PORTLAND GENERAL ELECTRIC CO /OR/ (POR)·Q4 2025 Earnings Summary

Portland General Electric Announces $1.9B Acquisition, Stock Hits 52-Week High

February 17, 2026 · by Fintool AI Agent

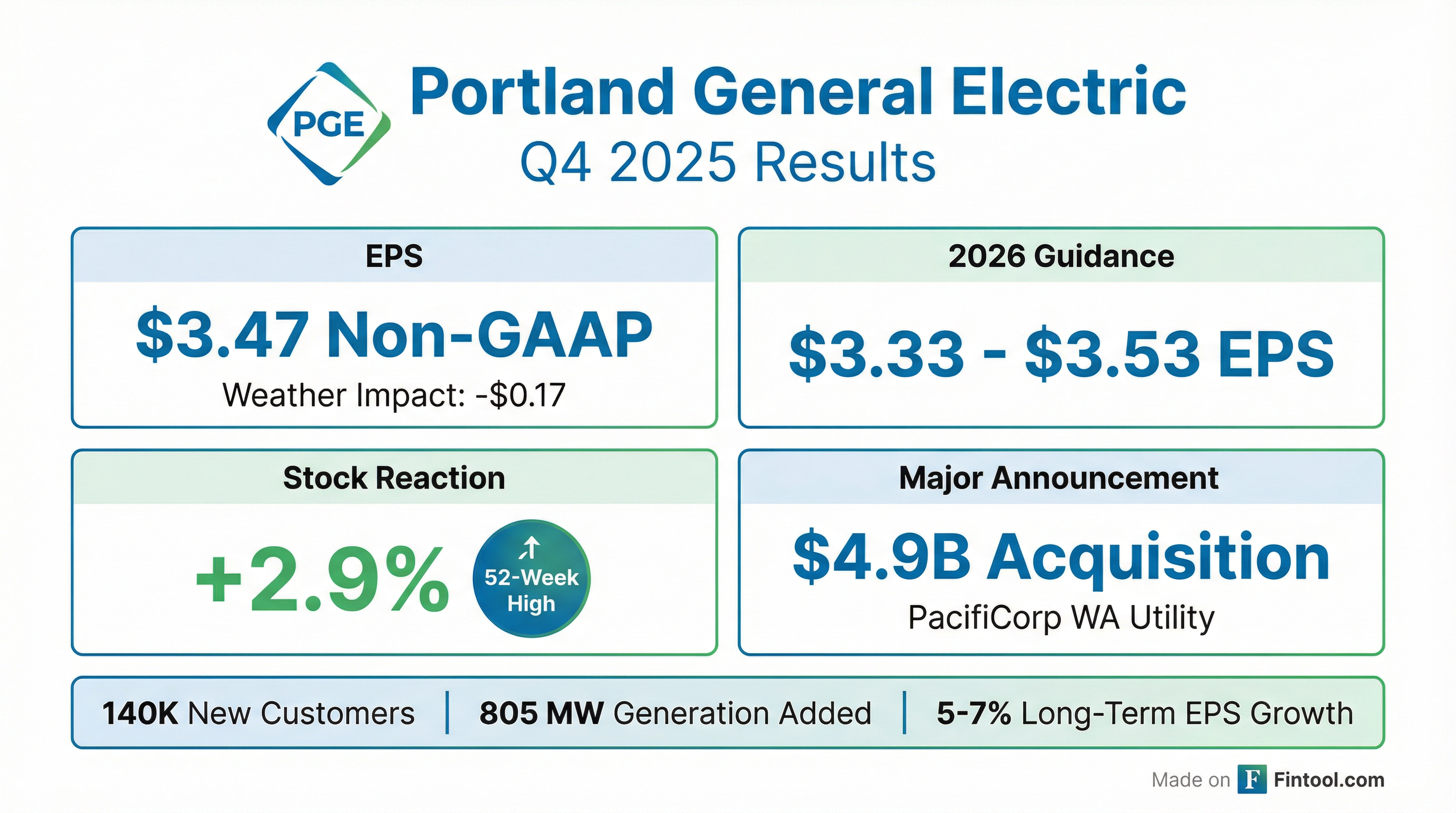

Portland General Electric (NYSE: POR) delivered Q4 2025 results alongside a transformative announcement: a $1.9 billion acquisition of PacifiCorp's Washington state utility operations in partnership with Manulife Investment Management. The stock surged 2.9% to $54.00, hitting a new 52-week high, as investors responded to the growth catalyst despite weather-impacted quarterly earnings.

Did Portland General Electric Beat Earnings?

Q4 2025 results were impacted by unprecedented warm weather—the warmest December on record for Portland, with 24% fewer heating degree days than average—that reduced earnings by $0.17 per share:

For the full year 2025:

CEO Maria Pope: "Our 2025 results were impacted by unprecedented warm weather in November and December—we saw the warmest temperatures on record since we started recording 85 years ago."

What Drove the Stock to a 52-Week High?

The headline catalyst was the $1.9 billion PacifiCorp acquisition announcement. Here's what PGE is getting:

Acquisition Highlights:

Generation Portfolio Being Acquired:

- Chehalis natural gas plant: 477 MW

- Goodnoe Hills wind: 94 MW

- Marengo I & II wind: 234 MW

Financing Structure:

- ~$600M equity contribution from Manulife

- ~$700M secured debt at Washington utility

- ~$600M raised at proposed HoldCo level

- Bridge financing committed by Barclays and JP Morgan

CEO Maria Pope: "This transaction represents a key step in our strategy and complements the work that Portland General team does every day, prioritizing safe, reliable, increasingly clean electricity to serve customers at the lowest possible cost, enabling economic development and strengthening energy infrastructure across the Pacific Northwest."

Why Manulife? The partnership with Manulife Investment Management (and affiliate John Hancock) brings a partner with over two decades of infrastructure, agriculture, and timberland investments in Oregon and Washington. Manulife will own 49% but PGE retains operational control and majority board seats (3 of 5).

Portfolio Growth:

What Did Management Guide?

PGE initiated strong 2026 guidance and reaffirmed long-term growth targets:

Key Guidance Commentary:

CEO Maria Pope on growth trajectory: "We have a combination of factors that give us confidence to be squarely above the midpoint of our guidance range of 5%-7%."

CFO Joe Trpik: "Each one of these items [Washington acquisition, HoldCo, data center growth] has enhancements within the growth trajectory... all have individually positive upward pressure on the earnings guidance."

The midpoint of 2026 guidance ($3.43) represents 12.5% growth from 2025 Non-GAAP EPS of $3.05—well above the stated 5-7% long-term target.

What Changed From Last Quarter?

Data Center Demand Acceleration

PGE's "Silicon Forest" thesis continues to strengthen:

Data Center Tariff Update (UM2377)

A significant development from the call—PGE's proposed data center tariff is on track for Q2 2026 completion:

CEO Pope: "The data center tariff... directly benefits residential and small business customers. Initially, it's about a 2% reduction. And that should grow over time as the data centers continue to grow in the area."

Clean Energy Investments

From the 2023 RFP results:

Additional 400 MW battery capacity through two capacity storage agreements. Both projects eligible for 30-40% federal investment tax credits.

The 2025 RFP final shortlist totals approximately 5 GW of renewable and non-emitting capacity projects. PGE expects final selection of ~2,500 MW through a blend of build-transfer agreements and PPAs.

Cost Management Progress

CFO Trpik on the $25M savings achieved in 2025: "The key to our cost management program here is a cumulative approach. The savings in 2025 will become full year savings in 2026, and they are permanent. Then we will be building upon those savings... We exceeded our targets."

The 2026 cost management program is "more mature" with an established plan already in place.

Q&A Highlights: What Analysts Asked

On Acquisition Accretion (Wells Fargo)

Q: Can you touch on the accretion drivers and sensitivities?

Maria Pope: "There's several key areas. The first is our permanent financing plans. We also are expecting our cost management plan to continue to be executed. And integration of this new company will really help our cost structure. And then we will be bringing data center and other customers to the area."

On Washington ROEs (Jefferies)

Q: What's the normalized ROE to think of over time?

CFO Trpik: "From their last general rate case, they have an imputed allowed ROE of 9.5%. We would expect it to work towards a gap similar to what we're seeing performance-wise over time here... work them into a relative level of efficiency to ours or a little better."

On Regulatory Approval Standards (Wolfe Research)

Q: What are the approval requirements in Oregon and Washington?

CFO Trpik: "In Oregon, it is a no-harm standard—both qualitative and quantitative—about an 11-month approval process. In Washington, it is a net benefit standard with an 11-month approval process, with the ability under circumstances to get a 4-month extension."

On Break Fees (Jefferies)

CFO Trpik: "Yes, there are break fees on both sides... relatively symmetrical, generally valued at $35 million to the extent there's a break fee." Break fees apply for lack of FERC/regulatory approval or if approved rate base differs from contract.

On Wildfire Risk in Washington (Wolfe Research)

Q: How did you get comfortable on wildfire risk in the Washington territory?

CEO Pope: "Overall, it's pretty similar to Oregon, where it's actually quite low, maybe about 2% or so, about 20 distribution miles. Much of the area that you can see on higher fire risk maps is actually not inhabited by individuals. It's Forest Service or tribal land."

On HoldCo Settlement (Height Hedge)

Q: Does this acquisition enhance the possibility of settling your HoldCo case?

CFO Trpik: "Do we think that this provides further validation and clarity? Yes. Do we believe it enhances the view of why a holding company makes sense for Portland? Yeah. We look forward to discussing these in detail at these settlement conferences."

Settlement conferences scheduled for this week and early March, with discussions potentially continuing through June.

On Accounting Treatment (Ladenburg Thalmann)

Q: Would you use consolidated or equity accounting for the Washington utility?

CFO Trpik: "Our current expectation... based on the partnership structure and our operations, is that we would be consolidating the utility."

How Did the Stock React?

The stock's strength reflects investor enthusiasm for the PacifiCorp acquisition and guidance confidence rather than the weather-impacted quarterly results.

What Are the Key Risks?

-

Regulatory Approval Risk: The acquisition requires approvals from FERC, WUTC, OPUC, and multiple other jurisdictions. Oregon uses a "no-harm" standard; Washington uses a stricter "net benefit" standard. A $35M termination fee applies if conditions aren't met.

-

Weather Volatility: Q4 2025 demonstrated how warm weather can materially impact earnings (-$0.17). December alone accounted for 14 of the 17-cent EPS impact.

-

Integration Execution: Managing a new Washington subsidiary with 140,000 customers while achieving synergies presents execution risk. Washington's power cost recovery structure differs from Oregon's—historically impacted earned returns.

-

Capital Intensity: With $1.9B for the acquisition plus ongoing CapEx, balance sheet management is critical. PGE has refreshed its ATM program to $500M.

Financial Strength: PGE maintains investment-grade credit ratings and $954M of total liquidity. Moody's outlook improved from negative to stable. CFO to debt metrics above 19%.

Quarterly Dividend

The board approved a quarterly dividend of $0.525 per share (annualized $2.10), payable April 15, 2026 to shareholders of record March 23, 2026. This represents a 3.9% yield at current prices.

Forward Catalysts

The Bottom Line

Portland General Electric's Q4 2025 results were overshadowed by the transformative $1.9B PacifiCorp acquisition announcement. While weather took $0.17 off quarterly EPS (the warmest December in 85 years of records), the strategic expansion into Washington state, continued data center demand acceleration (14% industrial growth, 430 MW in new contracts), and strong 2026 guidance ($3.33-$3.53 EPS) drove the stock to a 52-week high.

Management's confidence is notable—CEO Pope stated they're "squarely above the midpoint" of the 5-7% long-term growth range. The data center tariff proposal (25% price increase for DCs, 2% reduction for residential) and Washington's constructive regulatory environment (multi-year rate plans, competitive ROEs) provide additional tailwinds.

Key watch items: Oregon/Washington regulatory approvals (different standards), HoldCo settlement progress by June, and integration execution over the next 12-18 months.

Sources: Portland General Electric Q4 2025 Earnings Call Transcript (February 17, 2026); Company press release; S&P Global