Marqeta (MQ)·Q4 2025 Earnings Summary

Marqeta Beats Q4 Expectations But Stock Drops 7% on Slower 2026 Outlook

February 24, 2026 · by Fintool AI Agent

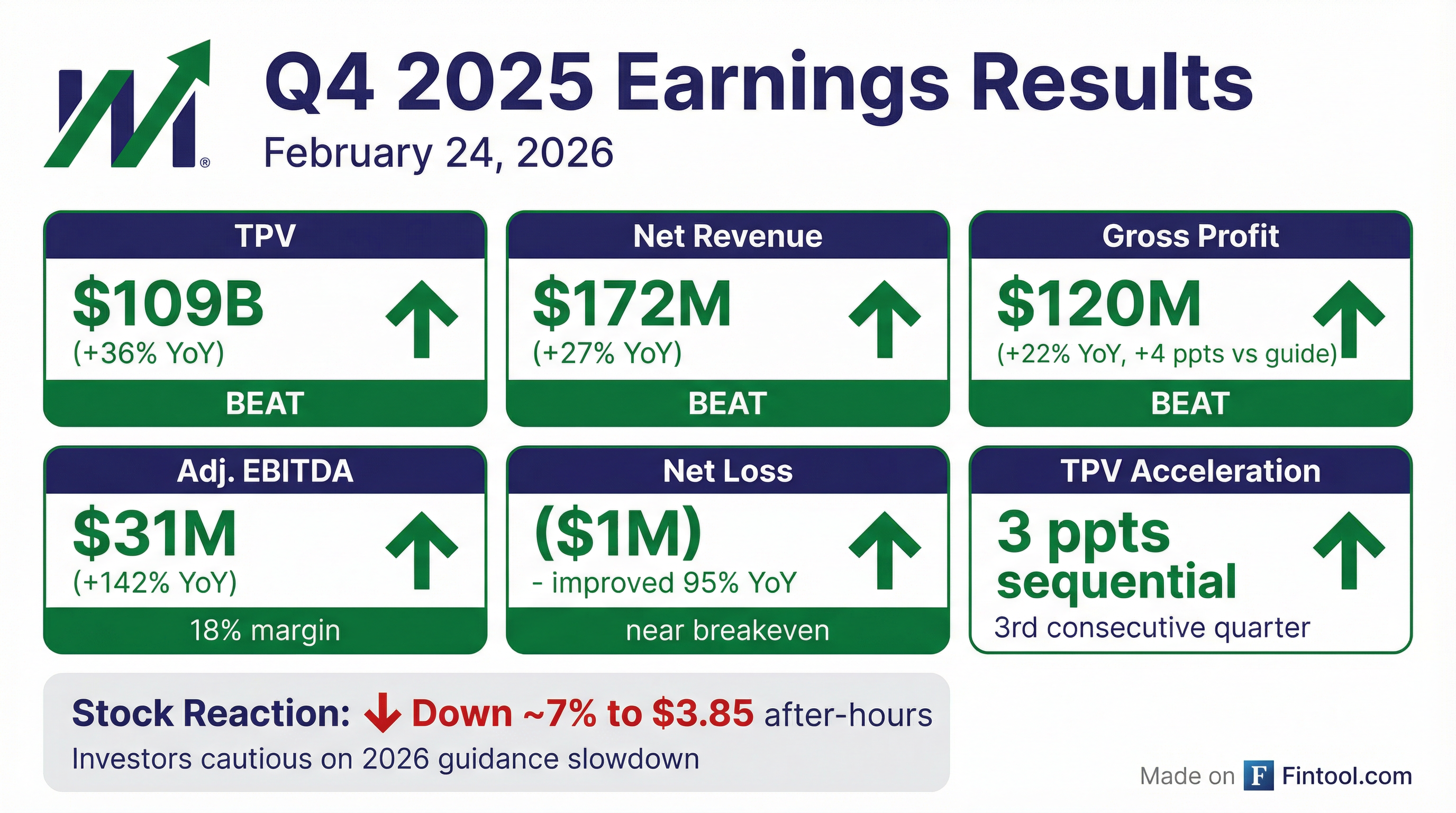

Marqeta (MQ) delivered a strong Q4 2025, with TPV accelerating to +36% YoY and gross profit beating guidance by 4 percentage points. Adjusted EBITDA hit an all-time high of $31M with 18% margin. However, shares dropped ~7% after-hours to $3.85 as investors focused on the 2026 gross profit guidance of just 10-12% growth — a sharp deceleration from 24% in 2025 — partly due to ~7 points of timing headwinds unique to next year.

Did Marqeta Beat Earnings?

Yes — Marqeta beat across all key metrics in Q4 2025:

This marks the third consecutive quarter of accelerating TPV growth — Q4 was 3 ppts higher sequentially. It's also Marqeta's first quarter exceeding $100B in TPV.

What Drove the Beat?

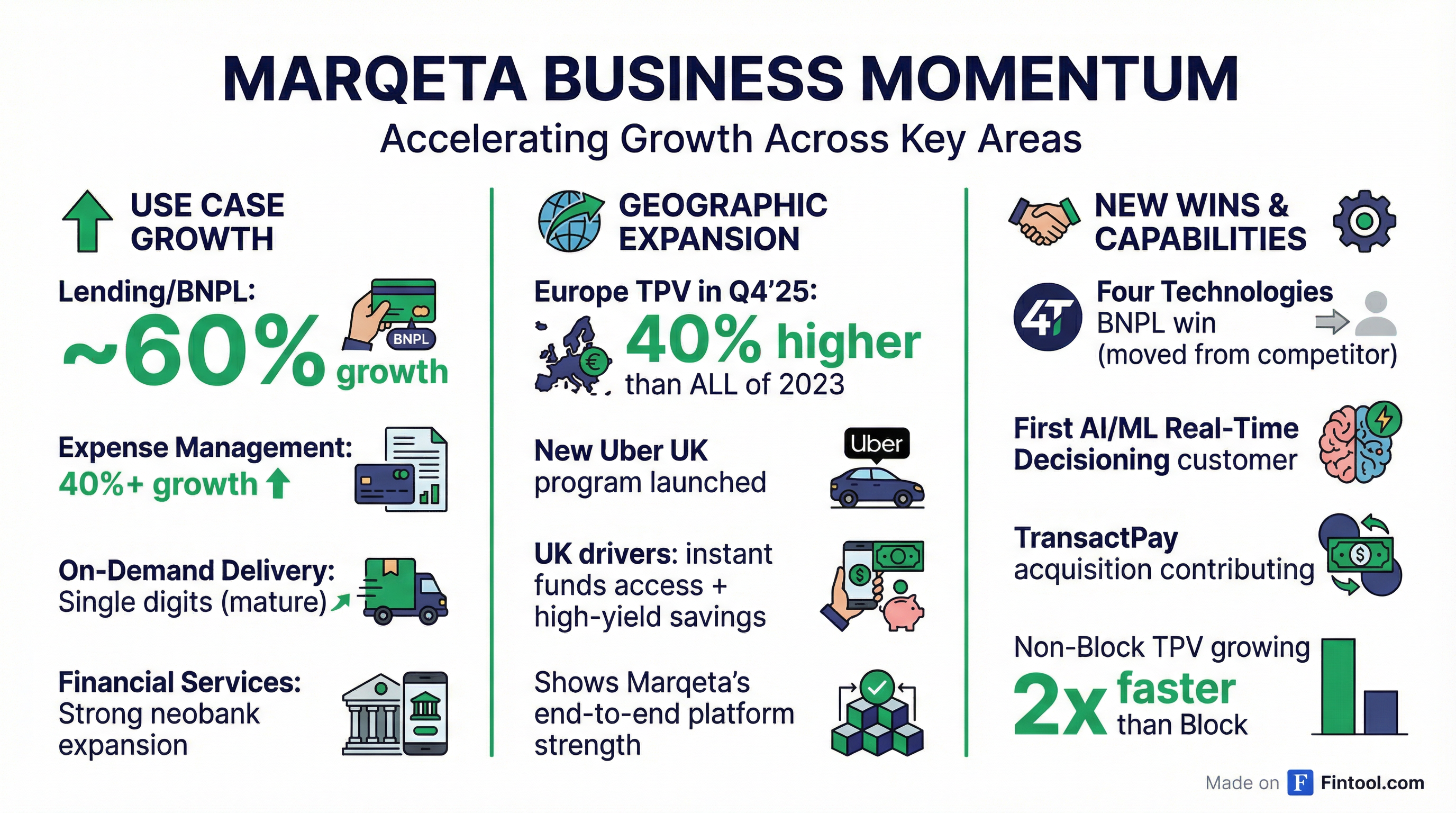

Broad-based strength across use cases:

- Lending/BNPL: Grew just shy of 60% — powered by Klarna's Europe migration and Pay Anywhere adoption

- Expense Management: Exceeded 40% growth — corporate card platforms gaining share

- Non-Block TPV: Growing 2x faster than Block, driving diversification

- Europe: Q4 2025 TPV was ~40% higher than all of 2023 — showing geographic scaling

Notable customer wins and launches:

- Uber UK: New program providing UK drivers instant fund access + high-yield savings — showcasing Marqeta's end-to-end platform across program management, banking, processing, fraud monitoring, and Real-Time Decisioning

- Four Technologies: BNPL provider moved from competitor to Marqeta for its "tech forward offering and proven track record"

- AI/ML Decisioning: First customer onboarded to enhanced Real-Time Decisioning using AI for risk evaluation during transaction authorization

What Did Management Guide for 2026?

The key concern: Full-year 2026 gross profit growth of 10-12% compares to 24% in 2025 — a meaningful deceleration. However, management noted this includes ~7 ppts of timing headwinds unique to 2026.

The positive: Marqeta expects to achieve GAAP Net Income profitability of ~$10M for the first full year — a significant milestone for the company.

How Did the Stock React?

Despite the Q4 beat, investors sold the stock after hours. The reaction suggests the market was expecting stronger 2026 guidance and is concerned about the deceleration in gross profit growth, even accounting for timing headwinds.

MQ is now trading near its 52-week low of $3.48, down significantly from the $7.04 high reached earlier in the trailing twelve months.

Full Year 2025 Performance

*FY 2024 Net Income included $145M one-time reversal from Executive Chairman award forfeiture

The full year story is remarkable: Adjusted EBITDA grew 3.5x year-over-year from $29M to $110M, demonstrating significant operating leverage as the platform scales.

Quarterly Trend Analysis

Note the consistent acceleration in TPV growth throughout 2025 — from 27% in Q1 to 36% in Q4, adding 3 ppts sequentially in Q4. This momentum gives credibility to management's optimism despite the guidance concerns.

What Changed From Last Quarter?

Positives:

- TPV growth accelerated again (+3 ppts sequentially to 36%)

- First quarter exceeding $100B in TPV

- Adjusted EBITDA hit new all-time high at $31M

- Europe continues rapid scaling

- First AI/ML enhanced decisioning customer onboarded

- New customer wins (Four Technologies, Uber UK expansion)

Concerns:

- 2026 gross profit guidance of 10-12% is below 2025's 24%

- ~7 ppts of timing headwinds flagged for 2026

- Stock dropped 7% after-hours despite the beat

- Gross margin compression from 72% (Q4'24) to 70% (Q4'25)

CEO Commentary

CEO Mike Milotich highlighted the company's positioning:

"In 2025, the business delivered outstanding growth and increased EBITDA by deepening existing customer relationships and developing new ones through geographic, use case, and solution expansion. As we start 2026, our leadership and expertise in powering innovative offerings with our differentiated end-to-end platform positions us well to expand our reach and deepen engagement as the market evolves toward modern, multinational processors operating at scale."

Balance Sheet & Cash Position

Cash declined primarily due to $391M in share repurchases during 2025, reducing shares outstanding by over 12% from year-end 2024 levels. The company remains well-capitalized with no debt.

Key Risks to Monitor

-

Block Concentration: While declining (45% in Q1 2025, down 4 ppts YoY), Block remains the largest customer

-

Guidance Deceleration: 10-12% gross profit growth in 2026 vs 24% in 2025 — even excluding timing headwinds, underlying growth is slowing

-

Macro Sensitivity: Consumer spending patterns on the platform could shift if macro conditions deteriorate

-

Competition: Other modern processors and card issuers competing for fintech and embedded finance customers

Forward Catalysts

- Q1 2026 Results (expected May 2026): First quarter under new guidance framework

- GAAP Profitability: Achieving the guided ~$10M net income would be a milestone

- Block Contract Renewal: Timing and terms of upcoming renewal will be closely watched

- Europe Expansion: Continued scaling could drive upside to guidance

- New Product Adoption: AI/ML decisioning and credit platform traction

Data sourced from Marqeta Q4 2025 earnings supplement, 8-K filing, and S&P Global.