LATAM AIRLINES GROUP (LTM)·Q4 2025 Earnings Summary

LATAM Airlines Q4 2025 Earnings: Revenue Beat, Record Margins Power 78% Profit Surge

February 04, 2026 · by Fintool AI Agent

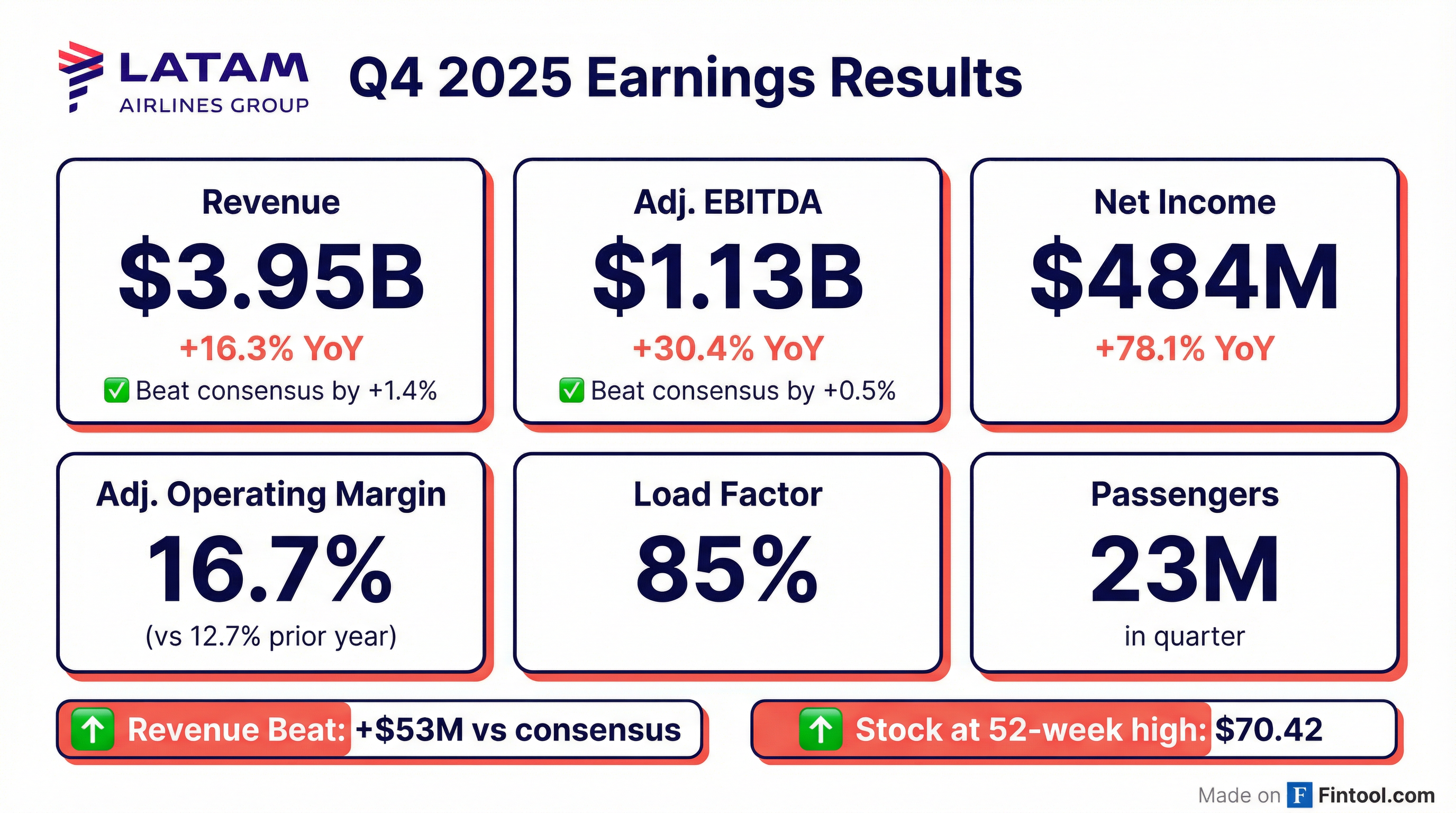

LATAM Airlines delivered a strong finish to 2025, beating revenue and EBITDA consensus while posting its highest quarterly net income margin (12.2%) on record . The South American carrier generated $484M in Q4 net income (+78% YoY) on $3.95B in revenue (+16% YoY), driven by disciplined capacity deployment and premium revenue growth . Shares are trading near their 52-week high of $70.42, reflecting investor confidence in LATAM's structural transformation.

Did LATAM Beat Earnings?

Yes — both revenue and EBITDA exceeded consensus.

Values retrieved from S&P Global

LATAM has now beaten revenue consensus in 6 of the last 8 quarters. The Q4 beat was driven by passenger revenue growth of 20.3% YoY, supported by strong load factors (85%) and a 7.7% capacity increase .

What Drove the Beat?

Three factors powered Q4 outperformance:

1. Unit Revenue Outpaced Unit Costs Passenger RASK (revenue per available seat kilometer) increased 11.7%, more than offsetting a 7.9% increase in CASK ex-fuel . Management noted ~$0.002 of the CASK increase was one-time (special bonus) and ~$0.002 from currency appreciation .

2. Premium Revenue Momentum Premium revenues accounted for 23% of passenger revenues and grew 14% YoY vs. 12% for total passenger revenues . The LATAM Pass loyalty program now has 54 million members representing ~60% of passenger revenues .

3. Network Strength Across All Segments

- Brazil domestic: +12% capacity, +14% RASK in USD

- Spanish-speaking domestic: +23% RASK in USD, +1.7pp load factor improvement

- International: High single-digit growth, 85% load factor, +6% unit revenues

Full Year 2025 Performance

2025 marked a transformational year for LATAM with record profitability:

CEO Roberto Alvo emphasized the structural nature of results: "These results are the product of a model that LATAM Group has been building over the last six years, anchored first in the people and the customers, focused on impeccable execution" .

What Did Management Guide for 2026?

LATAM's 2026 guidance signals continued profitable growth despite fuel and currency volatility:

Fleet expansion is accelerating: 41 aircraft deliveries expected in 2026 (vs. 26 in 2025):

- 3 Boeing 787 Dreamliners (with GEnx engines)

- 12 Embraer E2s (first of the type, for Brazil domestic)

- 26 Airbus A320 family aircraft

Capital Allocation: What's the Shareholder Return Outlook?

LATAM's financial policy creates significant flexibility for returns:

In December 2025, LATAM distributed $400M in interim dividends — an acceleration of the statutory 30% minimum that typically pays in April . The board will evaluate additional capital allocation opportunities and update the market accordingly .

Balance sheet strength supports flexibility:

- Net leverage: 1.5x (vs. 2.0x policy maximum)

- Cost of debt: 6.6% (down from 10.7% in 2023)

- Debt nearly 100% USD-denominated

How Did the Stock React?

LTM shares have been on a tear heading into earnings:

Values retrieved from S&P Global

The stock touched its 52-week high of $70.42 on February 3, the day before earnings, reflecting optimism about structural improvements. Pre-earnings run-ups often indicate results were at least partially priced in.

What Changed From Last Quarter?

Positive shifts:

- Net income margin expanded to 12.2% (vs. 10.0% in Q3) — new quarterly record

- Liquidity guidance raised to >$5B for 2026 (was $3.7B at Q3)

- NPS hit record 54 points (+3 vs. 2024)

- Organizational Health Index reached 83 (top decile globally)

Watch items:

- Cargo revenue -9.6% YoY (tough Q4 2024 comp)

- Net debt increased to $5.9B (+6% QoQ) due to $400M dividend acceleration

- Chile domestic was "a little bit slower" in late 2025 (but recovering in early 2026)

Key Q&A Highlights

On currency impact (CEO Roberto Alvo): "A stronger local currency is more positive than a weaker local currency... domestic markets work like import industries. In international, purchasing power for traveling abroad is higher when currencies appreciate" .

On premium strategy vs. competition: "It all starts with people. You are not going to be able to attract premium customers only with hardware. You need software... the DNA of this organization and the people, I think, is unmatchable" .

On Brazil market outlook: "Brazil was, out of the 10 largest domestic markets in the world, the one that grew the most in 2025... we see potential for development of our strategy" .

On E2 deployment: The first 12 Embraer E2s will be based in Brazil out of Guarulhos, Brasília, and Fortaleza hubs, enabling new routes and increased frequencies where A319/A320 economics don't work .

Forward Catalysts

Bottom Line

LATAM Airlines delivered another quarter of disciplined execution — revenue and EBITDA beats, record net income margin, and 2026 guidance that signals the structural turnaround is sustainable. With shares at 52-week highs, the key question is whether valuation now reflects the transformation. Management's confidence in maintaining 15-17% operating margins while growing capacity 8-10% and generating >$1.7B in free cash flow will be tested throughout 2026.