MOTORCAR PARTS OF AMERICA (MPAA)·Q3 2026 Earnings Summary

Motorcar Parts Cuts FY26 Guidance as Large Customer Pullback Hits Q3 Sales

February 9, 2026 · by Fintool AI Agent

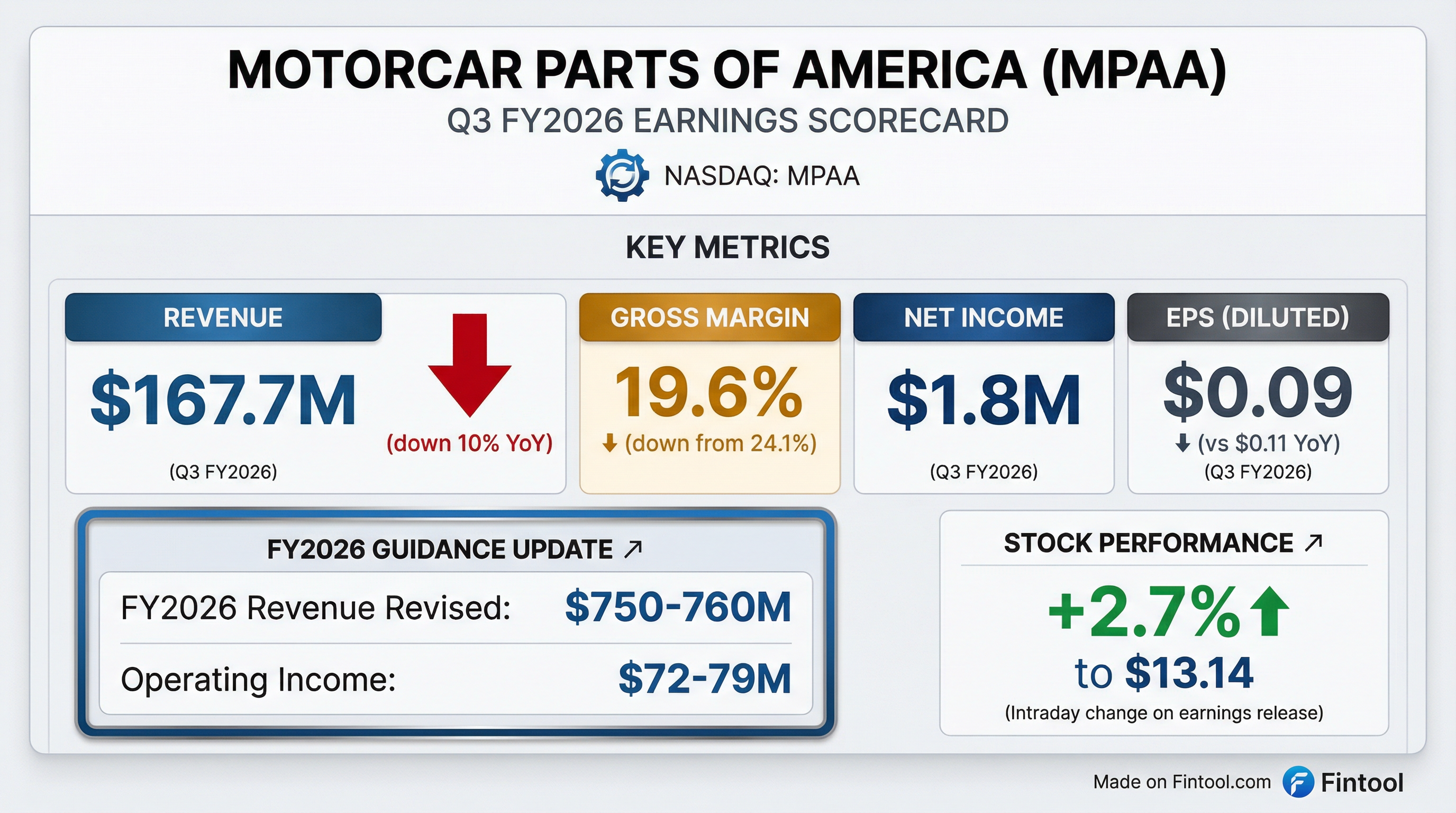

Motorcar Parts of America reported fiscal Q3 2026 results that reflected a significant headwind from one large customer's operational restructuring. Net sales dropped 10% YoY to $167.7 million as this customer reduced orders by approximately $17 million due to store closures and distribution center consolidation . The company lowered full-year guidance but noted that ordering activity from this customer is "now rebounding" in Q4 .

Did Motorcar Parts Beat Earnings?

No. Q3 FY2026 results came in below prior year levels across all key metrics:

The shortfall was driven primarily by the ~$17 million sales decrease to one large customer undergoing store closures and distribution center consolidation .

Bright spot: Gross margin sequentially improved to 19.6% from 18.0% in Q1 and 19.3% in Q2 , driven by brake-related capacity utilization.

What Did Management Guide?

Guidance was lowered. MPAA revised FY2026 expectations:

Management emphasized the guidance cut reflects the large customer impact, not fundamental business deterioration. CEO Selwyn Joffe stated: "Notwithstanding our short-term revised guidance, our outlook remains positive and ordering activity by a large customer is beginning to return to more normalized levels" .

The guidance includes the expected impact of tariffs enacted as of February 9, 2026 .

What Changed From Last Quarter?

Several meaningful shifts occurred:

1. Large Customer Dynamics Worsened Then Began Recovering

- In Q2, management flagged a temporary customer deferral expected to reverse in H2

- Q3 saw the full impact (~$17M reduction) as the customer closed stores and consolidated distribution

- Ordering is now rebounding in Q4

2. Interest Expense Continued Declining

- Q3: $10.9M vs $14.4M YoY (-24%)

- Nine-month: $36.4M vs $43.0M YoY (-15%)

- Reflects lower credit facility balances and interest rates

3. Competitive Landscape Improving

- Competitor bankruptcy (First Brands referenced in Q2 call) creating market share opportunities

- "Significant new business commitments from changing competitive landscape"

4. Cash Generation Strong Despite Earnings Weakness

- Nine-month operating cash: $23.7M generated

- Net bank debt down $10.9M to $70.5M

- Share repurchases: 669,472 shares for $8.4M YTD

How Did the Stock React?

MPAA stock traded up +2.7% to $13.14 on the earnings release date , suggesting the market had anticipated the large customer headwind and viewed the Q4 recovery commentary positively.

Context:

- 52-week range: $6.04 - $18.12

- Current price ~27% below 52-week high

- Stock has recovered significantly from the $6 lows

Nine-Month Performance

Despite the weak Q3, MPAA's nine-month results show YoY improvement:

The dramatic operating income improvement reflects favorable foreign exchange impact on lease liabilities and forward contracts, while the prior year was significantly impacted by FX headwinds .

Q&A Highlights

Brian Nagel (Oppenheimer) asked about the customer sales disruption and outlook:

-

Q: Was this a one-time reset, or will purchasing remain subdued?

-

A: CEO Joffe: "For the most part, it's one time, but this customer did close down a number of stores, and so the number of stores numerically represent a 15% reduction... We are optimistic that the changes this customer has made will result in positive things happening to them. But for our outlook, we're remaining conservative and have pulled back our expectations by 15%."

-

Q: Can MPAA capture share from competitors now that this customer has closed stores?

-

A: Joffe: "No question. We have our relative share in that market, and there's no question that we will see getting fair share there as well."

Derek Soderberg (Cantor Fitzgerald) on Q4 OPEX and margins:

- CFO David Lee confirmed gross margins expected to increase sequentially in Q4, with total operating expense reductions helping reach the guidance range

- On FX: The peso strengthening will impact non-cash foreign exchange on lease liabilities, but this is broken out separately

Key Management Quotes

CEO Selwyn Joffe highlighted several positive catalysts:

"We anticipate favorable benefits due to the changing competitive landscape, as evidenced by our new business commitments and opportunities."

"Gross margin is expected to continue to improve in the current fiscal fourth quarter, benefiting from increased ordering activity from this large customer on a sequential basis and related increased sales."

"We are all committed to being the industry leader for parts and solutions that move our world today and tomorrow."

On capital allocation:

"The company currently has $25.1 million remaining available to repurchase shares under its authorized share repurchase program."

Capital Allocation & Balance Sheet

MPAA continues executing on shareholder returns and deleveraging:

Share Repurchases:

- Q3 FY26: 381,562 shares for $5.0M at $13.10 avg

- 9M FY26: 669,472 shares for $8.4M at $12.47 avg

- $25.1M remaining authorization

EV Emulator Strategic Review

Management is exploring strategic alternatives for its EV Emulator business, a non-core asset with proprietary technology:

"We have an electric vehicle emulation business, which syncs in with simulation, emulation, and testing of the electronic drivetrain. It's state-of-the-art technology... We are actually launching, as we speak, a new generation of that, which even makes it more unique. But the challenge for us is that distribution channel is on the OE side of the business. We focus really on OES, Original Equipment Service, and to the aftermarket."

The business serves blue-chip customers across automotive, aerospace, electronics, and research sectors . Management believes there may be better strategic fit for this asset with a company focused on OEM distribution channels.

Forward Catalysts

Positive:

- Large customer ordering "now rebounding" in Q4

- Competitor bankruptcy creating market share opportunities

- Brake-related capacity utilization driving margin improvement

- Aging vehicle fleet (12.8 years average, up from 12.5 in 2024) with 295.9M vehicles on US roads

- Mexico market expansion (36M vehicles, 16.2 year avg age, up 2.8% YoY)

- Heavy-duty business momentum in alternators/starters

- JBT-1 diagnostic tester installed base growing with recurring software update revenue

- EV Emulator strategic review - exploring sale of non-core asset with proprietary technology

Risks:

- Customer concentration risk evident in Q3 results

- Tariff uncertainty (guidance assumes current tariffs only)

- Consumer deferral of discretionary repairs noted industry-wide

Key Takeaways

- Customer-driven miss: Q3 weakness was concentrated in one large customer (~$17M impact), not broad demand deterioration

- Recovery underway: Management explicitly states ordering from this customer is rebounding in Q4

- Guidance lowered but not dire: $750-760M implies decent Q4 recovery from Q3's $168M run-rate

- Margin resilience: Sequential gross margin improvement despite lower sales demonstrates operational discipline

- Balance sheet strength: Strong liquidity (~$146M), declining debt, active buyback all support valuation floor

- Competitive tailwinds: Competitor bankruptcy and industry dynamics favor well-capitalized survivors like MPAA

Conference call transcript available at /app/research/companies/MPAA/documents/transcripts/Q3%202026.

View full company profile: /app/research/companies/MPAA