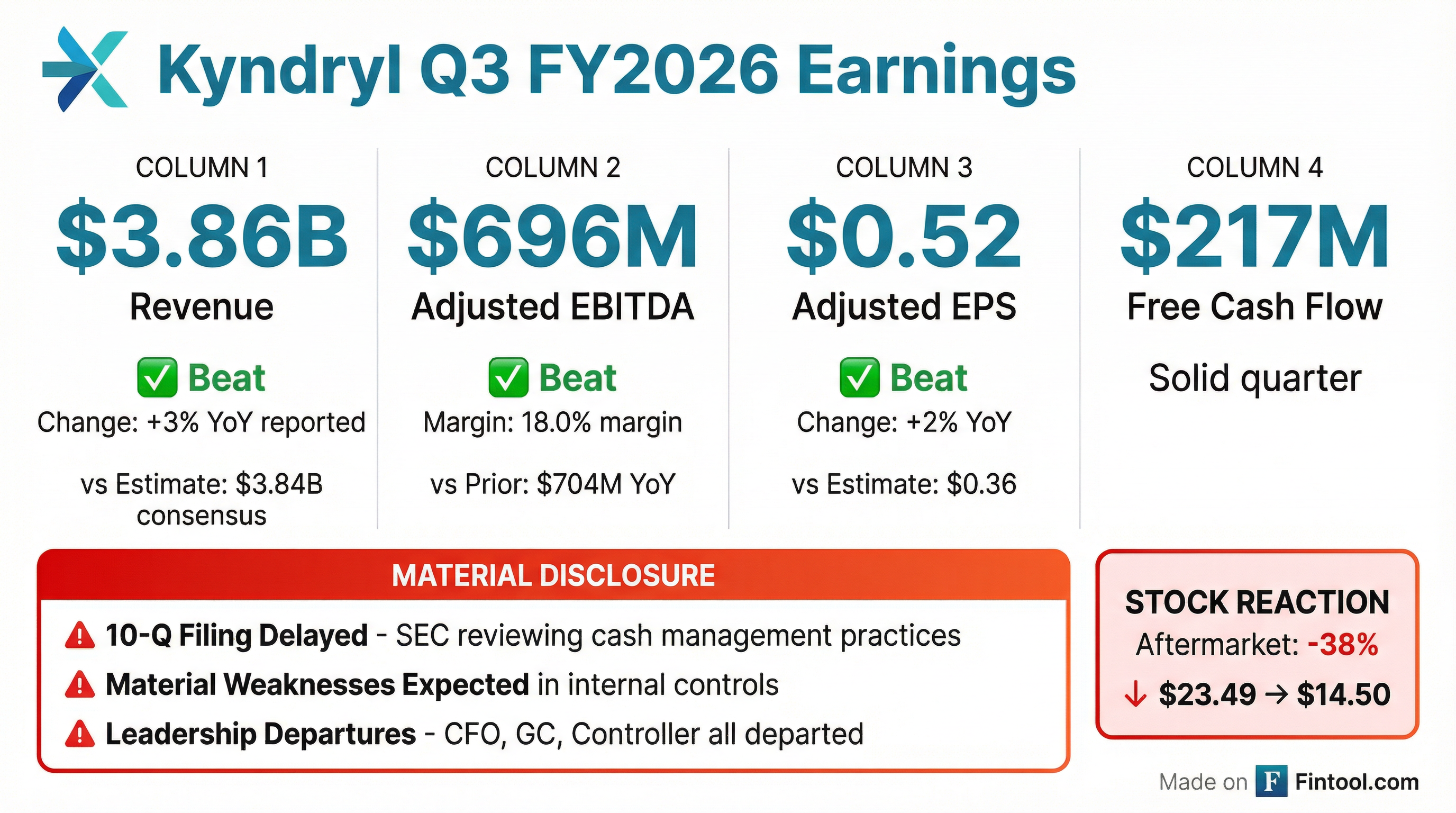

Kyndryl (NYSE: KD) delivered a solid Q3 FY2026, beating both revenue and EPS estimates while posting continued margin expansion. But the numbers were overshadowed by a bombshell: the company disclosed an SEC investigation, expected material weaknesses in internal controls, and the immediate departure of its CFO, General Counsel, and Controller. The stock plunged 38% in aftermarket trading, erasing gains from a quarter that would otherwise be considered a win.

Did Kyndryl Beat Earnings?

Yes—comfortably on the numbers that matter for the quarter:

Revenue grew 3% YoY on a reported basis (flat in constant currency), with Q3 representing the best constant-currency performance in recent quarters as the company approaches a return to growth.

The rub: GAAP EPS of $0.25 compared to $0.89 in the prior year, though that comparison is distorted by a $145M one-time gain from the divestiture of the Securities Industry Services platform in Q3 FY2025.

What Really Moved the Stock? The SEC Probe and Leadership Exodus

The earnings beat didn't matter. Here's what did:

SEC Investigation

Kyndryl disclosed that the SEC's Division of Enforcement sent "voluntary document requests" related to:

- Cash management practices

- Related disclosures (including drivers of adjusted free cash flow)

- Efficacy of internal control over financial reporting

The company filed a Form 12b-25 (NT 10-Q) indicating it cannot file its quarterly report on time pending this review.

Material Weaknesses Expected

Management anticipates reporting material weaknesses in internal control over financial reporting for:

- The current quarter (Q3 FY2026)

- The full fiscal year ended March 31, 2025

- The first two quarters of FY2026

The weaknesses are expected to include "the effectiveness and strength of certain functions at the Company, including with respect to controls related to information and communication and tone at the top."

Critically, the company stated that its prior internal control assessments and PwC's related opinion for FY2025 "should no longer be relied upon."

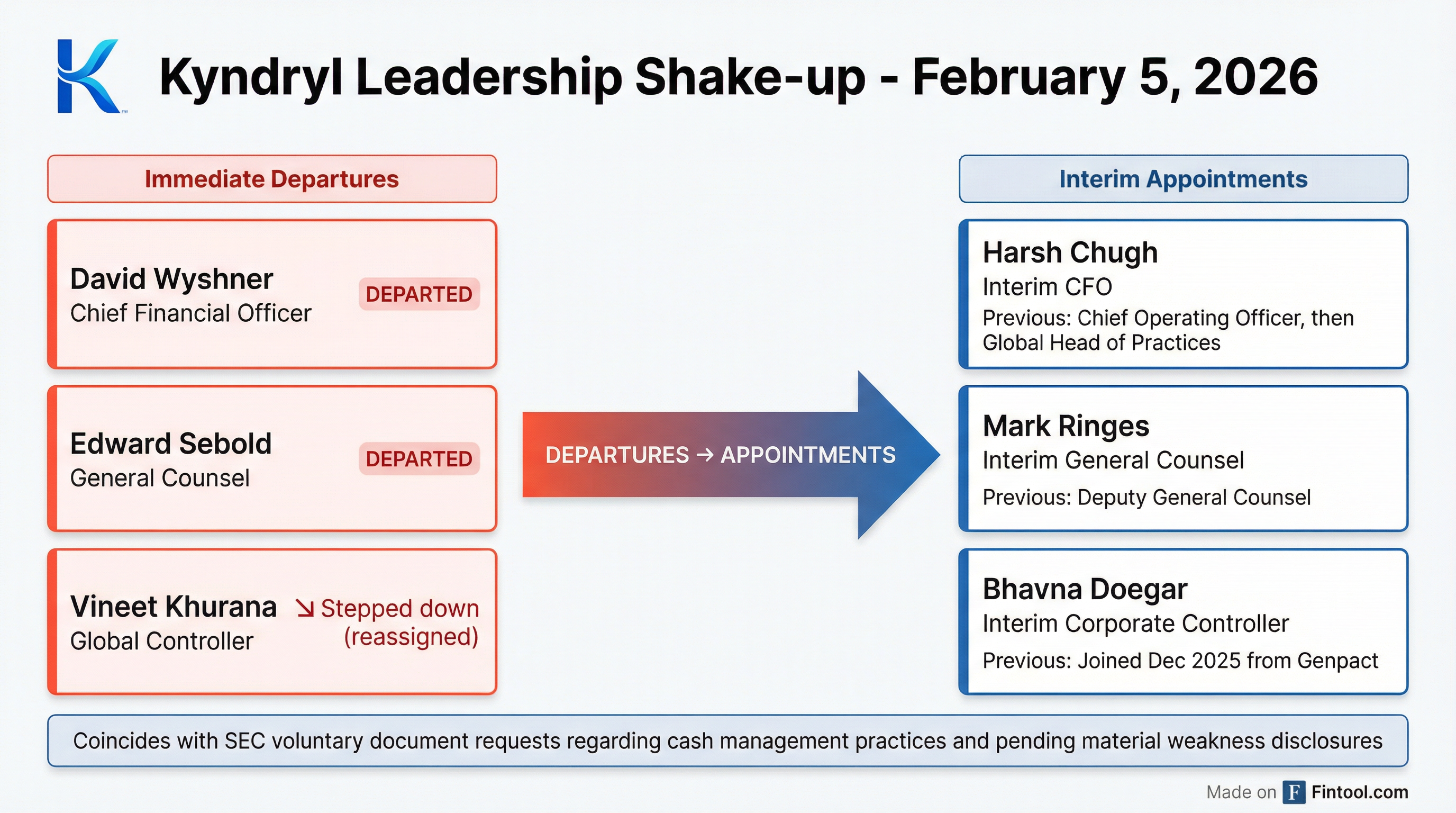

Leadership Departures

On February 5, 2026—just days before earnings—three key executives departed immediately:

The simultaneous departure of CFO, GC, and Controller—all on the same day—is a significant red flag that suggests the issues extend beyond routine accounting matters.

Stock Reaction

The aftermarket crash would take KD to new 52-week lows, wiping out approximately $2B in market cap.

The Operational Story Management Wants You to Focus On

Setting aside the governance crisis, the underlying business showed continued progress on Kyndryl's turnaround:

Growth Engines Delivering

Notable deal: 11 signed contracts exceeding $50M each in Q3, including a 5-year contract extension with Hertz to modernize IT infrastructure.

Gross Profit Book-to-Bill: The Hidden Value Story

A key metric management highlighted: gross profit book-to-bill ratio of 1.2x over the last 12 months.

This means Kyndryl is adding more gross profit to its backlog than it's currently recognizing—creating embedded future margin expansion as post-spin contracts roll through the P&L.

Segment Performance

Principal Markets (UK, Germany, France, Italy, Spain, Canada, India) drove the quarter with 10% reported growth, while Strategic Markets (rest of world) saw constant-currency declines of 7%.

What Did Management Guide?

Kyndryl revised down its FY2026 outlook from prior quarter guidance:

Key drivers of the revision: Longer sales cycles, IBM content headwinds, Consult investments taking longer to pay off, and lower attrition requiring time to adjust hiring.

The company reiterated its medium-term targets through FY2028:

Why management is confident in FY2028: Over the next two years, 90%+ of the P&L will be determined by post-spin contracts carrying high single-digit PTI margins (vs. the low/no-margin inherited contracts). Cash flow conversion remains strong—the last two years of combined profit less cash taxes essentially equals free cash flow guidance.

Management emphasized that the SEC review is "not expected to result in a restatement or other impact to financial statements"—though given the material weakness disclosures, that assurance carries less weight than it otherwise might.

What Drove the Q3 Miss vs. Expectations?

On the earnings call, management provided a candid breakdown of why the quarter came in below their prior guidance. At the start of Q3, they had expected ~6 points of acceleration from three drivers—but all three fell short:

Root causes cited:

-

Longer sales cycles: AI is causing industry disruption, making long-term infrastructure decisions more complex for customers. Data sovereignty concerns in Europe are adding regulatory uncertainty.

-

ERP cloud transitions delayed: Enterprise customers are taking longer to move ERP systems to cloud, delaying consult engagements.

-

Attrition slowdown: A "pretty dramatic slowdown in attrition" left Kyndryl with higher labor costs than planned.

-

Strategic markets weakness: Europe (a big component of Strategic Markets) saw particular softness due to data sovereignty regulatory discussions.

Management's timeline to fix:

"It'll take us a quarter to get ourselves back on track here... we know the wiring diagram works." — Martin Schroeter, CEO

The IBM Evolution Factor

A recurring headwind worth noting: the evolution of IBM content in Kyndryl's customer engagements continues to weigh on growth.

- Impact: ~3.5 percentage point adverse effect on constant-currency revenue growth

- Driver: Reduced IBM software/hardware content as Kyndryl shifts to hyperscaler and multi-vendor environments

- IBM spend trajectory: From ~$4B annualized at spinoff to ~$2B now—essentially cut in half

This is structural as Kyndryl diversifies away from its IBM heritage, but it masks underlying momentum in non-IBM work. As CEO Schroeter noted, without the IBM headwind, the core business is actually growing.

Capital Allocation

The company remained active on buybacks despite the governance overhang:

- Q3 repurchases: 3.7M shares for $100M (1.6% of outstanding shares)

- Program to date: 5% of shares repurchased since inception

- Remaining authorization: ~$350M capacity available

- Balance sheet: $1.35B cash, investment-grade rated by Moody's, Fitch, and S&P

- Net leverage: 0.7x Adjusted EBITDA (target: below 1.0x)

Liquidity moves: Kyndryl drew $1B under its revolving credit facility for "increased flexibility ahead of our seasonally higher cash outflow in our fiscal first quarter as well as for other general corporate purposes, including tuck-in acquisitions."

Management reiterated capital allocation priorities: maintain strong liquidity, remain investment grade, reinvest in the business (including tuck-in M&A), and share buybacks.

Q&A Highlights

Key exchanges from the analyst Q&A:

On the SEC review's impact on forward guidance (James Faucette, Morgan Stanley):

Management declined to comment on specifics but emphasized: "We are not changing our fiscal 2028 goals... we don't expect a restatement."

On sales cycle elongation timeline (Jonathan Lee, Guggenheim):

"Many of these deals are linked with renewals... there is a timely nature of customers and the urgency for them to sign. We're talking about a couple of quarters now."

On why FY2028 targets still hold (Jonathan Lee, Guggenheim):

CEO Schroeter: "Over the timeframes that we're talking about, more than 90% of our P&L will be determined by those high 9% PTI backlog elements as opposed to the backlog we inherited."

On free cash flow variance (James Friedman, Susquehanna):

Interim CFO Harsh Chugh: "Two components. One is the PTI that has a direct linkage—roughly about $150 million from where we were. And working capital... is going to be a bit behind for us [in Q4]."

What to Watch

-

10-Q Filing Timeline: The company must file within 5 days of the original deadline under the NT 10-Q rules, or face potential delisting concerns.

-

SEC Matter Resolution: "Voluntary document requests" can escalate—watch for any formal investigation or Wells Notice.

-

Permanent CFO Search: Harsh Chugh is interim; a permanent appointment (or lack thereof) will signal board confidence.

-

Customer Retention: Large enterprise customers may pause decisions given governance uncertainty.

-

Material Weakness Remediation: The "tone at the top" language is particularly concerning and suggests cultural/governance issues beyond process gaps.

-

Cost Base Adjustment: Management committed to "a quarter" to right-size labor costs. Watch Q4 for evidence of execution.

The Bottom Line

Kyndryl's Q3 results demonstrated continued operational progress—margin expansion, growth in Consult and hyperscaler businesses, and improving revenue trends. But none of that matters today.

The combination of an SEC investigation, expected material weaknesses, and the simultaneous departure of the CFO, General Counsel, and Controller has created a governance crisis that will take quarters to resolve. The 38% aftermarket crash reflects not just uncertainty about the SEC matter, but a fundamental breakdown in investor trust.

For existing holders, the question is whether the underlying business value—which appears intact—will survive the governance overhang. For potential investors, this is a "wait and see" situation until the scope of the SEC inquiry and internal control remediation becomes clearer.

Data sourced from Kyndryl's Q3 FY2026 earnings release, Form 8-K, NT 10-Q, earnings presentation, and earnings call transcript filed February 9, 2026. Aftermarket prices as of publication. Values retrieved from S&P Global where noted.