LOUISIANA-PACIFIC (LPX)·Q4 2025 Earnings Summary

LP Building Solutions Q4 2025 Earnings: Beats Own Guidance Despite OSB Collapse; New CEO Takes Helm

February 17, 2026 · by Fintool AI Agent

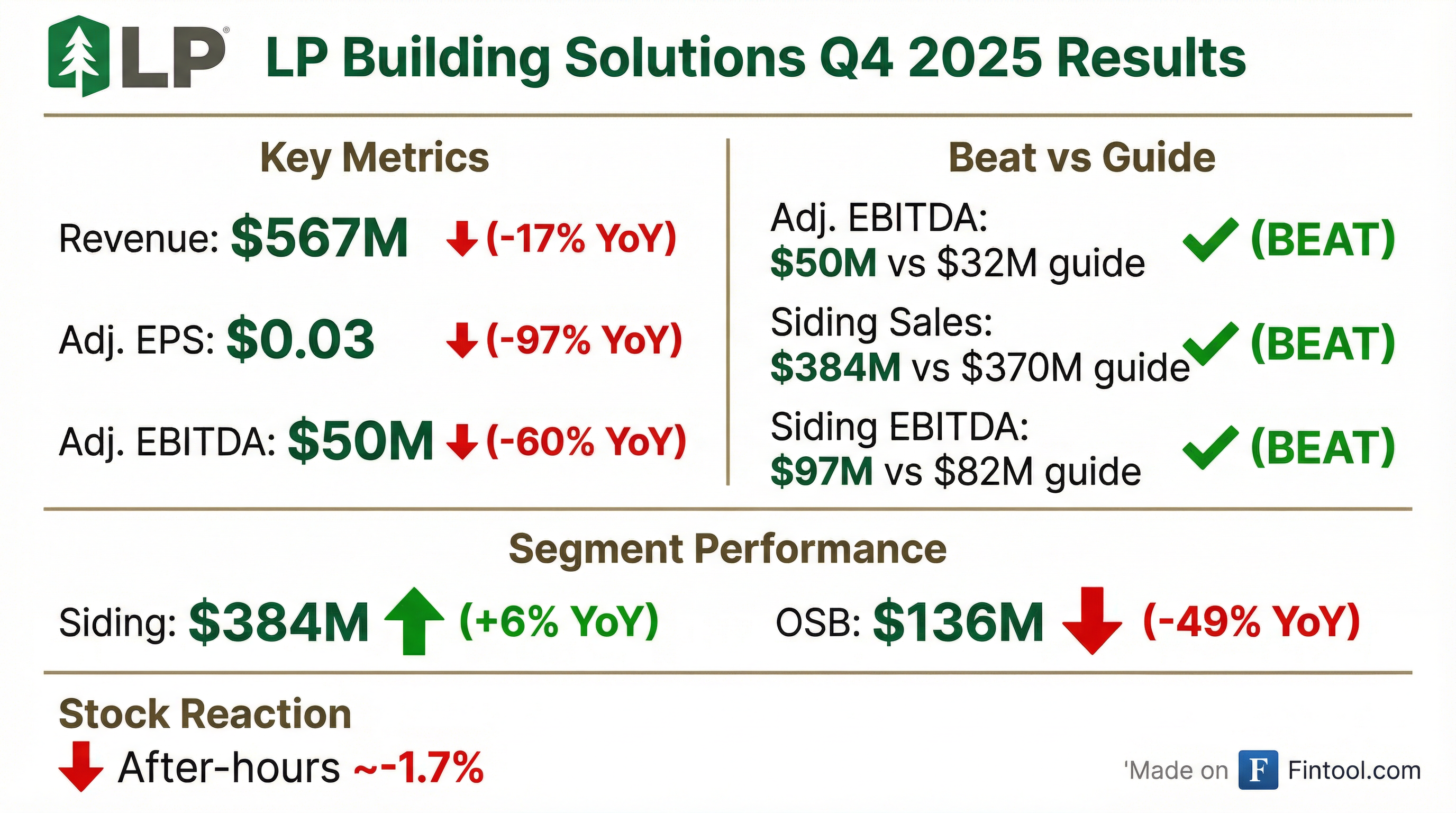

LP Building Solutions delivered a tale of two businesses in Q4 2025: the Siding segment continued its strong execution with 6% revenue growth and a 33% Adjusted EBITDA increase, while the OSB segment saw revenue collapse 49% on plummeting commodity prices. Despite the challenging OSB environment, the company handily beat its own guidance across all major metrics and raised its quarterly dividend by 7%.

Leadership transition: New CEO Jason Ringblom took the helm from Brad Southern, who retired after 25+ years of transformative leadership. Ringblom emphasized LP's commitment to "driving growth, gaining market share, delivering product and process innovation, and generating shareholder value."

Did LP Building Solutions Beat Earnings?

The short answer: Beat on adjusted EPS, missed on revenue, crushed company guidance.

LP significantly outperformed its own guidance from November, with consolidated Adjusted EBITDA coming in at $50M versus the $32M guide—a 56% beat. The Siding segment was the star, delivering $97M in Adjusted EBITDA versus the $82M guided, driven by better-than-expected pricing and mix.

What Changed From Last Quarter?

The divergence between LP's two business segments accelerated dramatically:

Siding (68% of Q4 revenue): Continued momentum with 6% revenue growth YoY driven by 8% higher average selling prices, partially offset by 2% lower volumes. ExpertFinish pre-finished siding now represents 17% of segment net sales, up from 16% in the prior year, contributing to favorable mix. Adjusted EBITDA margin improved to 25% from 20% in Q4 2024. ExpertFinish volumes jumped 35% YoY in Q4, with margins improving ~8 points due to volume leverage and manufacturing efficiencies.

Shed segment outperformance: For full-year 2025, shed volumes were up ~20%+ YoY, significantly outpacing other end markets. However, this included a pull-forward effect as distributors built inventory ahead of LP's 2026 price increase. New products launched for 2026—Everyday Flooring series and SilverTech Roofing—target continued shed growth once channel inventories normalize.

OSB (24% of Q4 revenue): A collapse in commodity prices drove a 49% revenue decline. Average selling prices fell 25% for structural solutions and 40% for commodity OSB, while volumes declined 24-27%. The segment posted a $(39)M Adjusted EBITDA loss versus $50M profit in Q4 2024. CEO Ringblom noted that at their trough, "OSB prices, adjusted for inflation, are the lowest we've seen in 20 years at LP."

What Did Management Guide for 2026?

LP provided Q1 2026 and full-year 2026 guidance that shows continued Siding strength but a weak OSB recovery:

The Q1 outlook reflects typical seasonality with Siding sales expected down ~12% YoY. However, management expects full-year Siding revenue to grow ~2% with strong margins around 26%. OSB is expected to reach breakeven for the full year, assuming OSB prices remain at February 13, 2026 levels.

Inflation headwinds baked into guidance: CFO Haughie disclosed that the Siding margin outlook already incorporates significant cost inflation—$20M in raw materials (resin and paper overlay, largely contractual), $7M in labor, plus modest freight increases.

Capital expenditure guidance of $400M is split evenly between strategic growth and sustaining maintenance projects, indicating continued investment in capacity expansion.

What Did Analysts Ask About?

The earnings call Q&A revealed several investor concerns and management responses:

Channel Inventory Issues: Management disclosed that two-step distribution partners have 2-4 weeks of excess inventory due to a volume allocation ahead of LP's 2026 price increase that was "somewhat larger than necessary." Combined with dealer caution on working capital, this led to weaker-than-expected order files entering 2026. Management expects inventory to normalize by Q2 as seasonal building demand returns.

Q1 Volume Breakdown: Analysts pressed on the weak Q1 outlook. Management provided granular detail:

- Total Siding volumes: down 15-20% YoY

- Shed volumes: down 25-30% YoY (largest drag)

- New residential construction & R&R: down 10-15% YoY (tracking housing starts)

ExpertFinish Off Allocation Early: A positive surprise—LP came off managed allocation for ExpertFinish on February 1, ahead of the Green Bay facility ramp in Q2. This was driven by OEE improvements across the network.

Affordability & Vinyl Competition: When asked about potential trade-down to vinyl siding, CEO Ringblom acknowledged "a little bit of a move to vinyl" but emphasized SmartSide's broad product offering and value proposition. With LP's relatively low market share, he sees "plenty of opportunities to continue on our growth trajectory."

Geographic Trends: Demand remains stronger in the Upper Midwest where LP has higher market penetration, while the Southeast and Texas remain softer. This regional divergence partially insulated LP from the worst of the housing weakness.

OSB Market Dynamics: CFO Alan Haughie noted that the recent OSB price rebound is largely supply-driven (Canadian mill closures, maintenance outages, winter storm disruptions) rather than demand-driven. Management cautioned that demand improvement will be needed to sustain balance through Q2/Q3.

How Did the Stock React?

LPX closed at $93.62 on February 13, 2026 (the last trading day before the release). In after-hours trading following the announcement, shares declined to approximately $92, representing a ~1.7% drop.

The muted reaction likely reflects: (1) the revenue miss versus consensus, (2) continued OSB weakness, offset by (3) strong Siding execution and (4) the dividend increase providing a floor for the stock.

Year-to-date performance: LPX has traded between $73.42 (52-week low) and $113.12 (52-week high), with the current price roughly in the middle of that range.*

Full Year 2025 Results

The full-year picture shows the transformation underway at LP:

Siding delivered $131M of revenue growth (+8%) driven by 4% volume increases and 4% price increases. OSB saw $352M of revenue decline primarily due to commodity price weakness.

Capital Allocation Update

LP maintained its shareholder-friendly capital allocation priorities:

- Dividend increase: Quarterly dividend raised 7% to $0.30/share from $0.28/share

- Share repurchases: $61M spent to repurchase 0.6M shares in 2025; $177M remaining authorization

- CapEx: Invested $291M in 2025; guiding $400M for 2026 (50% growth, 50% maintenance)

- Liquidity: ~$1B total liquidity as of December 31, 2025

- Balance sheet: Total debt of $348M, stockholders' equity of $1.7B

The increased CapEx guidance for 2026 suggests LP is investing through the cycle to expand Siding capacity ahead of an expected housing recovery.

Green Bay expansion: LP is ramping a new 70 million square foot ExpertFinish line in Green Bay, Wisconsin in early Q2 2026. Management noted detailed engineering work continues on additional ExpertFinish and primed capacity projects, with a "heavy bent towards being early versus late" on timing.

Portfolio solutions strategy: LP's organizational integration under a chief commercial officer and chief operating officer structure (vs. separate business GMs) is enabling new sales synergies—the company has secured "a couple of builder wins" by leveraging the combined OSB + Siding portfolio, with more expected.

Key Operational Metrics

LP provided several KPIs that highlight operational improvements:

Overall Equipment Effectiveness (OEE) improved in both segments, indicating better asset utilization even as volumes declined. The Siding segment showed particular improvement in Q4 with OEE reaching 78% versus 75% in Q4 2024.

Risks and Concerns

Several factors warrant monitoring:

-

OSB price sensitivity: Full-year guidance assumes OSB prices remain flat from February 13, 2026 levels. Any further decline would pressure results.

-

Housing starts weakness: US housing starts were 1.36M in 2025 versus 1.37M in 2024, and single-family starts declined from 1.01M to 949K. Continued softness could limit Siding growth.

-

Tariff exposure: LP called out $7M of tariff expenses in Siding for 2025. Trade policy uncertainty remains a risk.

-

Impairment charges: The company recorded $44M in impairment charges for full-year 2025 versus just $5M in 2024.

The Bottom Line

LP Building Solutions delivered a mixed Q4 2025 but demonstrated the resilience of its strategic pivot toward the higher-margin, less cyclical Siding business. While OSB remains challenged by commodity price weakness, the Siding segment continues to deliver strong execution with 8% revenue growth and expanding margins for the full year.

The 7% dividend increase signals management's confidence in the business, and the $1B liquidity position provides ample flexibility. The key question for 2026 is whether housing activity recovers enough to support the guided 2% Siding growth and OSB breakeven—both of which assume stable-to-improving market conditions.

*Values retrieved from S&P Global

Related: LPX Company Profile | Q4 2025 Transcript | Q3 2025 Earnings