MoonLake Immunotherapeutics (MLTX)·Q4 2025 Earnings Summary

MoonLake Surges on Positive Phase 2 axSpA Data, Stock Jumps 8% After Hours

February 23, 2026 · by Fintool AI Agent

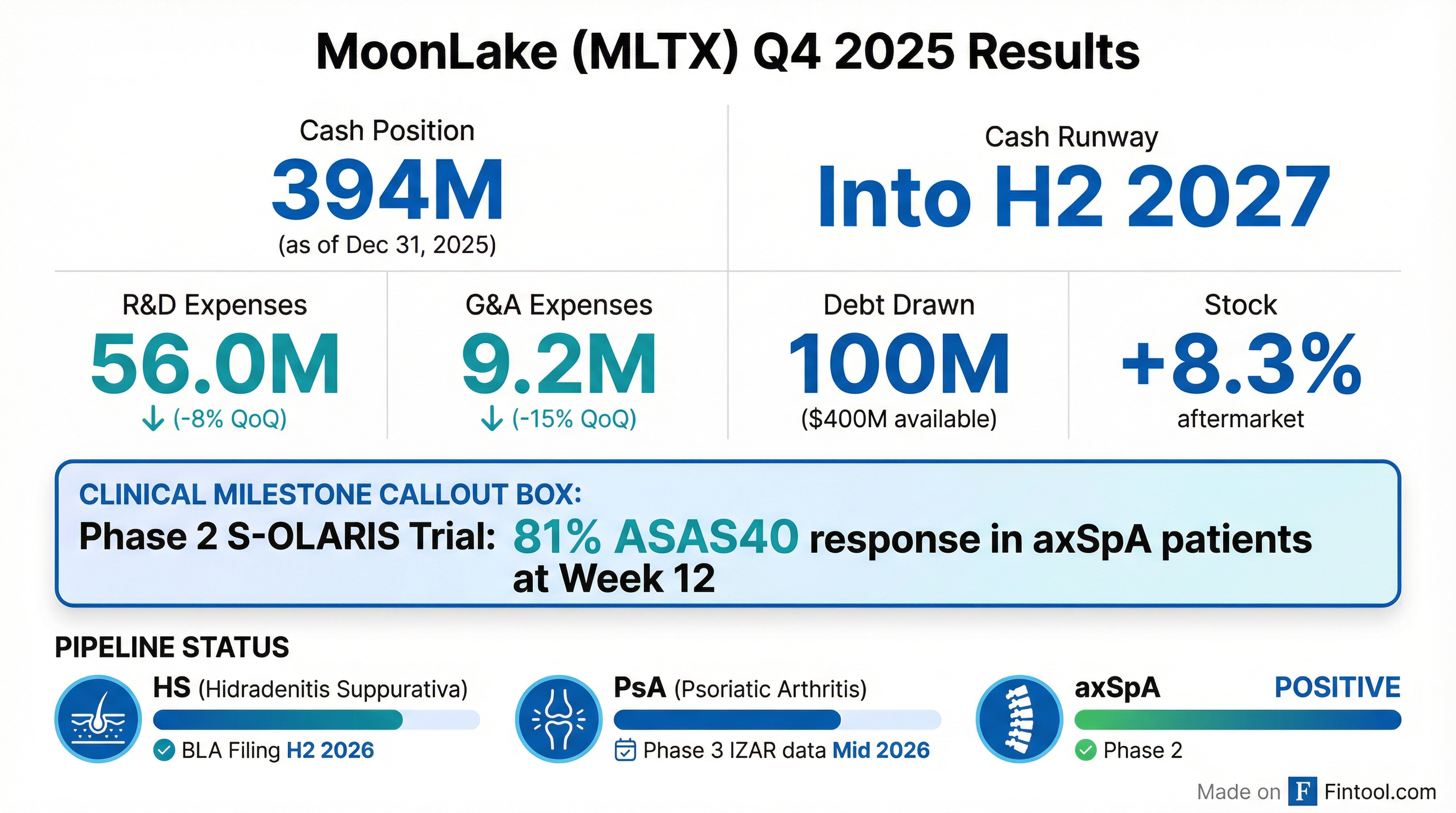

MoonLake Immunotherapeutics delivered a catalyst-rich Q4 2025 update, headlined by positive Phase 2 data in axial spondyloarthritis (axSpA) and an extended cash runway. The clinical-stage biotech reported 81% of patients achieved ASAS40 response at Week 12 in its S-OLARIS trial, while maintaining a strong $394 million cash position with access to up to $400 million in additional non-dilutive debt .

Did MoonLake Report Positive Clinical Data?

Yes—and it was the headline driver. The Phase 2 S-OLARIS trial in axSpA showed:

This represents sonelokimab's fifth indication with positive clinical data across Phase 2 and Phase 3 trials . The PET imaging data showing reduced osteoblast activity is particularly notable—it suggests potential for disease modification in axSpA by targeting the irreversible ossification process that causes mobility restriction .

"The combination of clinical, imaging, and biomarker data presents one of the clearest demonstrations to date of how targeting IL-17A and IL-17F with a Nanobody can meaningfully reduce inflammation in the axial structures." — Prof. Xenofon Baraliakos, President of EULAR

What is MoonLake's Cash Position?

The sequential increase in cash despite continued R&D spending was supported by a $75 million equity raise (gross proceeds) earlier in the quarter . Combined with available debt, MoonLake has runway into H2 2027 .

What Changed With the Debt Facility?

MoonLake amended its Hercules Capital loan agreement on February 20, 2026, drawing an additional $25 million and modifying future tranche milestones :

Total facility: $500M | Drawn: $100M | Available: $400M

The facility matures April 1, 2030 with interest at prime + 1.45% (floor 8.45%) .

How Did the Stock React?

The stock has recovered sharply from early February lows near $15, driven by anticipation of clinical catalysts. The after-hours move suggests the axSpA data exceeded expectations.

Stock is trading at 22.6% of its 52-week range, well below the $62.75 peak from early 2025—likely reflecting broader biotech sector weakness and the September 2025 VELA-2 mixed results.

What Are the Upcoming Catalysts?

An Investor Day was held today (February 23) at 8:00 AM ET where management discussed the axSpA data, FDA Type B meeting outcomes for HS, and 2026 outlook .

What About the Board Changes?

Simon Sturge notified the Board of his resignation effective February 28, 2026 . His departure was not due to any dispute with the company. In response:

- Dr. Jorge Santos da Silva appointed Interim Chair of the Board

- Spike Loy appointed Lead Independent Director

The Board will reduce from six to five directors .

What Changed From Last Quarter?

The reduced R&D spending in Q4 may reflect timing of clinical trial expenses rather than a structural change—management noted continued ramp-up for BLA preparation .

Key Risks to Monitor

-

VELA-2 Overhang: The September 2025 VELA-2 trial narrowly missed statistical significance using the composite strategy (p=0.053) . The upcoming 52-week data needs to demonstrate durability.

-

Dilution Risk: Despite non-dilutive debt, the company may require additional equity financing beyond H2 2027 if commercial launch is delayed.

-

Competitive Landscape: IL-17 inhibitors from J&J (Tremfya), Novartis (Cosentyx), and others are established in the market.

-

Tariff Exposure: Management noted potential supply chain impacts from evolving trade policy .

The Bottom Line

MoonLake delivered a strong Q4 with positive axSpA data representing the fifth clinical win for sonelokimab. The company's financial position is solid with $394M cash and $400M in available debt, providing runway to potential HS approval. The 2026 catalyst calendar is packed with four major data readouts and a BLA submission—any of which could significantly move the stock from current levels 77% below its 52-week high.

Key numbers to watch:

- 81%: ASAS40 response rate in axSpA (vs. historical IL-17 benchmarks of 40-50%)

- $394M: Cash position

- H2 2027: Cash runway

- H2 2026: Expected HS BLA submission

Data sources: MoonLake 8-K filed February 23, 2026; Q3 2025 10-Q; market data as of February 20, 2026.