PSQ Holdings (PSQH)·Q4 2025 Earnings Summary

PSQ Holdings Posts 109% Revenue Surge But Faces NYSE Delisting Warning

February 17, 2026 · by Fintool AI Agent

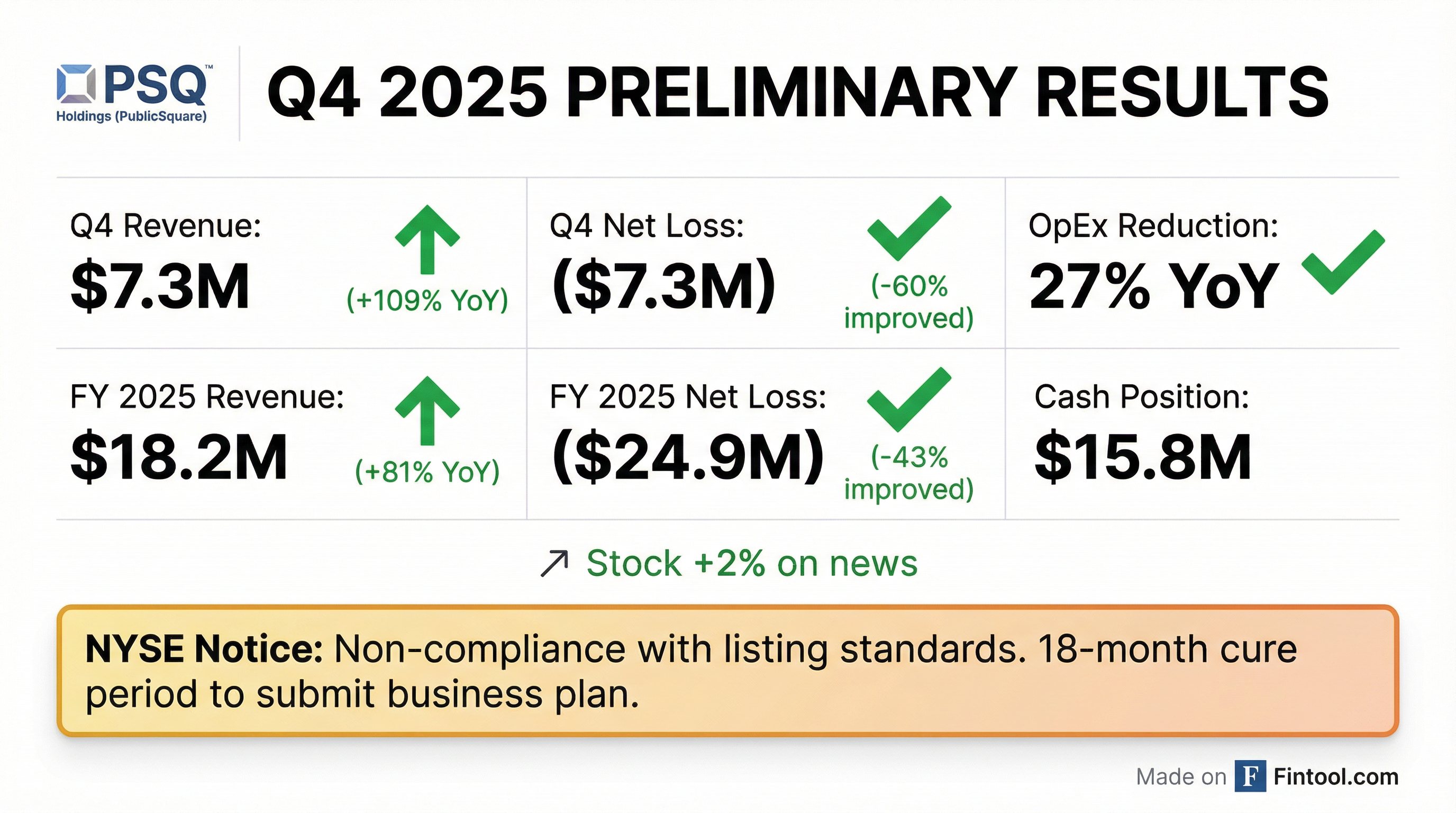

PSQ Holdings (NYSE: PSQH) delivered preliminary Q4 2025 results that showcased explosive revenue growth, with net revenue jumping 109% year-over-year to $7.3 million . However, the earnings release came packaged with troubling news: the company received an NYSE delisting notice for failing to meet minimum market cap and stock price requirements .

The payments and financial infrastructure company, formerly known as PublicSquare, has been pivoting hard into FinTech after deciding to monetize its non-core Brands and Marketplace businesses . Full-year 2025 revenue reached $18.2 million, up 81% from $10.1 million in 2024 . The stock rose approximately 2% on the news, though shares remain down over 50% from three months ago.

Did PSQ Holdings Beat Earnings?

Yes — PSQ Holdings significantly beat its Q4 2025 revenue guidance. The company had guided Q4 revenue at approximately $6 million during its Q3 2025 earnings call . Preliminary results came in at $7.3 million, a 22% beat versus guidance .

The company does not provide earnings per share estimates from analysts, but management delivered on their promise of improving operating efficiency while scaling the FinTech business .

What's the NYSE Delisting Risk?

This is the elephant in the room. On February 10, 2026, PSQ Holdings received written notice from NYSE that it is not in compliance with two critical listing rules :

- Rule 802.01B — Minimum market cap and stockholders equity requirements

- Rule 802.01C — Minimum average closing stock price of $1.00

The notice does not result in immediate delisting .

Cure Timeline

The company intends to notify NYSE within 10 business days of its intent to cure and will submit a business plan within 45 days . If NYSE accepts the plan, the company will be subject to quarterly monitoring .

Current stock price: ~$0.78 — well below the $1.00 threshold. The stock would need to rally approximately 30% just to regain compliance.

What Did Management Say?

New CEO Dusty Wunderlich, who was appointed in late January 2026, struck a measured tone emphasizing execution and discipline :

"These preliminary results reflect continued execution across our platform and the early impact of tighter operating discipline, coupled with the use of AI as a force multiplier. We are leveraging advanced tools to accelerate execution, increase efficiency, and enhance our operational tempo."

On the path forward, Wunderlich outlined clear priorities :

"Our priorities are clear: improve unit economics, execute with discipline, strengthen the balance sheet, and reduce cash burn. We intend to rebuild trust the right way, through consistent performance and a credible path to profitability."

This marks a notable shift from founder Michael Seifert, who led the company through its aggressive expansion phase in 2024 and early 2025.

How Did Full-Year 2025 Perform?

Full-year 2025 results (continuing operations only, excluding discontinued Brands and Marketplace segments) showed meaningful progress :

Including discontinued operations, the company reported :

- Net loss of $36.6 million vs. $57.7 million in 2024

- Loss per share of ($0.80) vs. ($1.80)

- Cash of $16.1 million including $1.2 million restricted

What Changed From Last Quarter?

Comparing Q4 2025 to Q3 2025 guidance and results:

Key changes since Q3:

- Revenue accelerated significantly (+66% QoQ vs +37% in Q3)

- CEO transition: Dusty Wunderlich replaced Michael Seifert

- NYSE delisting notice received

- Continued progress on EveryLife divestiture

How Did the Stock React?

The stock rose approximately +2-3% on the earnings release, closing at $0.78 on February 17, 2026. However, the broader context is challenging:

The stock has been in freefall since late 2025, driven by:

- General small-cap pressure

- Uncertainty around strategic pivot to FinTech

- Dilution from capital raises

- Now compounded by NYSE delisting concerns

What's the Forward Outlook?

Management reaffirmed 2026 guidance of ≥$32 million in revenue from continuing FinTech operations , which would represent 76%+ growth from FY 2025's $18.2 million.

Upcoming catalysts:

- Full audited FY 2025 results and 10-K filing in mid-March 2026

- EveryLife divestiture completion (expected purchase agreement by end of Q4 2025/early 2026)

- NYSE business plan submission (within 45 days)

- Launch of private label credit card program

- PSQ Impact fundraising platform launch

Key risks:

- NYSE delisting if cure plan fails

- Continued cash burn despite improvements

- Small market cap (~$36M) limits institutional interest

- Heavy dependence on niche merchant verticals (firearms-adjacent)

Key Takeaways

The Good:

- 109% YoY revenue growth demonstrates FinTech pivot gaining traction

- Operating losses narrowing significantly (-60% net loss improvement in Q4)

- Cost discipline evident with 27% YoY OpEx reduction

- $15.8M cash provides runway

The Bad:

- NYSE delisting notice creates existential overhang

- Stock price (-79% from 52-week high) reflects deep skepticism

- Still burning significant cash despite improvements

- New CEO still proving himself

Bottom Line: PSQ Holdings delivered strong operational results that beat expectations, but the NYSE delisting notice overshadows the positive developments. The company has 18 months to prove its business model works — investors will be watching closely to see if the FinTech pivot can translate into sustainable profitability and a stock price above $1.00.

This analysis is based on preliminary, unaudited financial results. Final audited results will be released in mid-March 2026.