PITNEY BOWES INC /DE/ (PBI)·Q4 2025 Earnings Summary

Pitney Bowes Surges 14% After Hours as Adjusted EPS Beats by 43%, Massive Buybacks Continue

February 17, 2026 · by Fintool AI Agent

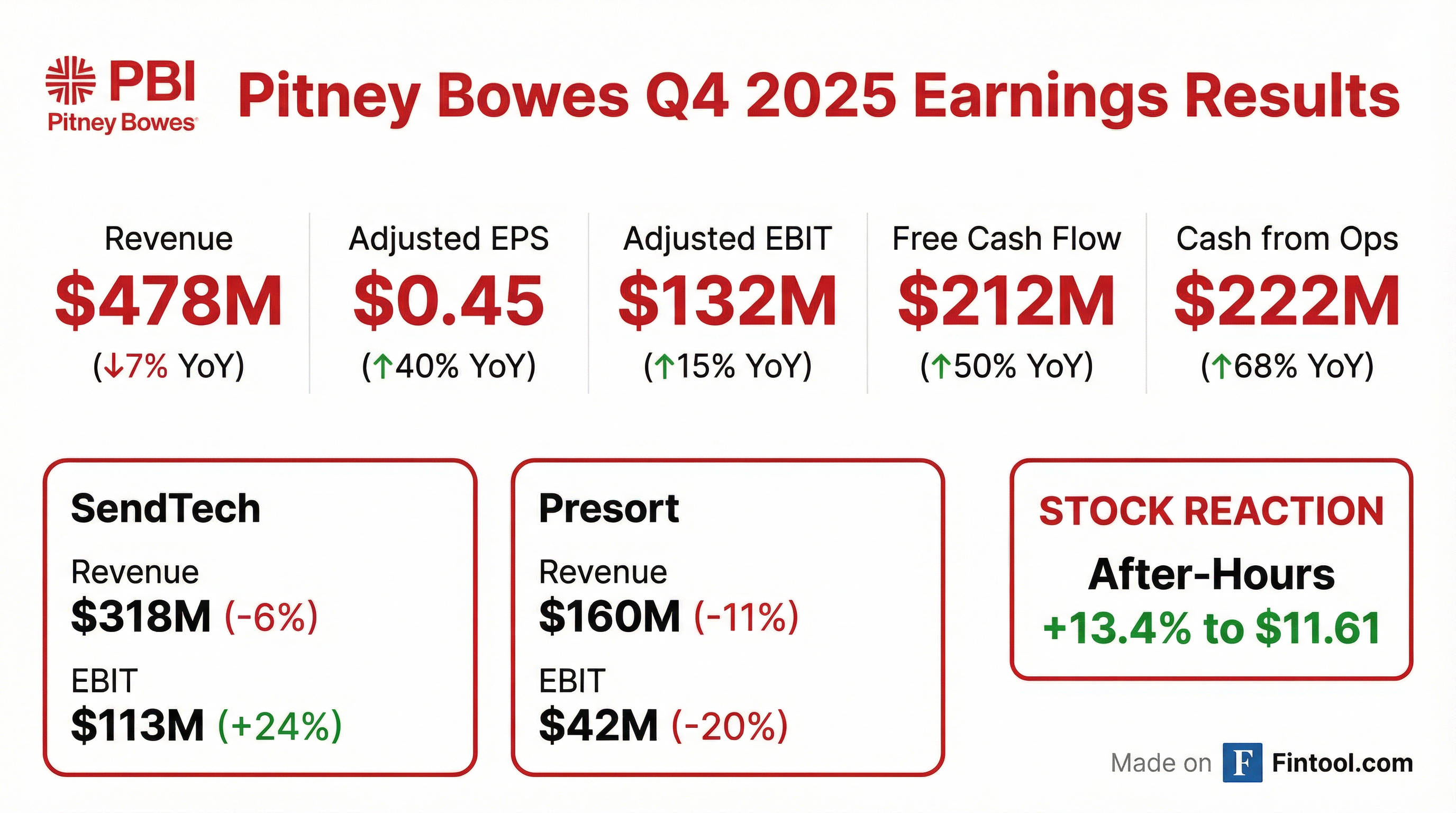

Pitney Bowes delivered a blowout Q4 with adjusted EPS of $0.45 crushing the $0.315 consensus by 43%, while revenue of $478M beat estimates by 2.3% despite ongoing top-line headwinds. The stock surged 14% after hours to $11.69 as investors cheered massive capital returns—the company bought back roughly 20% of its shares in 2025 and announced another $250M authorization.

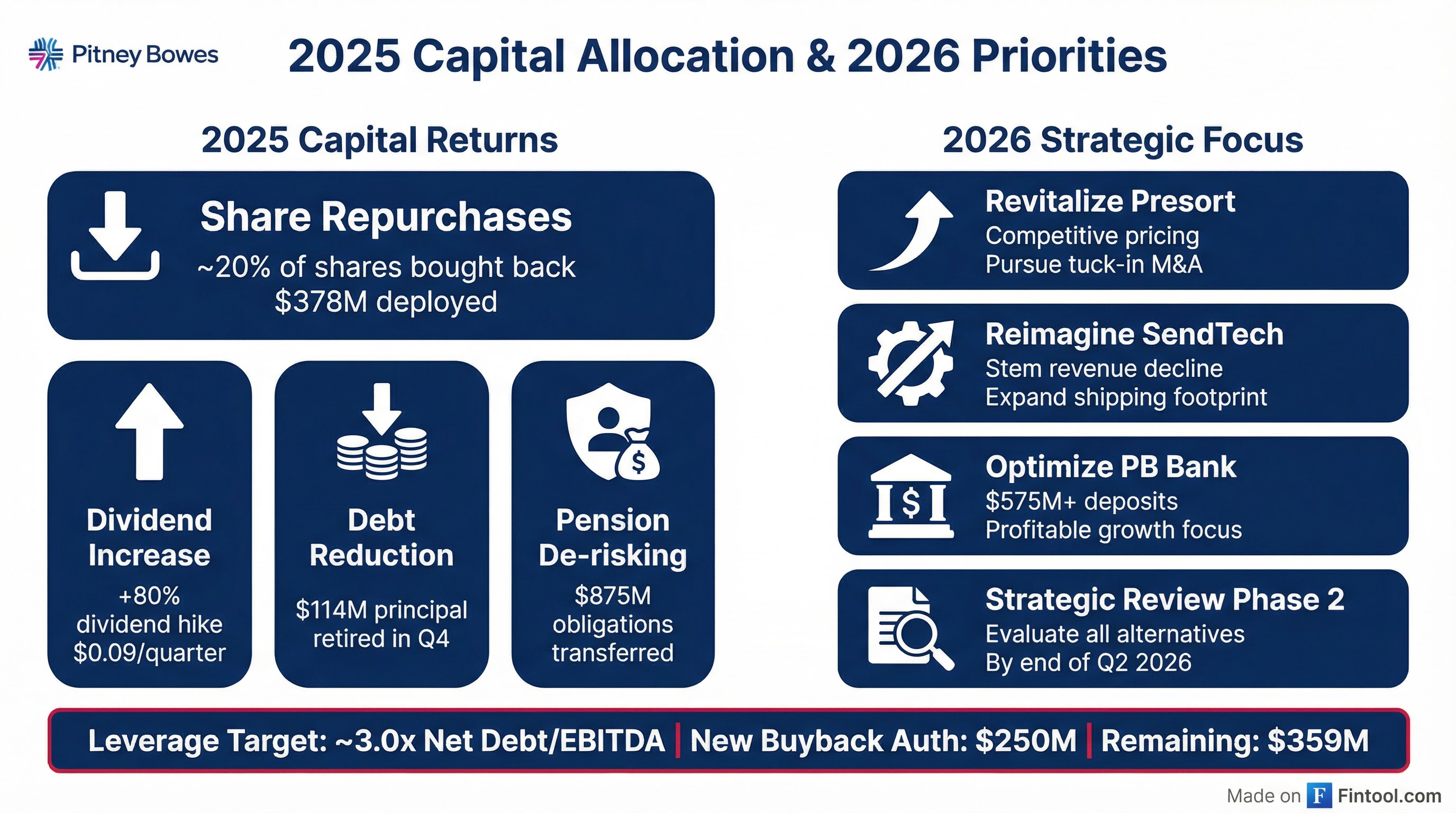

CEO Kurt Wolf's aggressive capital allocation strategy is paying dividends: free cash flow jumped 50% YoY to $212M in Q4, funding $127M in share repurchases and $114M in debt reduction during the quarter alone. The company also transferred $875M in pension obligations to insurance carriers, further de-risking the balance sheet.

Did Pitney Bowes Beat Earnings?

Yes—decisively on profitability, modestly on revenue.

The EPS outperformance came from disciplined cost management, improved operational execution, and significant share count reduction from buybacks. Operating expenses declined $28M YoY in SendTech alone, while gross margin expanded 180 basis points.

Full Year 2025 also showed dramatic improvement:

- Revenue: $1.893B (down 7% YoY)

- Adjusted EPS: $1.35 (up 64% vs $0.82 in 2024)

- Free Cash Flow: $358M (up 24% YoY)

What Did Management Guide?

Management issued wider-than-usual guidance ranges for FY2026, citing "market uncertainty and geopolitical challenges" and efforts to improve forecasting accuracy.

The guidance disconnect is notable: revenue is guided below consensus while EPS is guided above. This reflects management's confidence in continued margin expansion and buyback accretion, even as top-line headwinds persist. At the midpoint, EPS guidance implies 11% growth despite 4% revenue decline.

Key guidance assumptions from the CEO letter:

- SendTech expected to exit "the low point of its product cycle" with less steep revenue declines

- Presort may sacrifice short-term profitability for volume growth through competitive pricing

- Strategic Review Phase 2 to commence by end of Q2 2026

How Are the Segments Performing?

The two business segments showed divergent trends—SendTech improving operationally while Presort struggles with volume losses.

SendTech Solutions (66% of Revenue)

SendTech's revenue decline was driven by prior year product migration (now concluded) and shrinking mailing install base. However, operating leverage improved dramatically—EBIT margin expanded significantly on cost reduction initiatives. Shipping revenues declined only 5% YoY, suggesting stabilization in that growth vertical.

New leadership (Todd Everett, who previously led Newgistics to a value-maximizing sale) is developing strategies to stem revenue declines and resume growth by end of H1 2026.

Presort Services (34% of Revenue)

Presort's decline reflects previously communicated client losses and broader market decline. Management acknowledged that early-year pricing decisions caused "profitable business to walk out the door." New business wins and no material customer losses since June 2025 suggest the bleeding has stopped.

CEO Wolf has given Presort President Debbie Pfeiffer the "green light to act with urgency" with competitive pricing, even if it means sacrificing short-term profitability for long-term cash flow.

What Changed From Last Quarter?

Several material developments distinguish this quarter:

-

Massive Capital Returns - 12.6M shares repurchased for $127M in Q4, plus another $250M authorization (totaling $359M capacity). Roughly 20% of shares bought back in 2025.

-

Balance Sheet De-risking - $875M pension obligations transferred to insurance carriers via buy-in contracts. S&P issued a positive credit watch.

-

Debt Reduction - $114M principal retired in Q4 through tender offers, open market repurchases of Term Loan B and 2027 Notes, and scheduled amortization.

-

Leadership Upgrades - Paul Evans as CFO, Todd Everett as SendTech President, Steve Fischer to run PB Bank. Executive layers eliminated.

-

Headquarters Move - Relocated corporate HQ to existing Shelton, CT facility and eliminated Global Financial Services complex structure.

How Did the Stock React?

PBI closed the regular session at $10.24 (flat), but surged 14.2% to $11.69 in after-hours trading following the earnings release.

The stock has traded in a range between $7.40 and $13.11 over the past year. The after-hours move suggests investors are rewarding the combination of earnings beat, buyback-driven EPS growth, and progress on the turnaround under new leadership.

At current prices, PBI trades at roughly 8x FY2026 EPS guidance midpoint ($1.50)—a modest multiple for a company generating $350M+ in annual free cash flow with aggressive capital returns.

Key Management Quotes

From CEO Kurt Wolf's shareholder letter:

"We took decisive action which supported our success last year... New leadership's focus on efficiency and smoother processes delivered additional annualized cost savings in excess of $50 million – without the use of consultants."

On Presort's pricing mistake:

"While it is true we offer a premium service, with an extraordinary Net Promoter Score and faster delivery of mail than our competitors, customers largely buy based on price."

On capital allocation:

"I remain dedicated to a nimble capital allocation policy that balances debt reduction, share repurchases, well-timed dividend increases, and long-term and opportunistic investment."

What's Next? Forward Catalysts

-

Q4 2025 Earnings Call - February 18, 2026 at 8:00 AM ET. Watch for color on Presort volume trends and SendTech shipping strategy.

-

Strategic Review Phase 2 - Expected by end of Q2 2026, will "review all potential alternatives to our standalone value creation trajectory."

-

SendTech Strategy Articulation - New plan expected by end of H1 2026 focused on mailing meter retention, enterprise shipping expansion, and portfolio streamlining.

-

Presort Volume Recovery - Watch for new business wins and pricing-driven volume stabilization in coming quarters.

-

Continued Buybacks - With $359M remaining authorization and strong FCF, expect continued aggressive repurchases.

Risks and Concerns

- Secular Mail Decline - Physical mail volumes continue declining, pressuring both segments

- Presort Customer Losses - Pricing decisions led to client attrition; recovery uncertain

- Forecasting Credibility - Management acknowledged forecasting misses as "a disappointment"

- Leverage - While improving, ~3x Net Debt/EBITDA remains elevated

- Revenue Guidance Below Consensus - Top-line headwinds expected to continue in 2026

Earnings call scheduled for February 18, 2026 at 8:00 AM ET. This analysis will be updated with Q&A highlights following the call.

Related: PBI Company Profile | Q3 2025 Earnings | Latest Transcript