Option Care Health (OPCH)·Q4 2025 Earnings Summary

Option Care Health Beats on Revenue and EPS, Stock Falls 6% on Cash Flow Miss

February 24, 2026 · by Fintool AI Agent

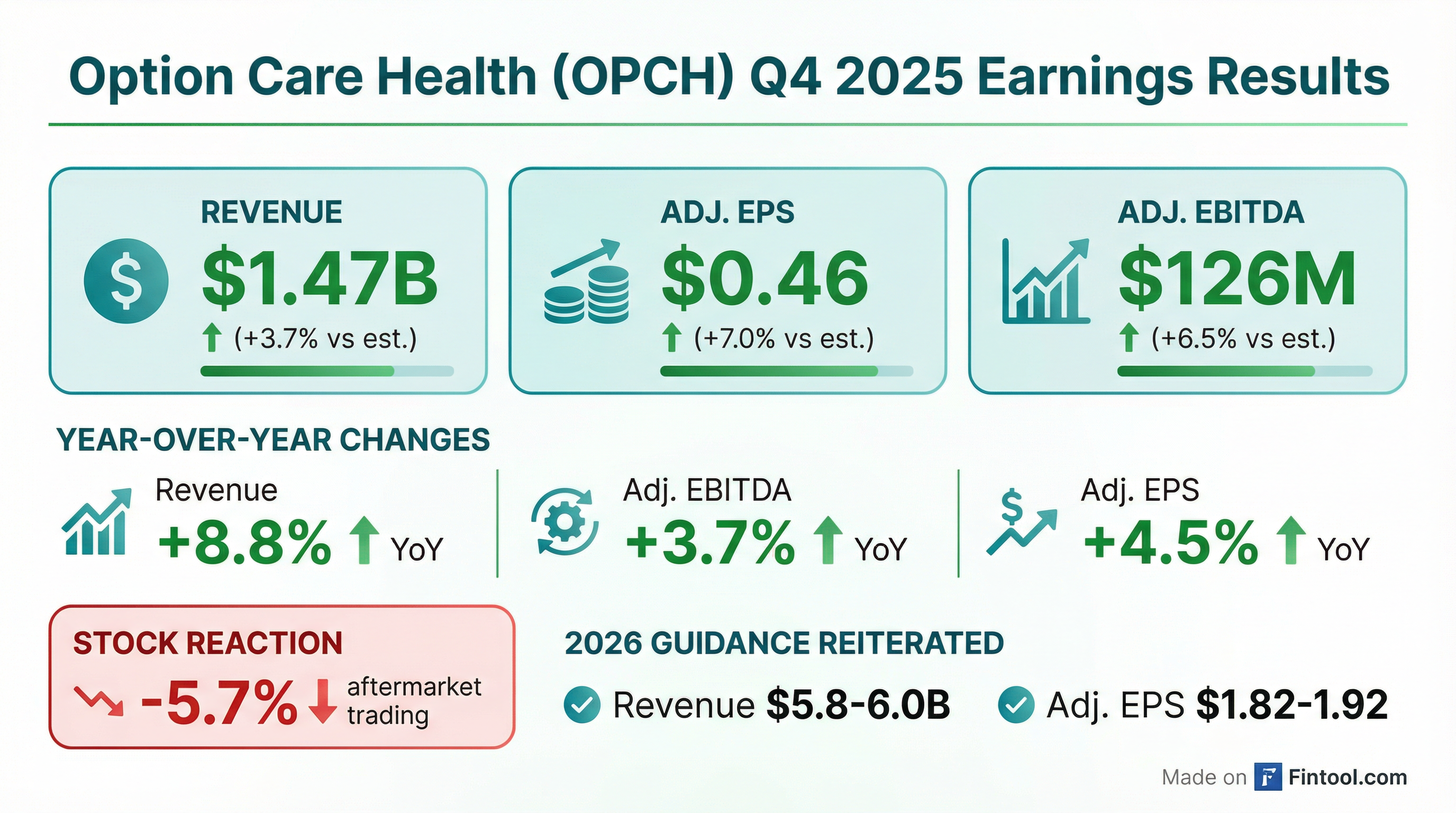

Option Care Health delivered a solid Q4 2025 with beats across revenue (+3.7%), Adjusted EPS (+7.0%), and Adjusted EBITDA (+6.5%), yet shares fell approximately 6% in aftermarket trading. The culprit: operating cash flow of $258M significantly missed the company's own guidance of "at least $320M," raising concerns about working capital management heading into 2026. Management reiterated full-year 2026 guidance unchanged from January, offering no upward revision despite the quarterly beats.

Did Option Care Health Beat Earnings?

Yes—OPCH beat on all major P&L metrics. The nation's largest independent home infusion provider delivered Q4 results that exceeded Street expectations:

Consensus estimates from S&P Global

Year-over-year comparisons show continued top-line momentum but margin pressure:

The 8.8% revenue growth outpacing 3.7% Adjusted EBITDA growth illustrates the margin compression theme that has persisted throughout 2025—higher volumes at lower incremental profitability.

Segment breakdown from the earnings call shows balanced growth across the portfolio :

Stelara biosimilar adoption created a 160 basis point revenue headwind for FY 2025, impacting the chronic portfolio .

How Did the Stock React?

Down ~6% in aftermarket, partially recovered during regular trading. OPCH closed at $36.09 on February 24 before the earnings release, dropped to ~$34.04 in aftermarket trading (-5.7%), then partially recovered during regular hours to trade around $34.94 (-3.2% from prior close). The stock touched an intraday low of $32.08.

The disconnect between solid quarterly results and negative stock reaction points to two key concerns:

-

Operating cash flow miss: Full-year 2025 operating cash flow came in at $258.4M , well below the "at least $320M" guidance provided in October . This represents a significant shortfall that management attributed to strategic inventory purchases.

-

No guidance raise: Despite beating Q4 estimates, management held 2026 guidance unchanged from the January 12 preliminary announcement , suggesting confidence levels aren't elevated heading into the new year.

What Did Management Guide?

2026 guidance reiterated, unchanged from January. Option Care Health's forward outlook factors in known headwinds from Stelara biosimilar conversions:

Key assumptions embedded in guidance:

- Stelara headwind: Management expects a 400bps revenue growth headwind from Stelara IRA and biosimilar conversions, translating to $25-35M gross profit headwind spread evenly throughout 2026

- Stelara de-risked: After 2026, Stelara and biosimilars represent <1% of company revenue and gross profit

- Cash flow recovery: The $340M+ operating cash flow target implies 30%+ growth vs 2025

2026 Modeling Items from CFO :

What Changed From Last Quarter?

Full-year 2025 results came in largely as expected based on January preliminary figures, with minor positive variances:

Beat/miss history shows consistent execution. Over the past 8 quarters, OPCH has beat or met EPS estimates in every period, demonstrating reliable delivery against expectations. The current quarter marks the 8th consecutive beat on Adjusted EPS.

What Did Management Say?

CEO John C. Rademacher struck a confident but measured tone:

"Our team continued to execute at a very high level to deliver extraordinary care and solid results in the fourth quarter and full year of 2025. During 2025, we served over 315,000 patients and they remain at the center of everything we do. We continued to make significant progress against our key priorities to build a sustainable growth enterprise while navigating a dynamic industry environment."

Looking ahead, Rademacher expressed optimism about growth opportunities:

"As we look ahead in 2026, I am excited about the opportunities to further our mission and capitalize on the positive long-term growth trends across our industry and the strength of our position to serve more patients."

Q&A Highlights: What Analysts Asked

On Stelara impact and guidance confidence — When asked about early Q1 trends and any changes to guidance, CFO Meenal stated: "Despite all that, when we look through all the activities and where we are today, we're not really seeing any substantial differences versus what we had assumed a month ago... If there was anything that would have caused us to rethink our guide, we would have incorporated here."

On double-digit EBITDA returning in 2027 — Brian Tanquilut (Jefferies) asked whether investors should expect a return to double-digit EBITDA growth once Stelara is behind them. The CFO noted: "If you take that out of the growth rate that the guidance implies, that puts us at a double-digit EBITDA. That's what we're striving for."

On payer affordability conversations — David MacDonald (Truist) pressed on payer dynamics. CEO Rademacher responded: "The pace of those conversations has increased, as the payers have been focusing around really their MLR and looking for opportunities to maintain quality, but do it at a lower cost."

On 340B exposure — Charles Rhyee (TD Cowen) asked about 340B program risk. Management clarified: "Any of the 340B savings is just a transfer of those savings back to the hospital... I wouldn't say it's a meaningful part of our overall economics."

On competitive landscape — Erin Wright (Morgan Stanley) asked about runway from competitor exits. Rademacher noted: "We certainly don't see as big of a significant shift that we've seen over the last couple of years with two major competitors kind of resetting their network design... The market for infused products is over $100 billion. We're $6 billion of that. We think there's still continue runway for us to be that partner of choice."

Capital Allocation Update

Aggressive share repurchases continued. Option Care Health repurchased $95M of stock in Q4 2025 and $307M for the full year 2025 . In January 2026, the Board expanded the buyback authorization from $500M to $1.0B , signaling confidence in the stock's value.

Balance sheet highlights as of December 31, 2025:

Cash declined $180M year-over-year as the company deployed capital toward share repurchases ($307M) and the Intramed Plus acquisition ($117M) .

Intramed Plus integration exceeding expectations — The South Carolina-based acquisition is performing above initial targets. Management noted infusion clinic visits at Intramed Plus sites grew 25% year-over-year in Q4 .

Operational Highlights: KPIs and AI Progress

Management highlighted several key operational achievements during the call :

AI and Automation — CEO Rademacher emphasized AI's impact: "The measurable response is when you're able to do 40% of your claim processing without actually having human intervention, you can see the benefits that are driven on that. Again, that allows our team to focus on the higher complexity claims."

Beyond revenue cycle, the company is deploying AI for call center capabilities, workforce optimization, and inventory management .

Payer Program Expansion — Option Care added 5 new site-of-care programs with regional health plans and 2 with nontraditional payers (conveners and direct-to-employer programs) in 2025 .

Pharma Partnerships — The company operates over 20 enhanced pharma manufacturer programs and expects to launch 2 additional rare/limited distribution drug platforms in 2026 .

Key Risks and Concerns

-

Cash flow volatility: The $60M+ cash flow miss in 2025 raises questions about working capital management and whether inventory build is truly "strategic" or masks operational challenges

-

Margin compression: Revenue growing faster than EBITDA (13% vs 6% in FY25) suggests pricing pressure in the competitive home infusion market

-

Stelara transition: While management frames the biosimilar conversion as manageable, execution risk remains through 2026

-

Share count dilution offset: Despite $307M in buybacks, diluted shares only declined 5.5% YoY (163.4M vs 172.8M) , as stock-based compensation partially offsets repurchases

Forward Catalysts

- Q1 2026 earnings (late April): First read on Stelara biosimilar conversion progress

- M&A activity: Management has capacity and stated appetite for "adjacent & accretive M&A"

- New therapy additions: Company added 600+ therapies in 2025 including limited distribution drugs

- Cash flow recovery: Proving $340M+ operating cash flow guidance will be critical for sentiment

The Bottom Line

Option Care Health delivered solid Q4 2025 results that beat consensus on revenue, EPS, and EBITDA, extending its streak of reliable execution. However, the operating cash flow miss and unchanged 2026 guidance suggest the easy money in this name has been made. The stock's 6% aftermarket decline reflects investor concern that growth is decelerating (FY26 revenue guide of +4% vs FY25's +13%) while margin expansion remains elusive. With the Stelara headwind to navigate and cash flow credibility to rebuild, OPCH enters 2026 with more to prove than its beat-and-reiterate quarter might suggest.

Data sourced from company filings and S&P Global. Stock prices as of market close February 24, 2026.