LEE ENTERPRISES (LEE)·Q1 2026 Earnings Summary

Lee Enterprises Q1 FY2026: EPS Miss Offset by $50M Capital Infusion and Interest Savings

February 10, 2026 · by Fintool AI Agent

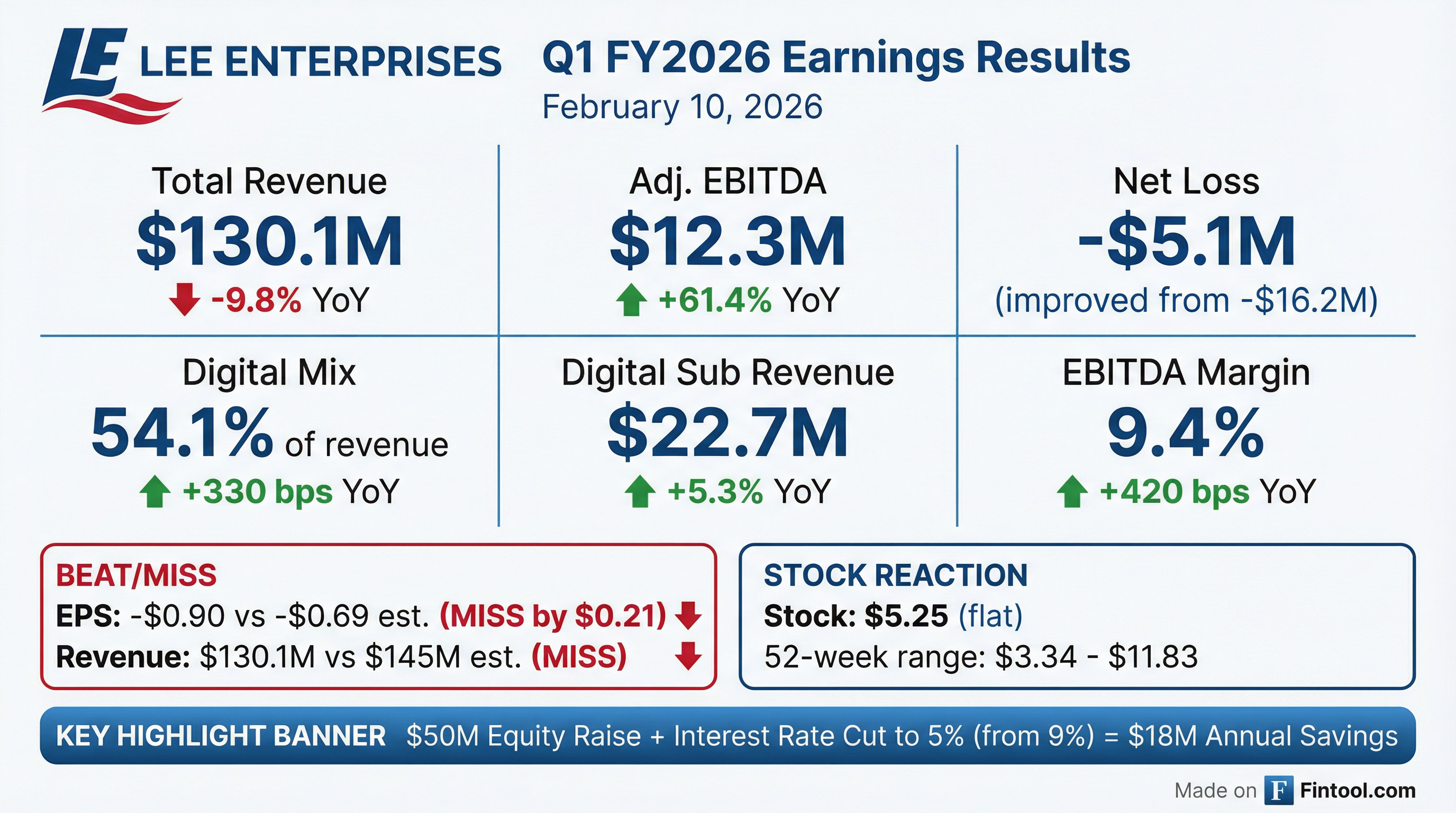

Lee Enterprises reported Q1 FY2026 results that missed Wall Street expectations on both the top and bottom lines, but the real story lies in the company's strategic recapitalization. While EPS of -$0.90 fell short of the -$0.69 consensus by 30%, a $50 million equity raise and interest rate reduction from 9% to 5% fundamentally transforms the company's free cash flow profile. Adjusted EBITDA surged 61.4% year-over-year to $12.3 million, and digital revenue now represents 54.1% of total revenue—up 330 basis points from a year ago.

Did Lee Enterprises Beat Earnings?

No. Lee missed on both EPS and revenue:

The EPS miss continues Lee's challenging streak—the company has missed consensus estimates in 8 consecutive quarters. However, the year-over-year improvement in net loss (from -$16.2M to -$5.1M) and the dramatic Adjusted EBITDA expansion suggest operational improvements are taking hold.

Important caveat: Q1 results included $2 million in business interruption insurance proceeds related to a cyber incident from last year. Excluding these proceeds, Adjusted EBITDA growth was 35% YoY rather than 61%. Management expects to receive additional insurance proceeds as FY26 progresses.

What Changed From Last Quarter?

The Recapitalization: A Game-Changer

The headline development is Lee's strategic recapitalization announced alongside Q1 results:

- $50 million equity raise through private placement at $3.25/share, anchored by investor David Hoffmann

- Interest rate reduced to 5% from 9% on outstanding debt under the Berkshire Hathaway credit agreement for five years

- ~$18 million annual interest savings based on current $455M debt outstanding

- Strategic pension plan termination in progress to eliminate long-term volatility from interest rates, mortality assumptions, and asset performance

- $26 million of non-core assets identified for monetization

This is transformational for a company that had been paying approximately $41 million annually in interest expense. The reduction to ~$23 million effectively doubles the free cash flow available for debt reduction and reinvestment.

Operational Highlights

How Did the Stock React?

Lee Enterprises shares traded relatively flat on earnings day:

The muted reaction suggests the market is weighing the EPS miss against the positive recapitalization news. The modest after-hours uptick may reflect investor appreciation for the interest savings and balance sheet improvements.

What Did Management Guide?

Lee reaffirmed FY2026 guidance for Adjusted EBITDA growth in the mid-single digits year-over-year.

Management emphasized several forward catalysts:

- Digital sustainability approaching: Digital gross margin expected to surpass SG&A costs in FY2027

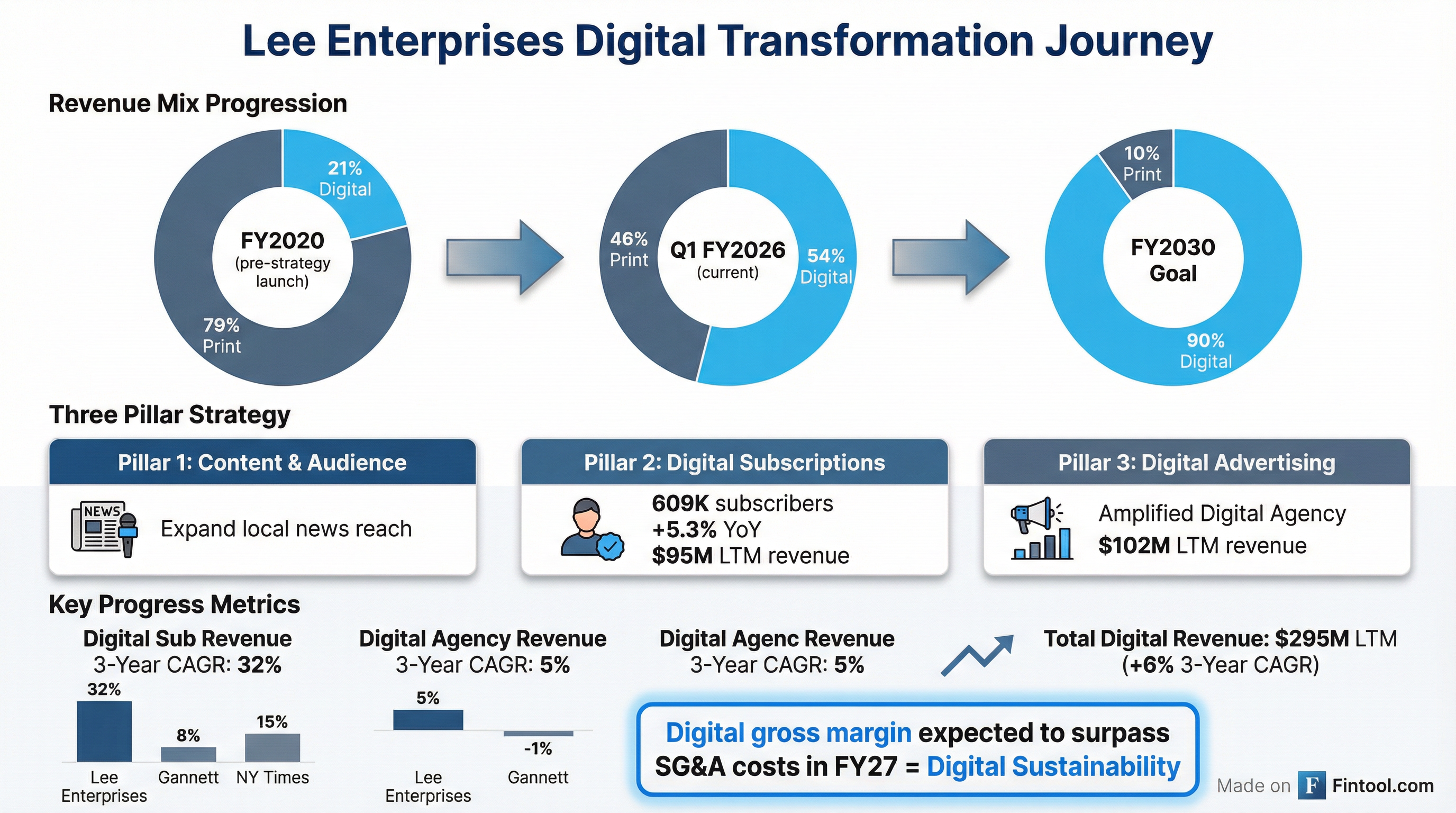

- $450M+ digital revenue by 2030: Three Pillar Strategy targets more than $450 million of digital revenue

- 90% digital mix by 2030: Transformation from 21% digital in FY2020 to current 54% to target 90%

The Digital Transformation Story

Lee continues to execute its Three Pillar Digital Growth Strategy with industry-leading growth metrics:

Digital Subscription Revenue: Industry Leader

- LTM Digital Sub Revenue: $95 million

- Digital-only subscribers: 609,000

- Q1 FY26 Digital Sub Revenue growth: +5.3% YoY (same-store)

Digital Agency Revenue: Amplified Digital®

- LTM Amplified Digital Agency Revenue: $102 million

- 71.3% of total advertising revenue now sourced from digital streams

Revenue Composition Deep Dive

Quarterly Revenue Breakdown

The print decline continues to accelerate (-15.6% YoY), but digital subscription revenue (+5.3%) provides a stable growth anchor. The key challenge is digital advertising (-8.4%), which management attributed to macro headwinds and the transition to higher-margin digital products.

Balance Sheet & Debt Profile

The Berkshire Hathaway credit agreement remains a strategic asset:

- No financial performance covenants

- No fixed amortization requirements

- No breakage costs or prepayment penalties

- 25-year runway providing significant flexibility

Cost Management: Continued Discipline

Lee executed approximately $40 million of annualized cost reductions in Q2 FY25, with an additional $10 million entering FY26.

The $17.4 million reduction in cash costs drove the dramatic Adjusted EBITDA margin expansion from 5.3% to 9.4%.

Risks and Concerns

- Persistent EPS misses: 8 consecutive quarters of missing consensus raises credibility questions

- Print decline accelerating: -19.3% print subscription decline is faster than digital growth can offset

- Digital advertising weakness: -8.4% decline in digital advertising needs to reverse

- Equity dilution: $50M raise at $3.25 dilutes existing shareholders

- Macro sensitivity: Advertising revenue remains cyclically vulnerable

Strategic Partnership: Hudl

Lee announced a new partnership with Hudl, a leader in sports technology, video analysis, and data. This represents one of the largest collaborations in local sports media:

- Scope: Hudl works with thousands of high schools and local sports teams nationwide

- Content: Partnership adds video content with free access to Lee's platforms

- Strategic fit: Aligns with Lee's mission to serve communities with high school sports coverage at the core

- Monetization: Positions Lee's digital platforms as the destination for local sports consumption and advertising

Management noted the partnership is in early stages but expressed strong enthusiasm about the collaboration.

Forward Catalysts

Q&A Highlights

The Q1 FY2026 earnings call had no questions from webcast participants. Management closed with remarks reiterating the company's digital-first transformation and the transformational impact of the $50 million private placement and interest rate reduction.

Key Takeaways

- EPS miss, but improving: -$0.90 vs -$0.69 estimate, though losses narrowed significantly from prior year

- Recapitalization is transformational: $50M equity + 5% interest rate = ~$18M annual savings

- Digital transformation on track: 54% digital mix, 609K digital subscribers, industry-leading growth rates

- Cost discipline continues: $17M cash cost reduction YoY, 420 bps EBITDA margin expansion

- Guidance reaffirmed: Mid-single digit Adjusted EBITDA growth for FY2026

- FY2027 inflection point: Digital sustainability (gross margin > SG&A) expected next year

Related: LEE Company Profile | Q4 FY2025 Earnings | Earnings Transcripts