MANITOWOC CO (MTW)·Q4 2025 Earnings Summary

Manitowoc Stock Drops 12% as Crane Maker's Q4 Revenue Beats but EPS Misses

February 10, 2026 · by Fintool AI Agent

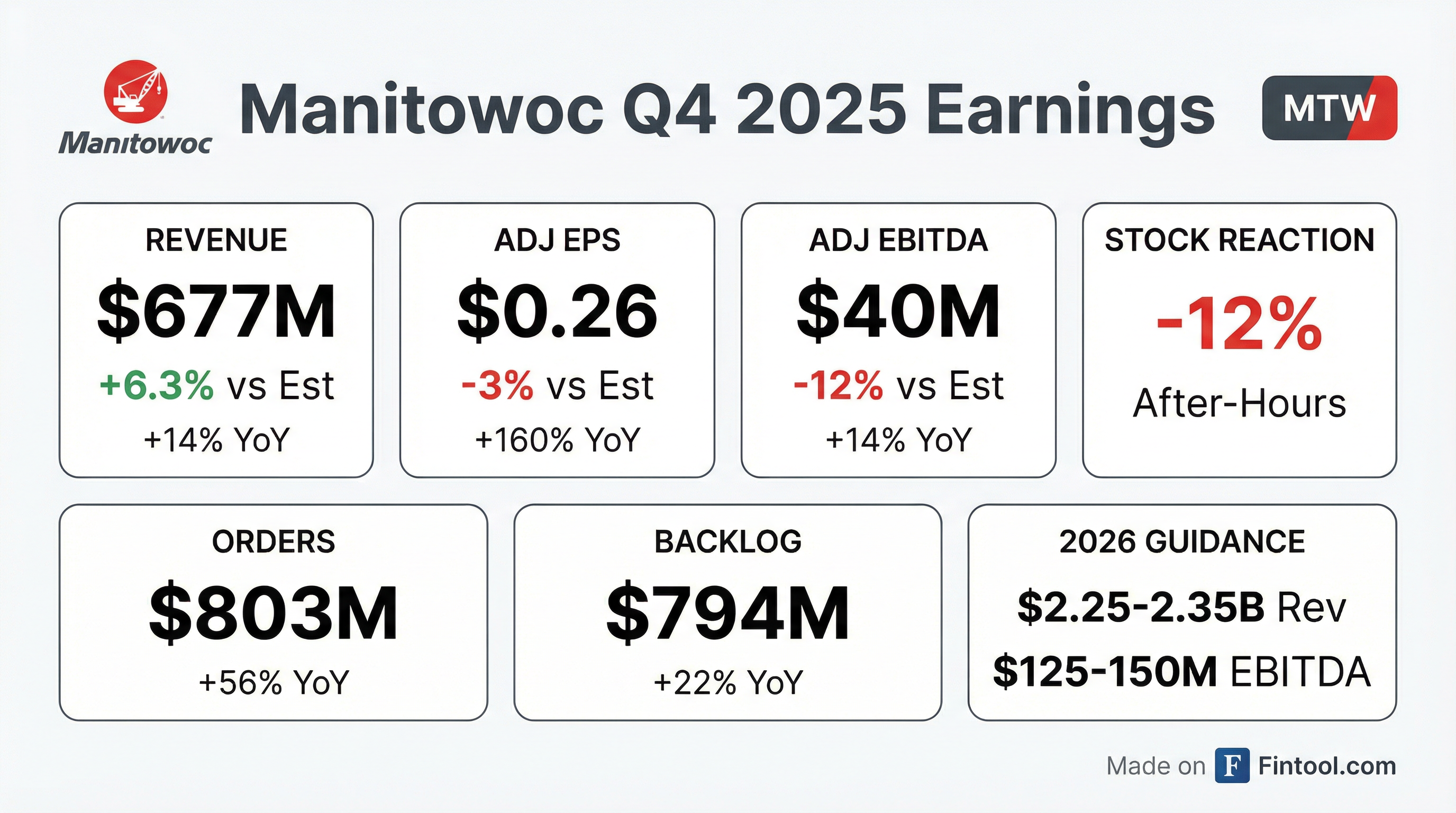

Manitowoc reported Q4 2025 results that beat revenue expectations but missed on profitability metrics, sending shares down 12% in after-hours trading. The crane manufacturer delivered revenue of $677M (+14% YoY), beating consensus by 6.3%, but Adjusted EPS of $0.26 missed the $0.27 estimate. More concerning was the Adjusted EBITDA miss of $40M vs $45M expected (-12%), despite the strong top-line performance.

Did Manitowoc Beat Earnings?

Mixed results: Revenue beat handily while earnings fell short.

The revenue beat was driven by strong order activity and non-new machine sales. Q4 orders surged 56% YoY to $803M (vs $516M in Q4 2024), while backlog grew 22% to $794M.

However, the EBITDA miss suggests margin pressure persisted. Full-year Adjusted EBITDA margin contracted to 5.4% from 5.9% in 2024, despite the revenue growth.

What Did Management Guide for 2026?

Manitowoc provided full-year 2026 guidance that signals improvement ahead:

The wide EPS guidance range ($0.45-0.90) reflects uncertainty around end-market conditions and tariff impacts. Management highlighted that 2025 free cash flow was impacted by a $45M EPA settlement payment — excluding this, underlying FCF would have been ~$30M.

The EBITDA bridge to 2026 midpoint ($138M) relies on pricing actions, market recovery in EU tower cranes, and restructuring savings to offset tariff headwinds and inflation.

How Did the Stock React?

MTW shares dropped 12% in after-hours trading to $13.00 from the $14.86 close.

The stock had been on a strong run heading into earnings, up nearly 50% from $10.08 in mid-May 2025. Investors appear disappointed by:

- EBITDA miss — Profitability underperformed despite revenue beat

- Tariff uncertainty — Management noted "customer sentiment muted due to tariff-related uncertainty" in North America

- Wide guidance range — EPS guidance of $0.45-0.90 signals low visibility

What Changed From Last Quarter?

Positives:

- Orders accelerated — Q4 orders of $803M were up 56% YoY and well above Q3's pace, with management citing "large stocking orders in Q4 to secure build slots"

- European sentiment improving — "Positive sentiment driven by public stimulus funding" and "continued improvement in Tower and Mobile Cranes"

- Record aftermarket — Non-new machine sales hit a record $690M for full year, up 10% YoY, with 500+ service techs (up 12%)

Concerns:

- North America uncertainty — Tariff concerns tempering customer sentiment despite stocking activity

- Middle East slowing — "Slowing pace of infrastructure projects" despite optimistic sentiment

- Margins under pressure — Full-year EBITDA margin of 5.4% down from 5.9% in 2024

Full-Year 2025 Performance

Full-year results showed modest top-line growth but earnings compression:

The FCF decline was primarily driven by the $45M EPA environmental settlement. Excluding this one-time payment, operating cash flow trends remained healthy.

Key Strategic Initiatives

Management highlighted several growth drivers for their long-term 15% ROIC target:

- Service expansion — 500+ field service technicians, with new locations in Nashville, Phoenix, Baton Rouge (US), Sydney (Australia), and France. Territory coverage expanded in North Carolina, South Carolina, Georgia, and several French provinces.

- New product development — 11 new crane models launched in 2025, with two major launches at ConExpo March 2026

- HIAB distribution agreement — MGX will represent HIAB knuckle boom products across 13 U.S. states, with synergies to existing boom truck portfolio

- Fleet replacement cycle — "Fundamentally, fleets continue to age, and at some point, a major refresh will be required"

Non-New Machine Sales Trajectory: From $376M in 2020 → $690M in 2025 (record), with a target of $1 billion. Gross margins on non-new machine sales are ~35% vs ~5% EBITDA margins on the consolidated business.

The company's Adjusted ROIC was 5.3% in 2025, down from 6.0% in 2024, still well below the 15% long-term target. Net leverage ended at 3.15x with $298M total liquidity; management targets leverage below 3.0x during 2026.

Regional Outlook

Regional Color from Management:

- Europe — Tower crane orders up 64% YoY, mobile crane orders up 39% YoY in Q4. CEO noted "sentiment is a lot better than it was a year ago" after meeting with key dealers in January.

- Middle East — Saudi Arabia projects moving but "cash continues to tighten." Dubai residential projects remain "extremely hot." Stargate data center in Abu Dhabi moving slower than expected — Phase 1 tower crane work complete but Phase 2 has not started. New Dubai airport has let first three construction packages with tower crane work expected in 2026.

- Asia Pacific — South Korea optimism bolstered by Samsung and SK hynix semiconductor project announcements. Australia awaiting green light on major power transmission project.

- North America — "Rental rates have remained flat, which is my biggest concern," said CEO Ravenscroft. "The cost of new cranes is going up, and rental rates need to follow for crane operators to justify the purchase of new cranes or fleet renewals."

Q&A Highlights

January 2026 orders: CEO reported ~$225M in January orders, calling it a "good month." The European winter campaign for tower cranes was strong — "first time in a few years we've had a good winter campaign." Demand for large rough terrain cranes and crawlers "has been really good."

Q1 2026 outlook: CFO Regan noted Q1 will be "a little bit low relative to the rest of the year" due to: (1) tariff headwind timing, (2) negative FX impact, and (3) restructuring savings benefiting later quarters. Q2 and Q4 are expected to be the strongest quarters.

Tariff mitigation: Tariffs had a gross unfavorable impact of $39M for 2025, but management mitigated ~85% through targeted pricing and sourcing actions. Net tariff impact was $0.13 per share headwind YoY.

LEAN/Manitowoc Way update: Shop floor improvements are mature — team is now applying SMED (quick changeover) and robot programming optimizations. CEO is "super excited to see what we can do with AI" for office productivity but noted "nothing to brag about just yet." Focus now on improving customer experience at MGX aftermarket locations.

Product Launches & ConExpo Preview

Manitowoc launched 11 new cranes in 2025 and previewed two major launches for ConExpo in March 2026:

CEO: "A big thank you to our engineering teams. It's been a big lift to extend our product portfolio into these higher ranges."

Safety Milestone

Manitowoc achieved a recordable injury rate (RIR) of 0.94 — the first time in company history the RIR dropped below 1.0. First-aid incidents also declined 10% YoY. For context: in 2015, Manitowoc had 91 recordable injuries; in 2025, just 42. Long-term goal remains zero injuries.

Bottom Line

Manitowoc delivered a strong revenue beat driven by surging orders, but profitability disappointed with EBITDA and EPS misses. The 12% after-hours drop reflects investor concern over margin compression and tariff-related uncertainty in North America.

The 2026 guide is constructive — implying EBITDA recovery and significant FCF improvement — but the wide EPS range ($0.45-0.90) signals management is hedging on end-market visibility. Watch for clarification on tariff impacts and margin trajectory in coming quarters.

CEO Ravenscroft closed with optimism: "Europe and Asia-Pacific are moving in the right direction, and the Middle East business remains positive. The American market appears poised for a rebound with interest rates trending down and the tariff environment stabilizing."

Key catalysts to watch:

- ConExpo product launches (March 2026)

- Tariff policy clarity

- Dubai airport tower crane awards

- Australia power transmission project decision

- Fleet replacement cycle timing

Related Links: