MERIT MEDICAL SYSTEMS (MMSI)·Q4 2025 Earnings Summary

Merit Medical Extends EPS Beat Streak to 9 Quarters, Stock Up 1.4%

February 24, 2026 · by Fintool AI Agent

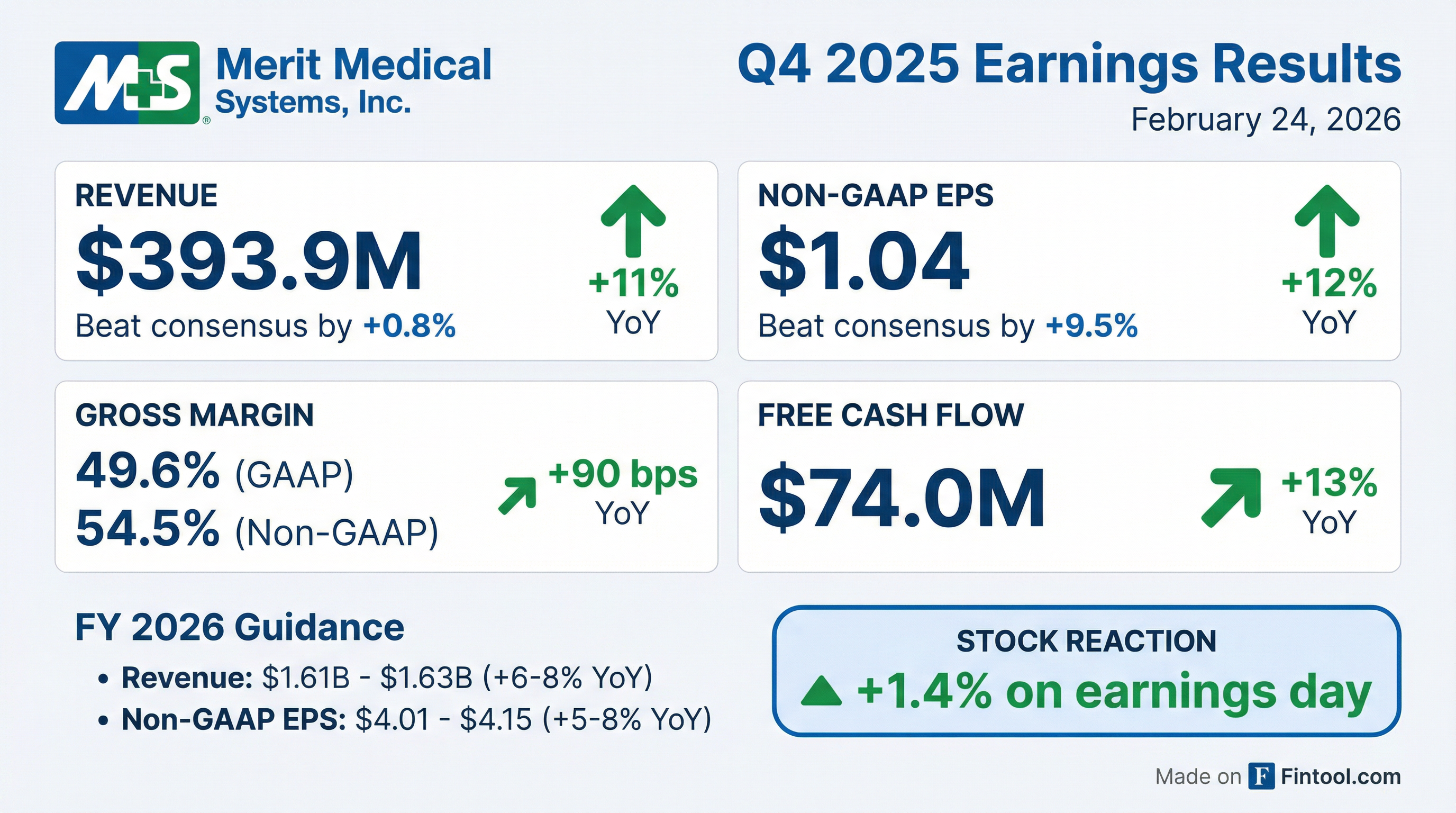

Merit Medical Systems (NASDAQ: MMSI) delivered another beat-and-raise quarter, posting Q4 2025 revenue of $393.9 million (+11% YoY) and Non-GAAP EPS of $1.04 (+12% YoY), both ahead of consensus estimates. The medical device manufacturer extended its quarterly EPS beat streak to nine consecutive quarters while guiding FY 2026 above the Street's expectations.

Did Merit Medical Beat Earnings?

Merit Medical beat on both top and bottom lines for Q4 2025:

The revenue beat was driven by double-digit growth in Cardiac Intervention (+23% YoY) and Peripheral Intervention (+15% YoY), which together represent over 70% of total revenue. On a constant currency organic basis, revenue grew 6.6%—excluding contributions from the C2 Acquisition, Biolife Merger, and Cook Transaction.

Margin expansion continued to be a key theme. Non-GAAP operating margin reached 21.0% (vs. 19.6% in Q4 2024), driven by gross margin improvement and operating leverage.

What Did Management Say?

CEO Martha Aronson highlighted the strength of the quarter and the team's progress on strategic initiatives:

"Merit delivered better-than-expected revenue and financial results in the fourth quarter. Our fourth quarter capped off an impressive year of operating and financial performance in 2025; we delivered 6.8% organic, constant currency revenue growth, a 130 basis-point improvement year-over-year in our non-GAAP operating margin and generated strong free cash flow of more than $215 million, a 16% increase year-over-year."

Management emphasized continued focus on the final year of the Continued Growth Initiatives Program and reaffirmed confidence in hitting the three-year targets ending December 31, 2026.

How Did Segments Perform?

Source:

Cardiac Intervention (+23%) was the standout, benefiting from the Cook Transaction closed in November 2024 and continued procedure volume recovery. Peripheral Intervention (+15%) maintained strong momentum with its vascular access and intervention portfolio.

The OEM segment declined 15% due to timing of orders and the reclassification of spine device revenues into this category for comparability purposes.

How Did Geographic Regions Perform?

Merit Medical generates ~40% of revenue internationally, with strong double-digit growth in EMEA and continued U.S. strength:

Q4 2025 Regional Performance:

Source:

FY 2025 Regional Performance:

Source:

U.S. (+12% CC in Q4) remains the core growth driver, representing 60% of total revenue with strong procedure volume trends. EMEA (+12.3% CC) benefited from market share gains and acquisition contributions. APAC (+2.6% CC) showed more modest growth, while Rest of World (-4.5% CC) reflected timing of distributor orders.

What Did Management Guide?

For FY 2026, Merit Medical issued guidance above consensus expectations:

Source:

Guidance assumes a ~0.8% FX headwind, translating reported growth of 6-8% to constant currency growth of 5-7%. Management noted guidance excludes potential impacts from trade policies or tariffs implemented after the report date.

The midpoint of EPS guidance ($4.08) implies continued margin expansion, consistent with the Continued Growth Initiatives Program targets.

How Did the Stock React?

MMSI shares rose 1.4% on the earnings release to $82.43, with trading volume at 1.6x the 20-day average. The muted reaction reflects a stock that has already pulled back significantly—down 22% over the past year and 4.7% YTD—despite consistent operational execution.

The stock's 9-quarter EPS beat streak hasn't been enough to drive sustained multiple expansion, as healthcare equipment names have broadly de-rated on macro concerns and GLP-1 headwinds affecting certain procedure volumes. Merit's valuation at ~12x forward P/E appears conservative relative to its consistent execution.

What Changed From Last Quarter?

Several notable shifts from Q3 2025:

-

Margin improvement accelerated: Non-GAAP operating margin hit 21.0% in Q4 vs. 19.3% in Q3, driven by seasonal mix and operating leverage.

-

Free cash flow surge: Q4 FCF of $74M (+13% YoY) reflected strong working capital management; FY 2025 FCF of $215.7M (+16% YoY) demonstrates cash generation capability.

-

Balance sheet strengthening: Cash increased to $446.4M from $376.7M a year ago, with total debt unchanged at $747.5M and ~$697M of available borrowing capacity.

-

Acquisition integration progressing: Contributions from Biolife (May 2025), C2 CryoBalloon (November 2025), and Cook Transaction (November 2024) are being integrated on schedule.

Full Year 2025 Results

Source:

Capital Allocation

Merit Medical continues to prioritize:

- Organic reinvestment: CapEx of $81.7M in FY 2025 (vs. $35.1M in FY 2024), reflecting capacity expansion

- Tuck-in M&A: Three acquisitions closed in 2025 (Biolife, C2 CryoBalloon, Cook assets) expanding cardiology and endoscopy portfolios

- Balance sheet optionality: $446M cash, $697M available credit capacity, 1.7x net debt/EBITDA

The company completed a small divestiture (DualCap® anti-microbial cap product line) in February 2026.

Key Risks Mentioned

Management highlighted several risks in the filing:

- Trade policy uncertainty: Guidance excludes potential tariff impacts from U.S. or other countries

- Integration risk: Multiple recent acquisitions require successful integration

- FX headwinds: ~0.8% headwind assumed in FY 2026 guidance

- Regulatory compliance: Ongoing Medical Device Regulation (MDR) expenses in Europe ($5.8M in FY 2025)

- Leadership transition: Executive succession planning activities underway

Bottom Line

Merit Medical delivered a clean beat-and-raise quarter, extending its EPS beat streak to nine consecutive quarters. The 130 bps of operating margin expansion in FY 2025 demonstrates execution on the Continued Growth Initiatives Program, while strong free cash flow generation ($216M, +16% YoY) provides flexibility for continued M&A.

FY 2026 guidance implies another year of above-market organic growth (5-7% constant currency) with continued margin expansion to the $4.01-4.15 Non-GAAP EPS range. At ~12x forward earnings, the valuation appears to underappreciate the company's consistent execution and margin improvement trajectory.

Data sources: Merit Medical Q4 2025 8-K filing, Q4 2025 earnings presentation, S&P Global consensus estimates, market data.