IMPINJ (PI)·Q4 2025 Earnings Summary

Impinj Q4 Beat Overshadowed by Steep Q1 Guidance Miss—Stock Plunges 25%

February 5, 2026 · by Fintool AI Agent

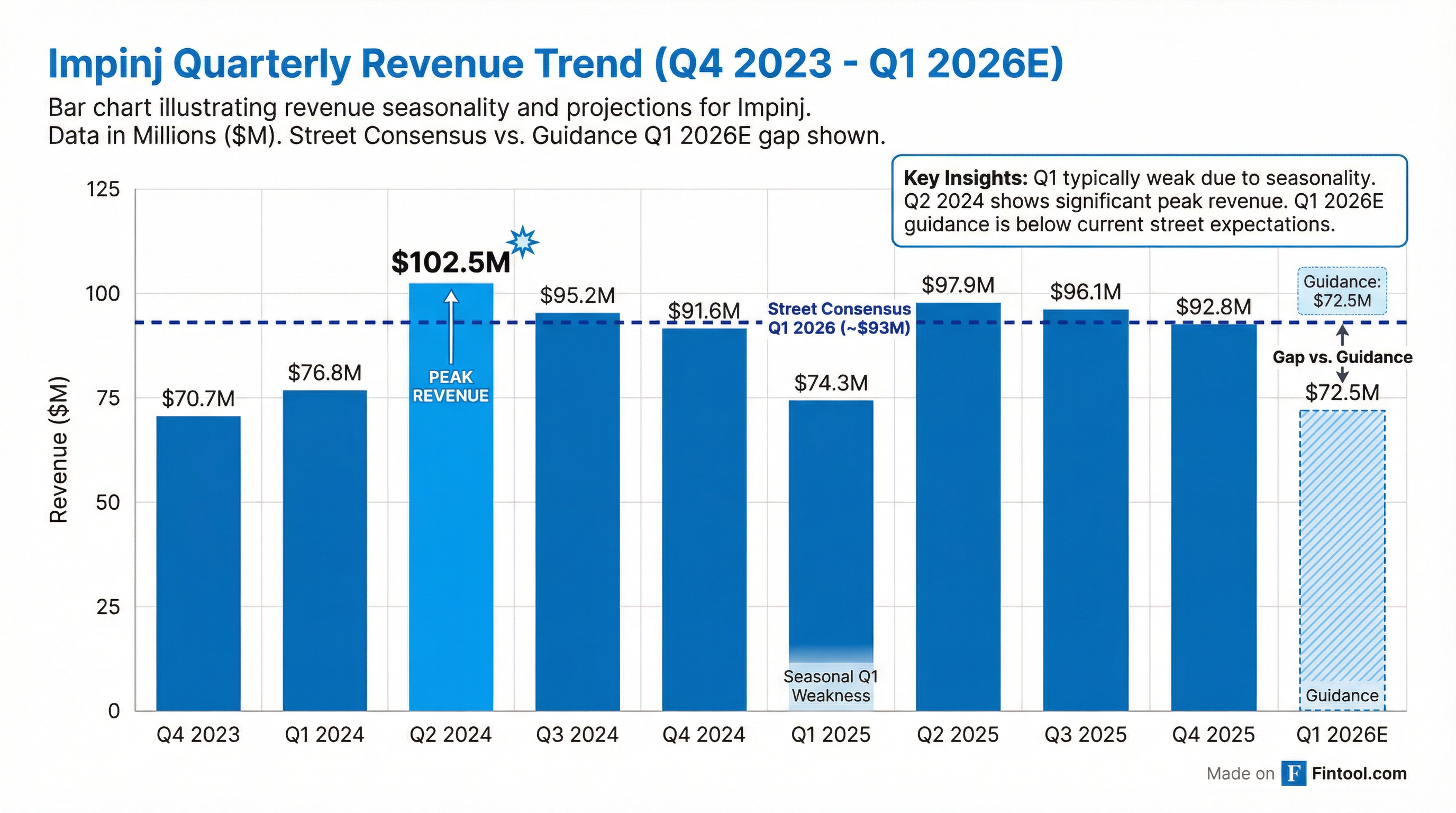

Impinj (NASDAQ: PI) reported Q4 2025 results that met expectations, but the stock cratered 25% in after-hours trading after the RAIN RFID pioneer guided Q1 2026 revenue 22% below consensus. The guidance miss signals a sharp deceleration heading into 2026, overshadowing what management characterized as a "transition year" in which the company grew endpoint IC volumes and launched new Gen2X technology.

Did Impinj Beat Earnings?

Impinj delivered Q4 2025 results essentially in line with analyst expectations:

*Values retrieved from S&P Global

This marked a solid beat versus the company's own prior guidance of $90-93M revenue and $15.4-16.9M adjusted EBITDA, which was preannounced in January.

For the full year 2025, Impinj delivered:

- Revenue: $361.1M (down 1.4% YoY from $366.1M in 2024)

- Adjusted EBITDA: $69.6M (record high)

- Non-GAAP Net Income: $64.2M ($2.11/share)

- Free Cash Flow (TTM): $45.9M

What Did Management Guide?

This is where things fell apart. Q1 2026 guidance came in dramatically below expectations:

*Values retrieved from S&P Global

The $72.5M revenue midpoint represents a 22% sequential decline from Q4 and puts Q1 2026 below even Q1 2025's $74.3M.

CFO Cary Baker broke down the Q1 guidance drivers:

- Logistics inventory burn: Inlay partners burning down "a few weeks of inventory" — each week ≈ $5M impact

- Pricing: Annual endpoint IC price reductions contributing ~$2M headwind

- Retail weakness: Apparel retailers reducing stock and under-buying demand

- Product transition: Custom IC ramp causing temporary dip as partners reduce prior M800 inventory

Positive signals management highlighted:

- January turn orders already double the same point in Q4

- Turn orders 50%+ higher than January 2025

- Endpoint IC business ~100% booked to midpoint of guide

- Elevated rescheduling behavior from 2025 has "significantly moderated"

How Did the Stock React?

The market reaction was swift and severe:

The 25% aftermarket drop reflects investor disappointment that the "transition year" narrative didn't translate into a 2026 inflection. Impinj entered the quarter trading at a premium multiple on expectations of RAIN RFID adoption acceleration.

What Changed From Last Quarter?

Q3 2025 vs Q4 2025 Key Changes:

Guidance trajectory worsened significantly:

- Q4 2025 guidance (given in Q3): $90-93M → Delivered $92.8M ✓

- Q1 2026 guidance: $71-74M → 22% below Street ✗

The Q1 seasonal trough is typical (Q1 2025 was also the weakest quarter at $74.3M), but this year's guidance suggests even deeper weakness.

Key Management Commentary

CEO Chris Diorio framed 2025 as a year of foundation-building while acknowledging Q1 headwinds:

"2025 was a tough year for our industry. Tariffs and tariff-related supply chain whipsaws, inventory reductions at every layer of our retail markets, a downward trend in apparel imports, and protracted general merchandise adoption all weighed heavily on the RAIN market."

"Despite the starting points looking the same, we see 2026 very differently from 2025. 2025, we took a competitive lead and held our own in what was otherwise a pretty tough year. In 2026, we're gonna press that lead in what we believe is shaping up to be a growth year."

Key operational highlights cited:

- 150B+ endpoint ICs sold (cumulative as of Dec 31, 2025)

- 6M+ connectivity devices sold

- 294 patents protecting the platform

- Gen2X launch — new RAIN solutions technology

- Chris Hundley hired as EVP for Enterprise Solutions to accelerate solutions pivot

Custom ASIC: A Strategic Pivot

One of the most significant developments revealed on the call was a custom endpoint IC developed specifically for Impinj's second-largest North American supply chain and logistics customer:

Key details:

- Already in production — not just in design, currently shipping

- Customer plans to fully switch to this IC in 2026

- Includes custom features like label authentication solving key business needs

- Eliminates unneeded features (think of it as an ASIC approach)

- Opens opportunities for outward-facing customer accounts

- Impinj retains the IP with ability to license to additional customers

- Priced "to market" currently — future solution sales may change pricing model

CEO Diorio emphasized this represents a shift toward enterprise solutions rather than component sales:

"We're focused on enabling solutions for enterprise end users. Those solutions are not just a chip. It's a chip and an antenna, and the airlink supporting it, and the Reader IC supporting that... We firmly believe that by delivering whole solutions and optimizing for the end user, we can outperform mix-and-match efforts using competitor products."

The custom IC approach provides better inventory visibility — Impinj can now match shipments directly to the customer's monthly consumption reports.

New Customer Wins & Retailer Momentum

Management highlighted several new retail accounts coming online:

- Abercrombie & Fitch

- Aritzia

- Old Navy

- Academy Sports

These wins come as existing apparel retailers work through inventory burn-down, with management expecting apparel demand to normalize as early as Q2.

Business Segment Performance

Impinj's revenue breaks down into two main categories:

Endpoint ICs (reader ICs, tag chips) represent ~81% of revenue and are the higher-margin growth driver. The sequential decline suggests inventory digestion or demand softness in retail/supply chain end markets.

Systems (readers, gateways, test equipment, software) held relatively steady, providing some stability.

Market Opportunity & Competitive Position

Impinj continues to highlight the massive TAM opportunity in RAIN RFID:

- 52.8B RAIN tag chips shipped globally in 2024

- This represents only ~0.5% of connectable items

- Trillions of consumable items remain unconnected annually

Target markets include:

- Food & drink packaging (3 trillion items/year)

- Auto parts (600 billion)

- Parcels & postal (400 billion)

- General merchandise (325 billion)

- Apparel (80 billion)

Major deployments span retail giants (Walmart, Target, Nike, H&M, Inditex), airlines (Delta, United, American), and logistics providers (UPS, China Post).

Balance Sheet & Liquidity

The balance sheet remains solid with near-parity between cash and debt. The asset-light manufacturing model and NOL shield provide financial flexibility during this soft patch.

Historical Beat/Miss Record

*Values retrieved from S&P Global

Impinj has a strong track record of beating estimates (7 of last 8 quarters on revenue), which makes the Q1 2026 guidance miss even more jarring.

Key Risks & Concerns

- Demand visibility: The steep Q1 guidance cut suggests either customer inventory destocking or delayed adoption timelines

- Cyclicality: RAIN RFID remains tied to retail capex cycles, which may be softening in 2026

- Competition: Growing competitive pressure in the endpoint IC market

- Concentration: Dependency on large retail deployments for volume growth

- Valuation reset: Stock traded at premium multiple; guidance miss forces multiple compression

EM Microelectronic Partnership

Impinj announced EM Microelectronic as a Gen2X licensee, a strategic move to provide second-source confidence to enterprise customers:

- Working on a dual frequency IC (first chip likely not available in 2026)

- Revenue impact immaterial for 2026

- Strategic value: Enables customers to feel confident about adequate supply

- Related to custom IC strategy — providing supply security for enterprise solutions

A license payment is expected in Q2 (similar to historical pattern with NXP).

Q&A Highlights

On competitive threats from BLE:

"The volume differences between [RAIN and BLE] are gigantic. I mean, our industry delivered 52.8 billion ICs in 2024... I view them as mostly complementary."

On Gen2X driving market share:

"I believe that Gen2X will be the significant driver of our market share gains... Think of Gen2X as a toolbox that we can bring to bear for enterprise customers who have an unmet need and allow us to solve their problem."

On food vertical expectations: Management sees "inexorable growth" in food despite modest Q1 volumes, with bakery leading and proteins to follow. The opportunity is described as "staggeringly large."

On 2026 outlook vs. 2025:

"2025, we took a competitive lead and held our own in what was otherwise a pretty tough year. In 2026, we're gonna press that lead in what we believe is shaping up to be a growth year."

Forward Catalysts

- Q2 license payment: Expected from competitor (similar to historical NXP payments)

- Q1 2026 earnings (late April): Watch for any guidance stabilization

- Custom IC full ramp: Second-largest logistics customer switching entirely in 2026

- Gen2X adoption: New technology platform driving enterprise solutions wins

- New retail accounts: Abercrombie & Fitch, Aritzia, Old Navy, Academy Sports onboarding

- Food vertical expansion: Bakery stores expanding, proteins next

- RAIN Alliance data: Industry IC shipment trends (next report H1 2026)

The Bottom Line

Impinj delivered a clean Q4 that matched expectations, but the Q1 2026 outlook was a gut punch. Revenue guidance of $71-74M is 22% below consensus, driven by a confluence of logistics inventory burn-down, retail weakness, and product transitions.

However, the earnings call revealed a more nuanced picture than the headline guidance suggests:

- Bookings are strong: January turns double Q4, up 50%+ YoY, nearly 100% booked to midpoint

- Custom ASIC strategy: Major logistics customer fully switching in 2026, improving visibility

- New retail wins: Abercrombie & Fitch, Aritzia, Old Navy, Academy Sports coming online

- Gen2X momentum: Management confident it will drive market share gains

The 25% aftermarket selloff prices in significant disappointment, and management acknowledged the Q1 inventory correction "may spill over into Q2." But the strategic pivot toward enterprise solutions and custom ICs—rather than commodity chip sales—could differentiate Impinj if execution delivers. The market opportunity remains massive (only 0.5% penetrated), and management sees 2026 as "a growth year" once Q1 headwinds clear.

Related Research: