REPLIGEN (RGEN)·Q4 2025 Earnings Summary

Repligen Beats on Revenue and EPS as Bioprocessing Demand Rebounds

February 24, 2026 · by Fintool AI Agent

Repligen (NASDAQ: RGEN) delivered a strong finish to fiscal 2025, beating consensus estimates on both revenue and EPS while guiding for continued above-market growth in 2026. The bioprocessing equipment maker reported Q4 revenue of $198 million, up 18% year-over-year (14% organic), exceeding the $192 million consensus estimate by 3.0%. Adjusted EPS of $0.49 beat the $0.44 consensus by 10.4%.

The stock gapped down approximately 10% at the open but recovered throughout the session, closing down roughly 3% as investors digested what management characterized as a "prudent" 2026 outlook that balances near-term uncertainty around FDA policy and pharma responses to the MFN ruling with strong underlying momentum.

Did Repligen Beat Earnings?

Yes, Repligen delivered a clean double beat for Q4 2025:

The beat was driven by broad-based strength across the portfolio, with Proteins and Analytics both exceeding 30% growth and Chromatography above 25%. For the full year, Repligen delivered $738 million in revenue (+16% YoY) and $1.71 in adjusted EPS (+9% YoY), exceeding the high end of their initial guidance.

What Did Management Guide for 2026?

Repligen issued 2026 guidance that implies continued above-market growth, though with a wider range reflecting macro uncertainty:

Key guidance assumptions include:

- Foreign exchange roughly flat to H2 2025

- Tariff surcharges representing ~50bp gross margin headwind (full-year effect)

- Gene therapy platform creating ~2-point headwind to overall growth

- Normal seasonality with ~48% of revenue in the first half

- Q1 revenue expected down only low single digits sequentially from Q4

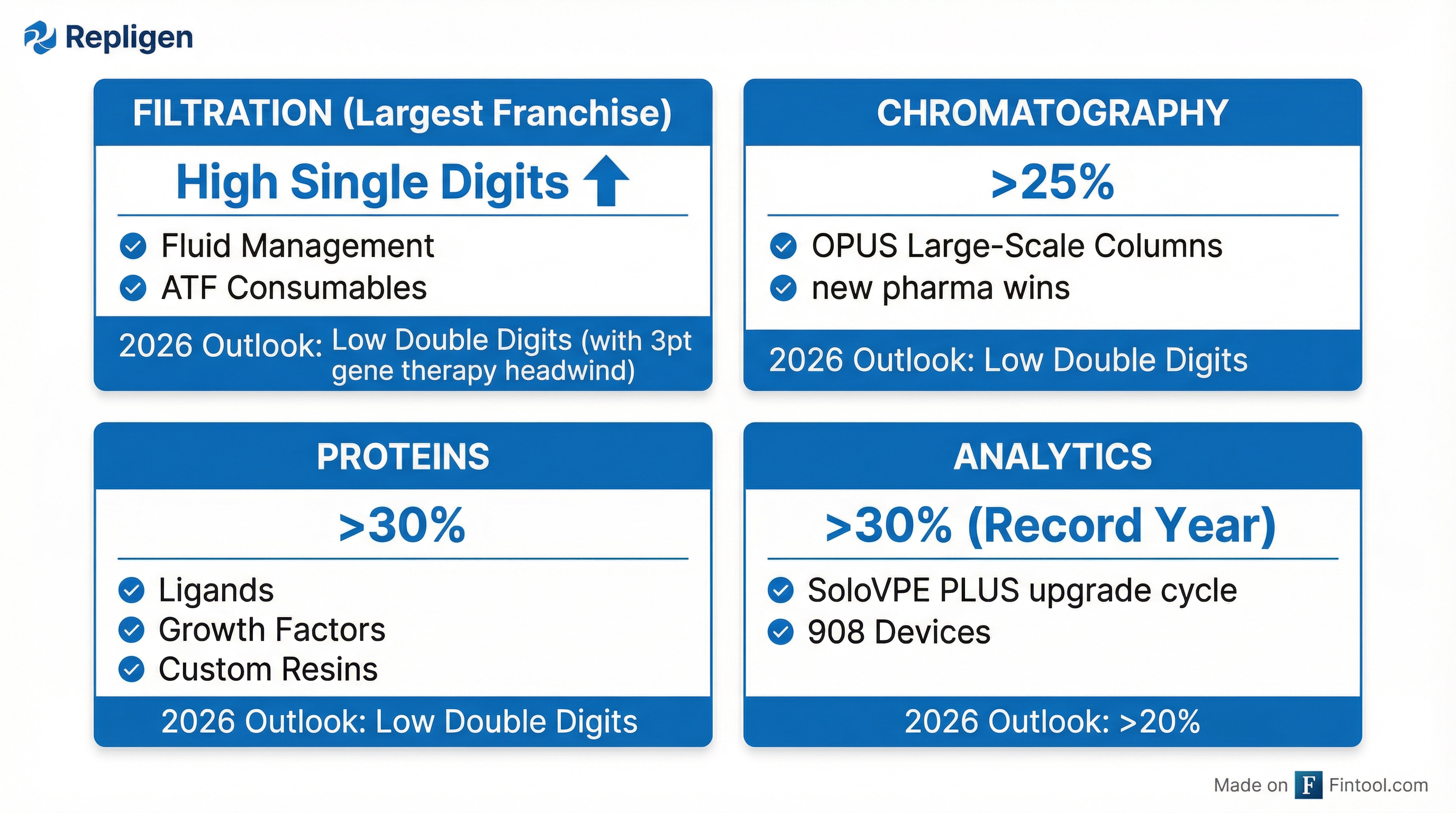

Franchise-level guidance (reported growth):

- Filtration: Low double digits (with 3-point gene therapy headwind)

- Chromatography: Low double digits

- Proteins: Low double digits

- Analytics: Greater than 20%

What Changed From Last Quarter?

Several notable developments emerged this quarter:

Strengthening Order Trends: Management highlighted that the strong order trend seen throughout 2025 continued in Q4, with the high-probability pipeline at its highest level ever. CEO Olivier Loeillot noted the funnel is "significantly higher than a year ago."

China Returning to Growth: China grew for the second consecutive quarter, albeit off a low base. Q4 orders were "very strong," and management expects China to return to significant growth in 2026.

CapEx Environment Still Muted: Capital equipment demand remained soft with full-year 2025 roughly flat versus 2024, though peers saw high-teens declines. Management expects CapEx to remain flat in 2026 outside of Analytics.

Emerging Biotech Recovery: Revenue from emerging biotech customers grew for the third consecutive quarter, though management cautioned it's "too soon to call this a trend" as activity remains below historical levels.

How Did Product Franchises Perform?

Proteins (>30% growth) was the standout performer for both Q4 and the full year, driven by broad-based strength across ligands, growth factors, and custom resins. The company launched three new AVIPure catalog resins for the new modality market in December and plans to launch 3-4 additional catalog resins in 2026.

Analytics (>30% growth) closed a record year with 37% full-year growth (21% excluding 908 Devices acquisition). The SoloVPE PLUS upgrade cycle is just beginning—less than 100 units upgraded out of a 1,500-2,000 unit installed base, representing a multi-year opportunity.

Chromatography (>25% growth) was driven by OPUS large-scale column wins at several new pharma customers. Management expects continued double-digit column growth in 2026.

Filtration (high single digits) grew modestly, with strength in fluid management and ATF consumables offset by muted downstream systems demand. Full-year growth was 8% (11% non-COVID).

What Are the Key Growth Catalysts?

Management highlighted several growth drivers for 2026 and beyond:

1. SoloVPE PLUS Upgrade Cycle: With less than 100 units upgraded out of 1,500-2,000 installed base, this represents a 2-3 year upgrade opportunity.

2. Proteins Portfolio Expansion: Continued launches of new catalog and custom resins, leveraging Avitide's Juloco bead technology to quickly develop customer-specific solutions.

3. ATF + MAVERICK Integration: The company is evaluating combining ATF systems with Raman technology (MAVERICK) acquired from 908 Devices. This could be a significant differentiator and growth driver.

4. Mid-IR Technology: A potential "game changer" for downstream UFDF and protein aggregation measurement, expected to launch late 2026 or early 2027.

5. China Expansion: Management is investing in local partnerships and commercial infrastructure, targeting above-company-average growth in China over the next three years.

6. Services Growth: Services represented ~6% of 2025 sales vs. ~10% industry benchmark. Analytics has >50% attachment rate, while larger equipment attachment rates are significantly lower—a clear opportunity.

What Are the Key Risks?

Management flagged several areas of uncertainty:

- FDA Policy Uncertainty: Limited biologic approvals so far in 2026 (only 5 new modalities approved in 2025 vs. 7 in 2024)

- MFN Response: Large pharma may delay CapEx decisions while digesting Q4 deals

- Gene Therapy Headwind: ~2-point headwind to overall growth, 3-point headwind to filtration

- Tariff Exposure: Full-year tariff surcharge impact (~50bp to gross margin), though management noted potential alternatives may be "a push or slightly better"

Key Management Quotes

On the business momentum:

"We have a very strong funnel of opportunity... the funnel with high probability, above 50%, is at the highest level ever and significantly higher than a year ago. We are very excited about it."

On the macro environment:

"There are a number of signs that macro backdrop is strengthening, including improved biotech funding, M&A activity, and more positive pharma sentiment. After a recovery year in 2025, the current environment is more balanced, though it remains early for some of these tailwinds."

On guidance philosophy:

"We believe our guidance is prudent, with the low end appropriately balancing some near-term uncertainty around FDA policy and biopharma's strategic response to MFN, while the high end assumes we're able to convert certain funnel opportunities in 2026."

How Did the Stock React?

The stock experienced significant intraday volatility following the earnings release:

The initial 10% gap down at the open likely reflected investor concerns about the wide guidance range and macro uncertainties flagged by management. However, the significant intraday recovery suggests the buy-side views the 9-13% organic growth target as achievable and sees the sell-off as overdone given the company's strong execution track record.

Forward Estimates

Current consensus for the next four quarters:

Values retrieved from S&P Global

FY 2026 consensus of $824M sits near the midpoint of management's $810-840M guidance range. The implied 15.5% FY 2027 revenue growth suggests analysts expect the bioprocessing recovery to continue gaining momentum.

Related Links: