Earnings summaries and quarterly performance for Phillips 66.

Research analysts who have asked questions during Phillips 66 earnings calls.

Manav Gupta

UBS Group

8 questions for PSX

Neil Mehta

Goldman Sachs

8 questions for PSX

Jason Gabelman

TD Cowen

7 questions for PSX

Matthew Blair

Tudor, Pickering, Holt & Co.

6 questions for PSX

Paul Cheng

Scotiabank

6 questions for PSX

Ryan Todd

Simmons Energy

6 questions for PSX

Theresa Chen

Barclays PLC

6 questions for PSX

Jean Ann Salisbury

Bank of America

4 questions for PSX

Douglas George Blyth Leggate

Wolfe Research

3 questions for PSX

Doug Leggate

Wolfe Research

3 questions for PSX

John Royall

JPMorgan Chase & Co.

3 questions for PSX

Phillip Jungwirth

BMO Capital Markets

3 questions for PSX

Roger Read

Wells Fargo & Company

3 questions for PSX

Douglas Leggate

Wolfe Research

2 questions for PSX

Joseph Laetsch

Morgan Stanley

2 questions for PSX

Justin Jenkins

Raymond James

2 questions for PSX

Lloyd Byrne

Jefferies LLC

2 questions for PSX

Sam Margolin

Wells Fargo & Company

2 questions for PSX

Stephen Richardson

Evercore ISI

2 questions for PSX

Steve Richardson

Evercore

2 questions for PSX

Joe Laetsch

Morgan Stanley

1 question for PSX

Theresa Chinn

Barclays

1 question for PSX

Recent press releases and 8-K filings for PSX.

- Phillips 66 has appointed Howard Ungerleider and Kevin Meyers to its Board of Directors, effective immediately.

- The additions follow constructive engagement with Elliott Investment Management and are intended to strengthen board expertise in finance, operations and energy.

- Long-time directors Glenn Tilton and Marna Whittington will retire at the May 2026 annual meeting, after which the board will total 14 members (13 independent); Ungerleider will serve as a Class II director and Meyers as a Class III director.

- Ungerleider brings over 30 years of financial leadership, including roles as CFO of Dow Inc. and DowDuPont, while Meyers offers 40+ years in oil & gas, retiring as SVP of ConocoPhillips Exploration & Production Americas.

- Integrated operations across midstream, refining, and CPChem drive resilient cash flows, with a 15% CAGR dividend over 13 years and commitment to return ≥50% of cash flow to shareholders quarterly.

- Refining turnaround since late 2021 reduced costs by >$1/bbl, improved utilization and clean product yield, with an inflection realized in 2025.

- Midstream EBITDA of $4 billion in 2025, targeting $4.5 billion by end-2027 through disciplined investments and expanded global origination.

- CPChem operates >100% capacity in North America (exporting >50% of production), with Middle East events poised to tighten cost curves and supply/demand in petrochemicals.

- Portfolio optimization: $5.5 billion divested non-core assets redeployed into high-return midstream acquisitions; capital plan allocates ~50% of $8 billion cash flow to $2 billion dividends, $2 billion buybacks, and ~$2 billion debt paydown annually toward $17 billion debt target by 2027.

- Integrated model driving durable cash flows: Phillips 66 leverages refining, midstream and its 50/50 CPChem JV to capture countercyclical earnings. Refining cost cuts of >$1/bbl since 2021 and portfolio‐wide EBITDA up ~40% to $4 billion, with a target of $4.5 billion by end-2027.

- Midstream build-out in Permian: completed DCP roll-up, acquired Pinnacle and the Epic (Coastal Bend) pipeline, and advancing Iron Mesa (300 kbd) to replace Goldsmith, all aimed at achieving $4.5 billion midstream EBITDA by 2027.

- Capital allocation: committed to returning ≥50% of operating cash flow. For 2026–27, projected $8 billion FCF split into $2 billion dividends, $2 billion share buybacks, $2 billion capex and $2 billion debt reduction to reach $17 billion net debt by 2027.

- Petrochemicals outlook: CPChem operating >100% rates in a downcycle; potential normalization of global cost curves—driven by reduced Chinese crude discounts and Middle East supply constraints—could catalyze the next upcycle.

- Phillips 66 reaffirmed its commitment to return at least 50% of operating cash flow to shareholders each quarter, with dividends growing at a ~15% compounded annual rate over 13 years and a recent increase declared.

- The company has reduced refining costs by $1+ per barrel since 2021, achieved record clean product yields and higher asset utilization, marking a 2025 inflection from these operational improvements.

- Midstream integration is driving growth: after the DCP roll-up and acquisitions like Pinnacle and EPIC (now Coastal Bend), Phillips 66 expects midstream EBITDA to reach $4.5 billion by end-2027, underpinned by accretive assets and organic expansions.

- The Western Gateway pipeline—conceived under a fully integrated refining-midstream-marketing strategy—completed a successful first open season and is in a second phase to secure Gulf Coast and Midcontinent commitments ahead of a final investment decision.

- With an $8 billion cash flow outlook for 2026–27, the company plans to allocate 50% to shareholder returns (~$2 billion dividends, ~$2 billion buybacks), ~$2 billion in capital spending and $1.5 billion annual debt reduction toward a $17 billion target.

- No cash distribution declared for unitholders of record February 27, 2026 for December 2025, as net profits did not cover the Trust’s administrative expenses and debt obligations, making future distributions highly unlikely.

- As of the end of the period, the Trust’s outstanding debt to PCEC, including drawn letters of credit and loans with accrued interest, totaled approximately $12.7 million.

- Under the Trust Agreement, dissolution is triggered because annual cash proceeds were below $2.0 million for both 2020 and 2021, initiating wind-up and potential asset sale.

- PCEC recorded upward adjustments to Asset Retirement Obligations of $459,000 (Developed Properties) and $140,000 (Remaining Properties) for the period, and will continue monthly accretion adjustments.

- Phillips 66 delivered strong Q4 and full-year 2025 results, achieving record safety performance, high refinery utilization with record clean product yields, and midstream adjusted EBITDA of ~$1 billion in Q4, up 40% since 2022.

- Refining controllable cost was $5.96/barrel in Q4 (excluding Los Angeles idling costs items would be ~$5.50/barrel); company targets $5.50/barrel by end-2027 and idled the 135 kbd Los Angeles refinery to optimize the asset base.

- Midstream segment targets a run-rate $4.5 billion adjusted EBITDA by year-end 2027 via organic expansions (Permian gas plants every 12–18 months, Iron Mesa online early 2027) and pipeline growth (Coastal Bend +125 kbd by late 2026).

- Portfolio optimization included acquiring the remaining 50% of the WRB JV (boosting heavy crude exposure by 40%), selling a 65% stake in the Germany/Austria retail business, and idling the Los Angeles refinery to streamline operations and enhance returns.

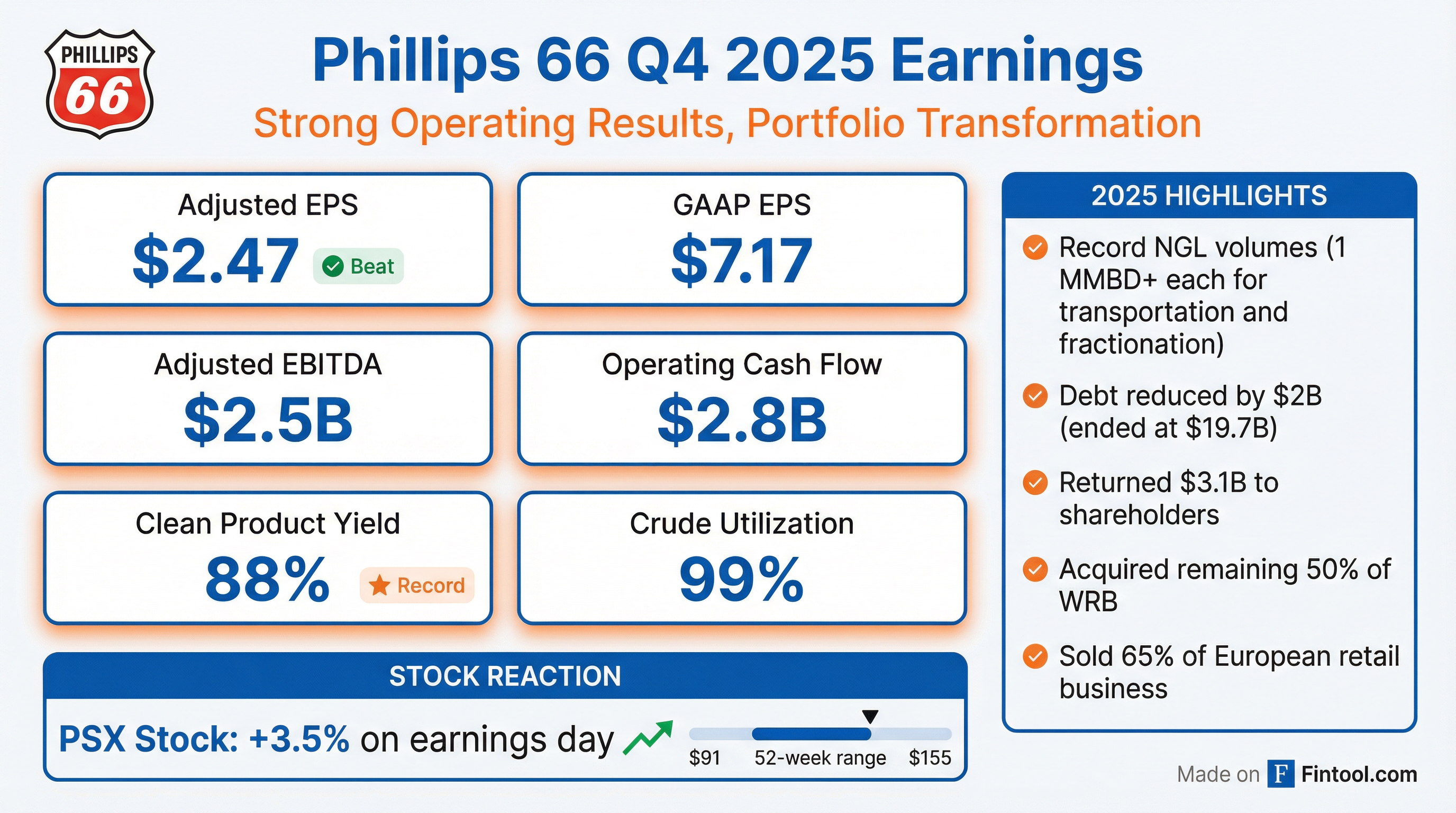

- Reported Q4 earnings of $2.9 billion ($7.17/share) and adjusted earnings of $1.0 billion ($2.47/share); generated $2.8 billion of operating cash flow, spent $682 million of capital, repaid over $2 billion of debt, and returned $756 million to shareholders (including $274 million of share buybacks); net debt to capital ended at 38%.

- Operational & portfolio highlights: best-ever safety performance; record clean product yields and high utilization across refining; record NGL transportation and fractionation volumes with ~$1 billion of midstream adjusted EBITDA; completed acquisition of the remaining 50% of WRB JV, sold 65% of Germany/Austria retail business, and idled the Los Angeles refinery.

- 2026 guidance: Q1 global refining/utilization mid-90s%; corporate & other costs of $400–420 million (Q1) and $1.5–1.6 billion (FY); depreciation & amortization of $2.1–2.3 billion; turnaround expenses of $170–190 million (Q1) and $550–600 million (FY).

- Refining cost reduction target: Q4 controllable cost of $5.96/barrel (or $5.50–5.57 ex-Los Angeles idling) against a goal of $5.50/barrel by end-2027, with a $0.30 annual tailwind in 2026 from LA idling and an additional $0.15/barrel expected from continuous improvement initiatives.

- Delivered strong Q4 results with high refining utilization rates, record clean product yields, and best-ever safety performance; optimization initiatives target $5.50 controllable cost per barrel by end of 2027

- Executed strategic portfolio actions: acquired remaining 50% of WRB JV, sold 65% of Germany/Austria retail business, idled Los Angeles refinery; expanded NGL volumes via Coastal Bend and Dos Picos II

- Midstream segment achieved ~$1 billion adjusted EBITDA in Q4 2025 (up 40% since 2022); projects on track for $4.5 billion run-rate EBITDA by year-end 2027 with gas plants every 12–18 months and 125 kbpd pipeline expansion

- Q4 reported earnings of $2.9 billion ($7.17/share) and adjusted earnings of $1 billion ($2.47/share); generated $2.8 billion operating cash flow, spent $682 million on capex, returned $756 million to shareholders, and net debt/capital at 38%

- 2026 outlook includes Q1 global utilization in mid-90s, corporate costs of $400–420 million in Q1 and $1.5–1.6 billion full-year, D&A of $2.1–2.3 billion, and $550–600 million of full-year turnaround expenses

- Phillips 66 reported Q4 earnings of $2.9 billion ($7.17/share) and adjusted earnings of $1.0 billion ($2.47/share), including $239 million of pre-tax accelerated depreciation at its Los Angeles Refinery.

- The company generated $2.8 billion of net operating cash flow ($2.0 billion ex-working capital) and reduced debt by $2.0 billion, ending 2025 with $19.7 billion of debt.

- Operationally, Refining achieved a record clean product yield of 88% and 99% crude capacity utilization, while Midstream set new records with NGL transportation and fractionation volumes each exceeding 1 MMBD.

- For full-year 2025, Phillips 66 earned $4.4 billion ($10.79/share) and adjusted $2.6 billion ($6.44/share), generated $5.0 billion of operating cash flow ($6.1 billion ex-working capital) and returned $3.1 billion to shareholders (>50% of cash flow).

- Strategic portfolio actions included selling the majority of its European retail business, acquiring the remaining 50% interest in WRB Refining LP, and enhancing its Midstream position through the Coastal Bend acquisition and Dos Picos II expansion.

- Phillips 66 delivered fourth-quarter earnings of $2.9 billion (or $7.17 per share) and adjusted earnings of $1.0 billion (or $2.47 per share), including $239 million of pre-tax accelerated depreciation on the Los Angeles Refinery.

- Achieved record NGL transportation and fractionation volumes of over 1 million barrels per day, an 88% clean product yield and 99% crude capacity utilization in refining.

- Generated $2.8 billion of net operating cash flow ($2.0 billion excluding working capital) and reduced debt by $2.0 billion, ending the year with $19.7 billion of debt.

- Enhanced portfolio through sale of its European retail business, acquisition of the remaining 50% of WRB Refining and midstream expansions including Coastal Bend and Dos Picos II.

Quarterly earnings call transcripts for Phillips 66.

Ask Fintool AI Agent

Get instant answers from SEC filings, earnings calls & more