RESIDEO TECHNOLOGIES (REZI)·Q4 2025 Earnings Summary

Resideo Beats on Revenue, Surges 11% as Separation Unlocks Value

February 24, 2026 · by Fintool AI Agent

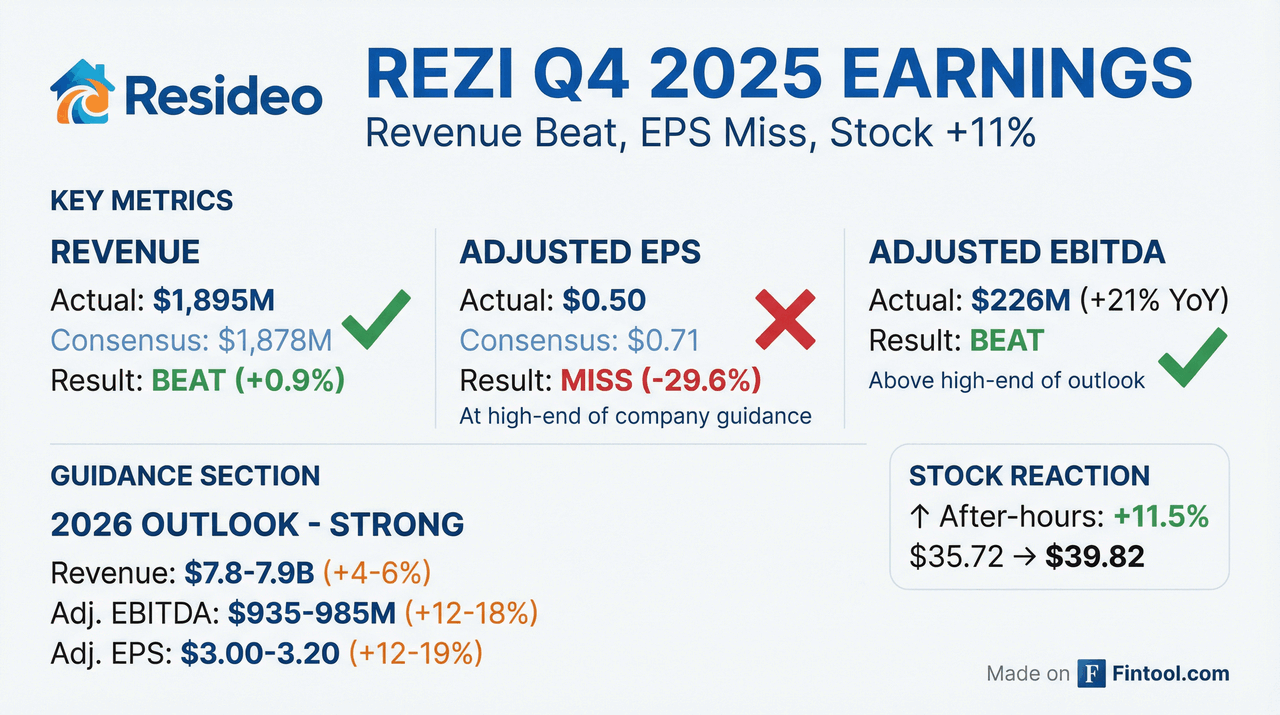

Resideo Technologies (NYSE: REZI) delivered Q4 2025 results that beat on revenue while missing EPS consensus, but the stock surged 11% after-hours to $39.82 as investors focused on strong 2026 guidance and the company's announcement to separate into two independent public companies.

The quarter capped a record year for Resideo, with FY25 marking all-time highs in revenue ($7.47B), Adjusted EBITDA ($833M), and Adjusted EPS ($2.68).

Did Resideo Beat Earnings?

Revenue: BEAT — Q4 revenue of $1.895B exceeded consensus of $1.878B by 0.9% and came in above the high-end of company guidance.

EPS: MISS vs Consensus, IN LINE with Guidance — Adjusted EPS of $0.50 missed the Street's $0.71 estimate by 29.6%, but was at the high-end of management's outlook range. The EPS decline vs prior year ($0.59 in Q4'24) reflects higher interest expense from the debt raised to terminate the Honeywell Indemnification Agreement.

Adjusted EBITDA: BEAT — Q4 Adjusted EBITDA of $226M (+21% YoY) exceeded the high-end of outlook, with margin expanding 180bps to 11.9%.

How Did the Stock React?

REZI shares closed at $35.72 on the regular session (+2.3%) before surging to $39.82 after-hours — an 11.5% pop on the earnings release.

The positive reaction despite the EPS miss reflects investor enthusiasm for:

- All metrics above high-end of guidance — Management delivered on every key metric

- Accelerating 2026 outlook — Guided EPS growth of 12-19% YoY

- Business separation — Two pure-play companies to unlock sum-of-parts value

- Honeywell overhang removed — Terminated $140M/year Indemnification Agreement

What Did Management Guide?

Management issued strong 2026 guidance, projecting meaningful acceleration across all key metrics:

The EBITDA and EPS guidance acceleration reflects the full-year benefit of eliminating the Honeywell Indemnification Agreement, which immediately unlocked $35M of quarterly EBITDA.

What Changed From Last Quarter?

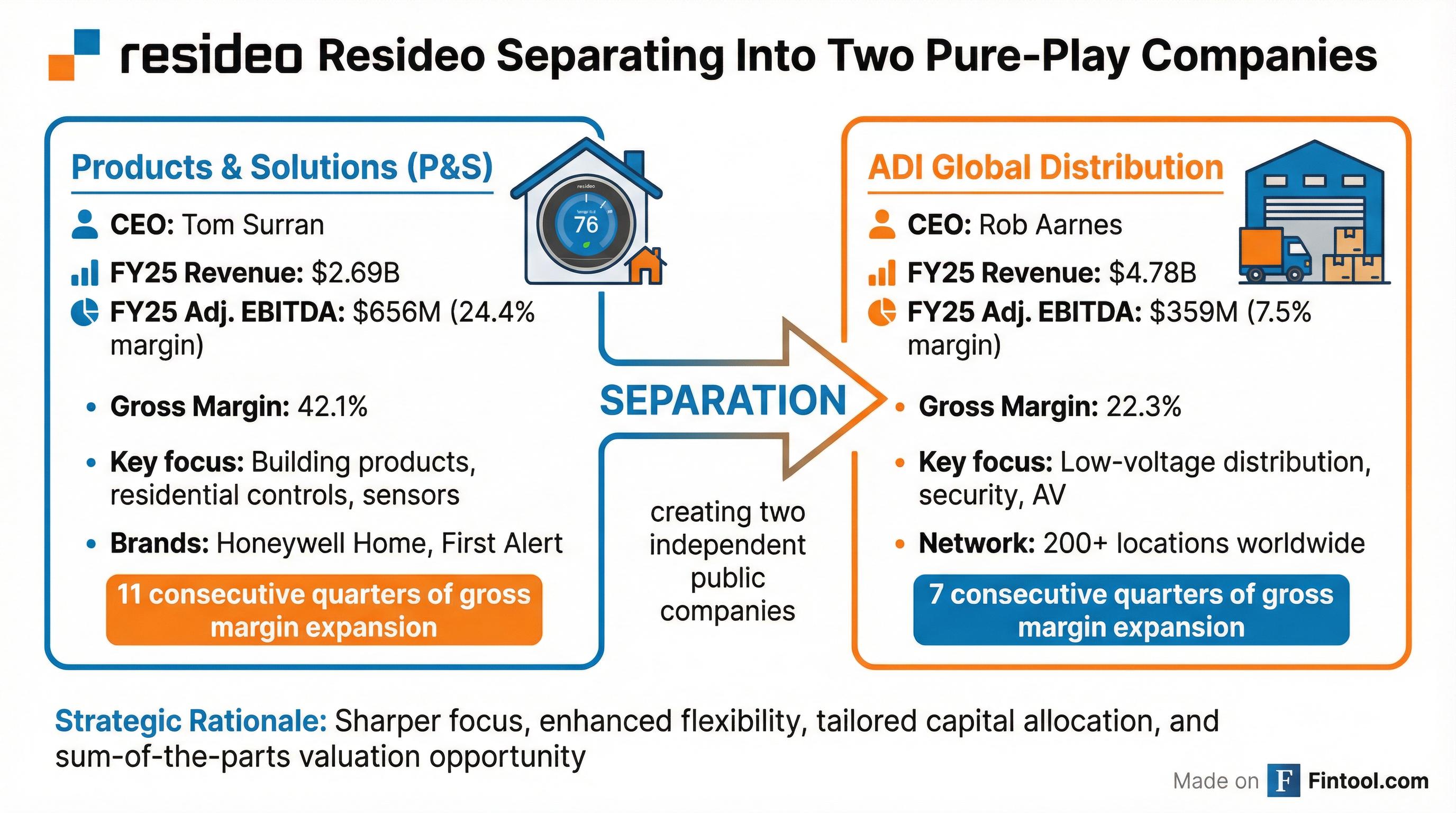

Business Separation Announced

The most significant development is Resideo's plan to separate into two independent publicly traded companies:

Products & Solutions (P&S) — Led by President Tom Surran, this segment will focus on residential controls and sensing solutions under brands like Honeywell Home and First Alert. FY25 delivered $2.69B revenue with 42.1% gross margin and 24.4% Adjusted EBITDA margin.

ADI Global Distribution — Led by President Rob Aarnes, this segment is a leading wholesale distributor of security and AV products with 200+ locations worldwide. FY25 delivered $4.78B revenue with 22.3% gross margin and 7.5% Adjusted EBITDA margin.

Honeywell Overhang Removed

In August 2025, Resideo made a one-time $1.59B payment to Honeywell to terminate the Indemnification Agreement — a legacy obligation from the 2018 spin-off that required $140M in annual payments through 2043.

The termination:

- Eliminated ongoing payments and related covenants

- Unlocked $35M of quarterly EBITDA immediately

- Is immediately accretive to Adjusted EPS and cash flow

- Enabled the separation transaction

Segment Performance

Products & Solutions: Steady Growth

P&S delivered Q4 revenue of $712M (+6% YoY), driven by price realization in the OEM channel and new product demand in electrical distribution and retail. Gross margin expanded 20bps to 41.0%, marking 11 consecutive quarters of year-over-year margin expansion.

Air products remain soft due to a weak residential HVAC market, but are "improving" per management.

ADI Global Distribution: Margin Expansion Continues

ADI posted Q4 revenue of $1,183M (-1% YoY), impacted by declines in video surveillance that offset growth in commercial security and professional AV. The story here is margin — gross margin expanded 110bps to 22.7%, the seventh consecutive quarter of year-over-year improvement.

E-commerce revenue grew 3% YoY and Exclusive Brands grew 2% YoY, reflecting positive momentum from new products and digital adoption.

Balance Sheet & Cash Flow

The balance sheet reflects the Honeywell termination financing:

Q4 cash from operations was strong at $299M, driven by cash collections and the benefit of eliminating the Indemnification Agreement payments.

For FY25, reported cash used in operations was negative $1.14B due to the $1.59B Honeywell payment. Adjusted for this one-time item, cash provided by operations was $453M.

Key Risks & Considerations

-

Leverage — Gross debt increased to $3.2B from $2.0B to fund the Honeywell termination, creating meaningful interest expense headwind

-

Separation execution risk — Separating into two public companies involves operational disruption and significant one-time costs

-

Tariff exposure — Management flagged tariff-related risks in the forward-looking statements

-

HVAC market softness — Air products remain challenged by weak residential HVAC demand

-

Video surveillance decline — ADI continues to see pressure in this category

Management Quotes

"In 2025, Resideo exceeded the high-end of our outlook range for all of our key financial metrics and achieved record highs in net revenue, Adjusted EBITDA and Adjusted EPS." — Jay Geldmacher, President and CEO

"The Products and Solutions and ADI teams delivered outstanding results in 2025 by demonstrating resilience and operational excellence throughout a very dynamic year. These are part of our core values that will drive future standalone success for each company post business separation." — Jay Geldmacher, President and CEO

Forward Catalysts

- Separation timeline — Execution and completion of the two-company split

- Q1 2026 earnings — First quarter showing full benefit of Honeywell termination

- Housing recovery — Potential tailwind for P&S Air products if residential HVAC improves

- Video surveillance stabilization — Potential inflection point for ADI's largest category

- Snap One synergies — Company targeting $75M+ in synergies by year 3 post-acquisition

Data sources: Resideo Q4 2025 8-K filing, Q4 2025 Earnings Presentation, S&P Global consensus estimates.