Otter Tail (OTTR)·Q4 2025 Earnings Summary

Otter Tail Q4 2025: EPS Misses as Plastics Normalization Accelerates, 2026 Guidance Down 17%

February 17, 2026 · by Fintool AI Agent

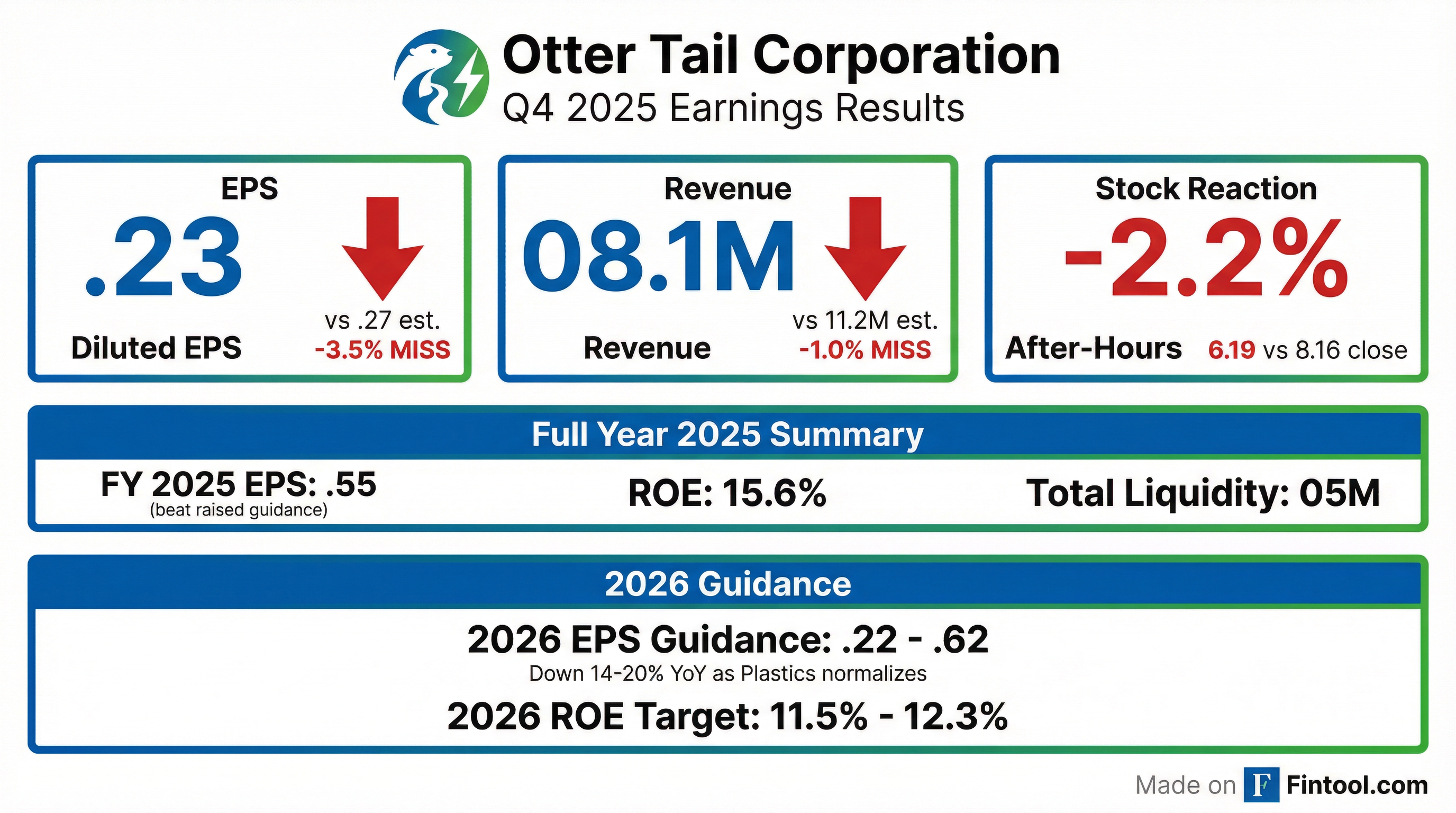

Otter Tail Corporation (OTTR) reported Q4 2025 results that missed consensus estimates on both EPS and revenue, marking the company's second consecutive quarterly miss. More significantly, 2026 guidance of $5.22-$5.62 implies a 14-20% earnings decline as the Plastics segment continues its multi-year normalization from peak profitability in 2022.

The stock traded down 2.2% in after-hours to $86.19 following the release.

Did Otter Tail Beat Earnings?

No. Otter Tail missed on both EPS and revenue in Q4 2025:

This marks the second consecutive miss after Q3 2025's slight EPS shortfall, breaking a streak of six consecutive beats from Q1 2024 through Q2 2025.

Full-year 2025 results exceeded guidance, however, with diluted EPS of $6.55 vs the original guidance range of $5.68-$6.08 (later raised to midpoint $6.47).

What Did Management Guide for 2026?

Otter Tail initiated 2026 EPS guidance of $5.22-$5.62, implying a 14-20% decline from 2025's $6.55. The midpoint of $5.42 represents a 17% YoY decline.

2026 EPS guidance breakdown by segment:

The guidance implies a significant earnings mix shift: 2026 is expected to be approximately 49% Electric / 51% Non-Electric, moving toward the long-term target of 70% Electric / 30% Non-Electric as Plastics normalizes.

CEO Chuck MacFarlane emphasized the company's long-term trajectory:

"We are initiating our 2026 diluted earnings per share guidance range of $5.22 to $5.62 and affirming our long-term financial targets. The fundamentals of our business and diversified portfolio remain strong and we are confident in our ability to deliver on our growth plan for the benefit of our customers and shareholders. We continue to target a long-term earnings per share growth rate of 7 to 9 percent, resulting in a total shareholder return of 10 to 12 percent."

What Changed From Last Quarter?

Key changes from Q3 2025:

-

Manufacturing momentum improved. Q4 Manufacturing segment net income was $2.6M vs a loss of $0.6M in Q4 2024—an $3.2M swing—as sales volumes increased 11% with customers replenishing inventories.

-

Plastics pricing pressure accelerated. Q4 2025 PVC pipe prices declined 20% YoY, worse than the 15% FY decline, suggesting normalization is accelerating.

-

Rate base growth visibility improved. The company reaffirmed 10% rate base CAGR through 2030, with 2026-2030 capex plan of $2.05B.

-

Cash position strengthened. Total liquidity reached $705.5M at year-end, up from $606M in Q4 2024.

How Did the Stock React?

OTTR traded down 2.2% in after-hours to $86.19 from the $88.16 close on February 13 (the last trading day before the long weekend). Markets were closed February 14 and 17 for Presidents' Day.

Recent stock performance:

- YTD 2026: +3.5%

- 52-week range: $71.79 - $90.11

- Current valuation: ~13x forward P/E (based on $5.42 midpoint guidance)

The modest sell-off suggests the earnings normalization was largely anticipated. OTTR has traded in a relatively tight range as investors balance the Plastics headwind against Electric segment growth and strong capital return.

Segment Performance Deep Dive

Electric Segment — The Growth Engine

The Electric segment delivered consistent growth despite the company-wide earnings decline:

Key drivers for 2026 Electric growth (+14% segment earnings):

- 14% increase in average rate base

- Interim revenues from Minnesota general rate case (first since 2020)

- Final rates expected from South Dakota general rate case

- Higher operating expenses from labor costs and Big Stone Plant outage

Rate Case Requests:

Large Load Opportunity Pipeline:

Note: Phase 1 and 2 large load additions are not included in load growth or capex forecasts. Opportunities driven by data centers, crypto mining, clean fuel, and agriculture processing.

Plastics Segment — Normalization Continues

The Plastics segment remains highly profitable but is returning to historical margins:

Plastics Earnings Normalization Path:

Management expects Plastics earnings to normalize to $45-50M annually by 2028, implying further significant declines from the $170M in 2025 and guided $105-115M in 2026.

Manufacturing Segment — Signs of Recovery

After struggling through 2025, Manufacturing showed Q4 improvement:

CEO MacFarlane noted that "customer order activity picked up" toward year-end, "enabling us to end the year with momentum."

Capital Allocation and Investment Plan

Otter Tail outlined an aggressive capital investment plan funded entirely without equity issuances:

5-Year Capital Expenditure Plan (2026-2030):

Major Generation & Storage Projects

Major Transmission Projects

Rate base growth trajectory:

The plan produces a 10% CAGR on average rate base over the five-year period.

Balance Sheet and Liquidity

Otter Tail's balance sheet remains a key differentiator:

The company plans to finance its entire 5-year growth plan without any equity issuances, using cash flow from the manufacturing platform to fund utility rate base growth.

Key Risks and Concerns

1. Plastics normalization could accelerate. Q4 pricing was down 20% YoY, worse than the 15% full-year decline. If pricing pressure intensifies, 2026 guidance could prove optimistic.

2. Manufacturing recovery is uncertain. While Q4 showed improvement, "conditions in certain end markets remain challenged" per guidance assumptions.

3. Regulatory execution risk. 2026 guidance assumes favorable outcomes from Minnesota and South Dakota rate cases—the company's first rate filings since 2018 and 2020, respectively.

4. Large load pipeline remains early stage. Despite 970 MW of letters of intent for potential large loads (data centers, etc.), none have converted to signed electric service agreements.

Forward Catalysts

The Bottom Line

Otter Tail's Q4 miss and lower 2026 guidance were largely expected as the Plastics segment normalizes from extraordinary profitability. The key question for investors is whether the Electric segment's 10% rate base CAGR can offset the multi-year Plastics headwind.

Bull case: Electric growth accelerates through large load opportunities (not in base plan), Plastics stabilizes faster than expected, strong balance sheet enables opportunistic investments.

Bear case: Plastics pricing deteriorates further, Manufacturing recovery stalls, rate case outcomes disappoint, large loads fail to materialize.

Long-Term Shareholder Return Targets:

The company has paid dividends for 88 consecutive years without interruption or reduction, with the 2026 indicated dividend of $2.31 representing a 10% increase from 2025 (the second consecutive double-digit increase).

At ~13x forward P/E with a 2.6% dividend yield (recently increased 10%), OTTR appears fairly valued for a utility in earnings transition. The stock likely remains range-bound until visibility improves on 2027+ earnings trajectory.

Earnings call: February 17, 2026 at 10:00 AM CT — View transcript

Last updated: February 17, 2026 (Updated with earnings call transcript — no Q&A questions asked)