PACKAGING CORP OF AMERICA (PKG)·Q4 2025 Earnings Summary

PKG Misses on Revenue and EPS as Greif Integration Costs and Volume Weakness Weigh on Q4

January 28, 2026 · by Fintool AI Agent

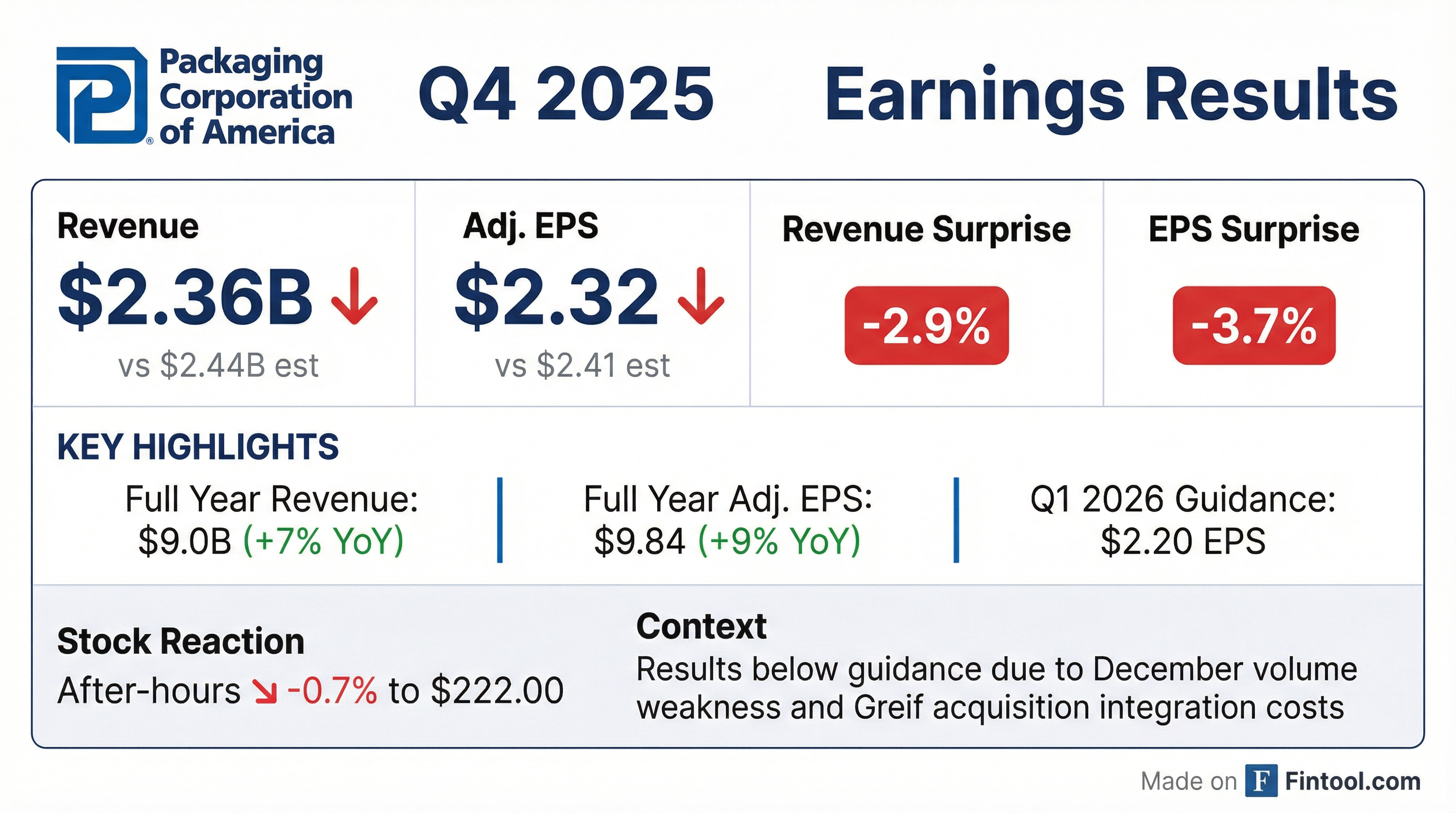

Packaging Corporation of America reported Q4 2025 results that missed on both top and bottom lines. Adjusted EPS of $2.32 came in 3.7% below consensus of $2.41, while revenue of $2.36B missed by 2.9%. The shortfall was driven by weaker December volume in the legacy corrugated business, extended outages at the acquired Greif Massillon mill, and $128M in restructuring charges related to the Wallula, WA mill reconfiguration.

Despite the Q4 miss, full-year 2025 results showed solid improvement: adjusted EPS grew 9% to $9.84 vs. $9.04 in 2024, and revenue increased 7% to $9.0B. The stock traded down ~0.7% in after-hours to $222.

The key takeaway from the call: Management struck a bullish tone on 2026 demand, noting January bookings are up 11% and billings up 8% per day year-over-year. CEO Mark Kowlzan said the company expects to "run the entire mill system full out" for all of 2026.

Did PKG Beat Earnings?

No — PKG missed on both revenue and EPS.

Management attributed the miss to "unfavorable December volume and mix in the legacy corrugated business and unfavorable December production and sales volume in the acquired Greif business."

EPS Bridge: Q4 2025 vs Q4 2024

The $0.15 year-over-year decline in adjusted EPS was driven by:

Headwinds:

- Lower legacy PCA packaging volume: -$0.23

- Higher operating costs: -$0.23

- Higher maintenance outage expense: -$0.14

- Higher depreciation: -$0.07

- Higher freight: -$0.06

- Greif acquisition loss (including interest): -$0.05

Tailwinds:

- Higher packaging prices and mix: +$0.50

- Lower fiber costs: +$0.10

- Lower fixed and other expenses: +$0.04

What Did Management Guide?

Q1 2026 EPS Guidance: $2.20 — below consensus of $2.28.

CEO Mark Kowlzan outlined expectations for Q1 2026:

Important Caveat: Management noted last weekend's winter storm impacted multiple regions, causing plants to be down "from the Texas region all the way across the Gulf region up through the Mid-Atlantic." While mills ran through the storm, the company couldn't ship tons out during the period.

$70/Ton Price Increase — Minimal Q1 Impact

PKG announced a $70/ton containerboard price increase effective March 1. However, management clarified Q1 guidance includes only "a small amount" of this benefit:

"These price increases... take place over about a 90-day period. And then we have some contracts that extend to mid-year." — Tom Hassfurther, President

Q4→Q1 Cost Bridge

CFO Kent Pflederer provided detail on the sequential cost headwind:

- Q4 to Q1 cost increase: $0.45-$0.50 per share

- Recovery in Q2: "A little under half" excluding Wallula

- Wallula benefit: Cost improvements begin in March, ramping in Q2

What Changed From Last Quarter?

Positive Developments

-

Demand Recovery in January: January bookings up 11% and billings up 8% per day vs prior year. "We're seeing improvement across our customer base, which is a good sign for healthier underlying demand."

-

Greif Integration Progress: Both acquired mills now running near PCA standard efficiencies with ~15% operational improvement. No planned outages in H1 2026.

-

Consumer Sentiment Shift: Management noted "a much more positive vibe across our entire customer base right now" with less uncertainty vs. 2025.

-

Pricing Gains: Packaging segment benefited from +$0.50 per share in higher prices and mix.

-

Share Repurchases: 760,000 shares at $201 average in Q4.

Negative Developments

-

December Volume Miss: "December got off to a strong start... Later in the month, customers appeared to manage their already low inventories further down for year-end."

-

Wallula Mill Restructuring: $128M in charges for discontinuing the No. 2 machine and kraft pulping activities.

-

Greif Inventory Overhang: Acquired plants finished Q4 with higher inventory than forecast due to purchase/trade commitments and lower-than-expected shipments. Will take 2 quarters to optimize.

-

Legacy Volume Weakness: Corrugated shipments down 1.7% vs Q4 2024's record quarter.

How Did the Segments Perform?

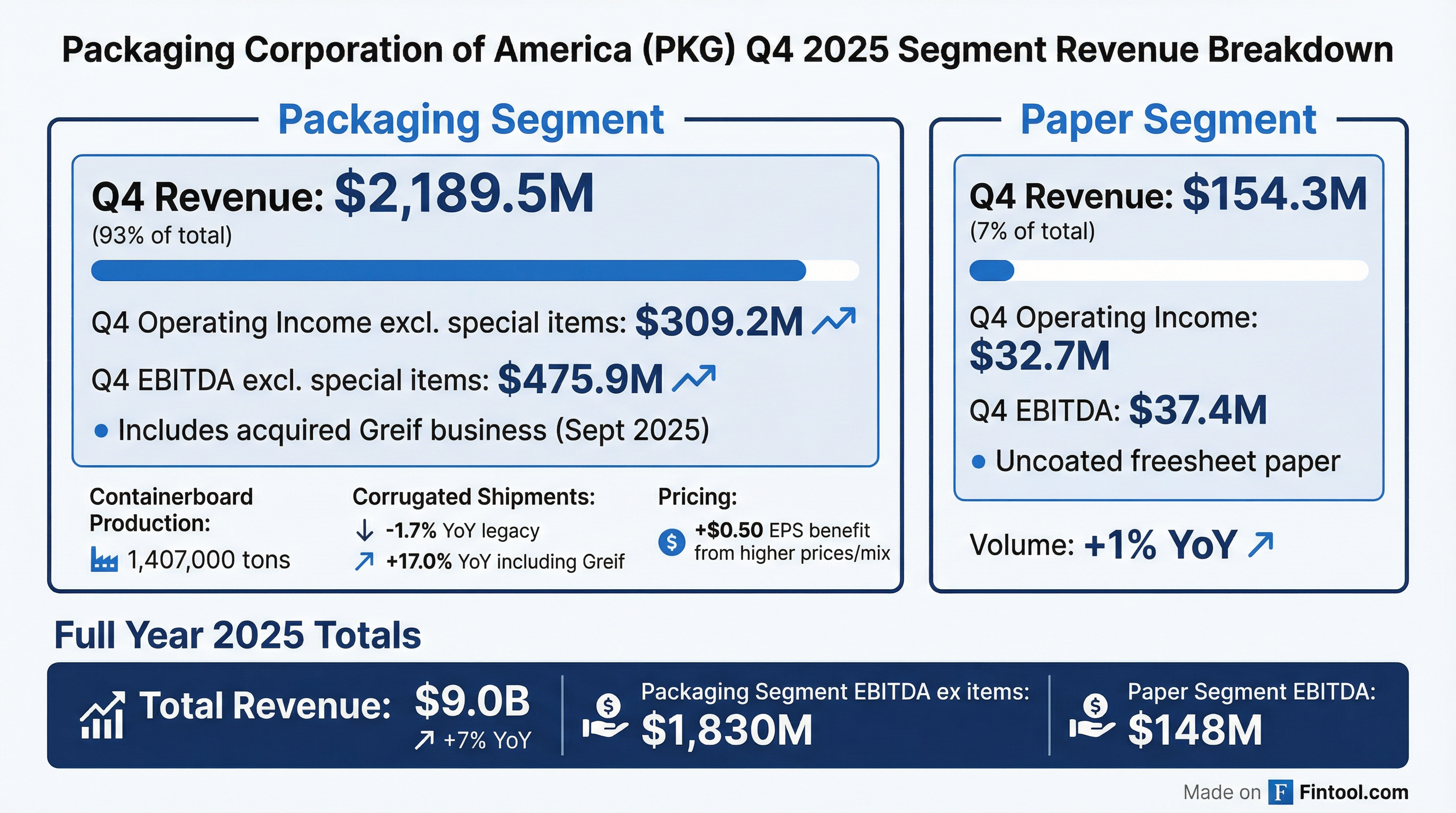

Packaging Segment (93% of Revenue)

Volume Metrics:

- Legacy corrugated shipments per day: -1.7% YoY, +4.2% QoQ

- Including Greif: +17.0% YoY, +16.5% QoQ

- Containerboard production: 1,407,000 tons

- Inventory: +84,000 tons YoY (primarily from acquisition)

Paper Segment (7% of Revenue)

Sales volume +1% YoY but down 4% from seasonally stronger Q3.

How Did the Stock React?

PKG closed at $223.62 on January 27 and traded down to $221.99 in after-hours following the earnings release — a decline of approximately 0.7%.

Beat/Miss History (Last 8 Quarters)

PKG has missed EPS estimates in 3 of the last 4 quarters, though the stock has held up well with full-year adjusted EPS growth of 9%.

Capital Allocation Update

Q4 2025 Capital Spending: $319.0M

Full Year 2025 Capital Spending: $828.9M vs. $669.7M in 2024

2026 CapEx Guidance: $840-870M

Cash Position: $667.8M in cash, equivalents, and marketable securities (vs. $852.2M at year-end 2024)

Share Repurchases: 760,000 shares at $201 average in Q4, ~$283M remaining authorization

Gas Turbine Energy Projects — $250M Investment

Management announced plans to install gas turbines at two mills over the next 30 months:

- Total investment: ~$250M (most in 2027-2028)

- Expected returns: Mid- to high-teens

- Strategic benefit: Electricity independence at these facilities

- Status: Finalizing scope, seeking board approval in Q1

A third installation at another mill is also under consideration.

Special Items Detail

Q4 2025 included $1.19 per share in special items:

The Wallula, WA mill restructuring involves discontinuing the No. 2 machine and kraft pulping activities, with cost benefits expected starting in March 2026.

Forward Estimates

Estimates via S&P Global

Management's Q1 2026 EPS guidance of $2.20 is 3.5% below consensus of $2.28, suggesting potential downward revisions ahead.

Q&A Highlights

On January Demand Strength

The most bullish commentary came on January order trends:

"January bookings in our legacy corrugated and sheet plants are up over 11%, and billings are up 8% on a per-day basis through last Thursday. We're seeing improvement across our customer base, which is a good sign for healthier underlying demand." — Tom Hassfurther, President

Management attributed the improvement to several factors:

- Customer inventories at "bare bones" levels that can't be sustained

- GDP up >4% last quarter, projected >5% this quarter

- Consumer wages now ahead of inflation for first time in 4+ years

- Housing showing signs of recovery with mortgage rates under 6%

On Running Mills Full Out in 2026

When asked if demand had truly inflected, CEO Kowlzan was emphatic:

"If we had the two extra days, we'd still be running full. The way we've looked at the entire year for the full 2026, we expect to run the entire mill system full out... which is a high-class problem to have."

On Greif Accretion Timeline

CFO Kent Pflederer confirmed the Greif acquisition is on track:

- Q1 2026: Expected to be "slightly accretive"

- Synergies: LTM EBITDA framework of ~$240M and ~$20M run rate synergies by Q2 remains intact

- 2026 outlook: Accretion improving as seasonality improves through the year

On the "Massillon Mill Rebuild"

CEO Kowlzan described an aggressive approach to fixing acquired assets:

"We learned a lesson from Boise... In a 3.5-month period of time, we've essentially rebuilt the Massillon Mill, so it's become the little mill that could. We've improved operational efficiency at both Massillon and Riverville... probably a 15% improvement overall."

On End Market Recovery

Lagging segments are finally showing life:

"Auto building products, durables, those segments were down and continued to be down all the way through the fourth quarter... And we're seeing some pickup in that area, and that's a real positive for us because those are still large segments for us." — Tom Hassfurther

Key Catalysts to Watch

- March Containerboard Price Increases: $70/ton increase effective March 1, full benefit in Q2+

- Greif Integration: No planned mill outages in H1 2026; targeting slight accretion in Q1

- Wallula Reconfiguration: Cost benefits begin in March 2026

- January Demand Durability: Bookings +11%, billings +8% — sustainability through Q1 is key

- Winter Storm Impact: Potential negative impact from plant downtime and transportation disruptions

- Gas Turbine Projects: Board approval expected Q1, mid-high teens returns

Management Tone Shift

Analysts on the call noted a "clear inflection" in management's tone. President Tom Hassfurther explained the difference vs. last year:

"How does it feel for us? I mean, it feels improved. In fact, much improved... A new administration was gonna take hold. A lot of things were up in the air. We were already dealing with potential tariff stuff... Those are all pretty well cleared up at this point in time."

Key macro tailwinds cited:

- GDP up >4% last quarter, projected >5% this quarter

- First time in 4+ years that wages are ahead of inflation

- Mortgage rates under 6%, supporting housing recovery

Related Links

Analysis based on Q4 2025 earnings call held January 28, 2026.