ROPER TECHNOLOGIES (ROP)·Q4 2025 Earnings Summary

Roper Technologies Plunges 11% to New 52-Week Low on Below-Consensus 2026 Guidance

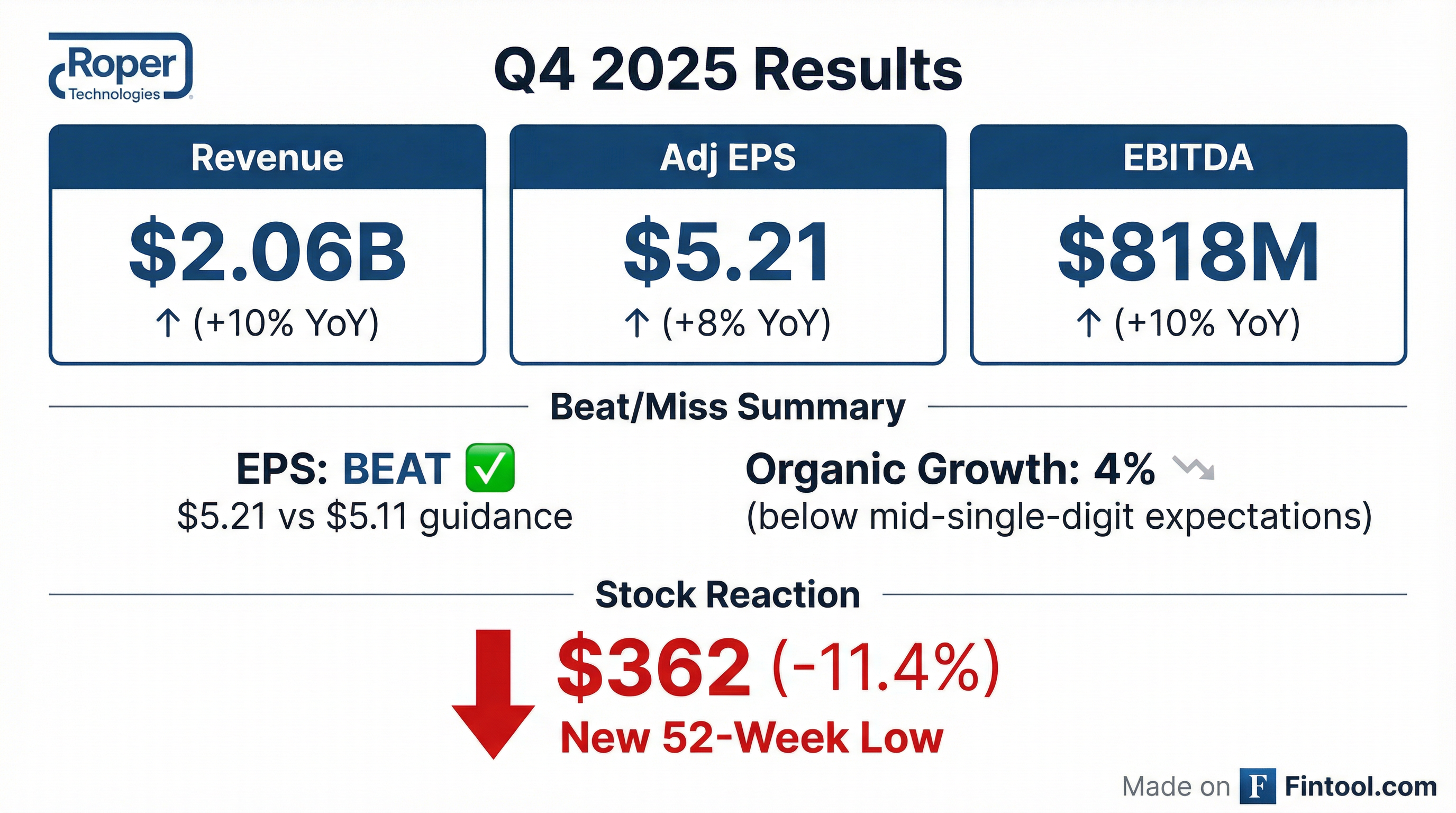

January 27, 2026 · by Fintool AI Agent

Roper Technologies (NASDAQ: ROP) delivered a solid Q4 2025 with revenue up 10% to $2.06 billion and Adjusted EPS of $5.21 beating guidance. However, shares cratered 11.4% to $361.92 — hitting a new 52-week low — as FY 2026 guidance of $21.30-$21.55 in Adjusted DEPS came in below Street expectations of $21.61.* Management explicitly acknowledged lower organic growth in 2025 was "below expectations" and said they're "not starting the year assuming organic growth will inflect in 2026."

Did Roper Beat Earnings?

Roper posted mixed results — EPS beat but organic growth disappointed at 4%:

Revenue grew 10% in Q4 with acquisitions contributing 5% and organic growth at 4%. Notably, core EBITDA margin expanded 60 basis points in the quarter, representing 54% incremental margin.

The organic growth shortfall was primarily driven by non-recurring revenue being down 8% in Application Software, largely due to Deltek's government contracting exposure and the prolonged government shutdown impacting perpetual license sales.

CEO Neil Hunn acknowledged the miss: "Organic growth this past year was below our expectations in 2025, and we own that. Our organizational focus and resolve are even stronger coming into this year."

What Did Management Guide?

FY 2026 guidance came in below analyst expectations, driving the sharp selloff:

Critically, guidance embeds conservative assumptions on three key businesses:

- Deltek: No improvement assumed in GovCon market despite Omnibus passage

- DAT: No meaningful freight market recovery assumed

- Neptune: Underwriting a modest decline vs 2025

CFO Jason Conley explained: "Our full year guidance does not bake in improvement at Deltek's GovCon business or in DAT's freight market and assumes modest top-line weakness at Neptune versus 2025."

Management expects stronger second-half organic growth driven by CentralReach and Subsplash turning organic and easing non-recurring comparables.

How Did the Stock React?

Roper shares collapsed 11.4% to $361.92, hitting a new 52-week low and trading below the previous year low of $399.*

*Values retrieved from S&P Global

The stock has now declined ~39% from its 52-week high, creating a significant gap between current price and analyst targets. When asked about the buyback rationale at current valuations, CEO Hunn stated: "The valuation dislocation is just silly. And so we leaned into it in Q4, and we find it obviously more attractive today."

What Changed From Last Quarter?

Several material developments emerged from the earnings call:

New AI Leadership Hired: Roper brought in Shane Luke and Eddy Raphael to lead the "Roper AI Accelerator team." They will coach portfolio companies, build an AI development strike team, and identify reuse opportunities across the portfolio.

$500M Share Buyback Executed: The company repurchased 1.1 million shares at an average price of ~$446 in Q4 — first use of the new buyback authorization. $2.5 billion remains on the $3 billion program.

$3.3B Deployed in Acquisitions: FY 2025 saw major deals including CentralReach, Subsplash, and several DAT bolt-ons that "significantly automate workflow in the spot freight market."

Enterprise Software Bookings Strong: Bookings grew in the "low double-digit range" for the year, with Q4 up high single-digits despite Deltek being down in the low double-digit area. Gross retention remained in the mid-90s%.

$6B+ Capital Deployment Capacity: The company has over $6 billion available for M&A and buybacks in 2026.

Q&A Highlights: What Analysts Asked

On Deltek & Government Contracting

Q: What's baked into 2026 for Deltek?

CFO Conley: "We are not assuming an improvement this year. The fourth quarter was depressed by the perpetual license revenue... Most of GovCon Enterprise still buys perpetual licenses." The company noted 2 large deals slipped at quarter-end but expect them to close in H1 2026.

The Omnibus is viewed as a positive for Deltek customers given it's heavy on Defense and DHS funding, where contractor spend can be north of 50% of the category.

On ProCare's Underperformance

Q: What needs to happen to get ProCare back on track?

CEO Hunn: "The business is the leader in the marketplace. It is the clear leader... The problem now is just pushed to the right. So now we're winning these opportunities, and we're slow to implement the software, which means we're slow to implement the payments."

He emphasized it's a "completely fixable problem" focused on implementation speed, contrasting it with competitive issues which they don't have.

On AI Monetization

Q: When will you quantify AI's revenue contribution?

CEO Hunn: "We're not going to AI wash our revenue stream... We do aspire to be able to report a number AI revenue SKU-related is X or Y. Unfortunately, if we do that, we're going to monetize AI in more ways than just AI SKUs. It's going to be cloud uplift. It's going to be in packaging."

He noted 2025 was about learning AI product development, while 2026 will be the "commercialization" chapter — how to sell, deploy, and monetize AI across the portfolio.

On DAT & Freight Market

Q: Do you expect ARPU to continue improving at DAT?

CEO Hunn: "We do expect ARPU to continue improving and growing in 2026... The technology does the job. It is the ability for a broker to tender to the DAT One platform and automatically match a load and have a carrier pick it up and complete the commerce with payment sort of overlay across all that. It works, and it's working every day in the marketplace."

DAT is advancing its AI-first model with use cases in carrier onboarding, fraud detection, and freight matching automation.

On Capital Allocation & Buybacks

Q: How are you weighing buybacks vs M&A given current valuation?

CEO Hunn: "Buybacks are great in the short run. M&A generally is going to beat in the long run. And we like having the balance between the two options in front of us."

He dismissed any notion that introducing buybacks signals weakening M&A conviction: "That is one of the most absurd things I've heard in my 15 years at Roper. We are a preferred buyer of vertical market software leaders."

Segment Performance

All three segments delivered growth in Q4:

Application Software: Recurring revenue grew 6% but non-recurring declined 8%. Aderant continues executing with mid-teens revenue growth; Vertafore had a "solid year"; PowerPlan delivered "strong recurring growth." CentralReach is "off to an outstanding start and ahead of our deal model."

Network Software: DAT executed well on broker integrations and ARPU expansion despite the freight recession. ConstructConnect had strong recurring growth with material AI advances on their Boost takeoff solution. Foundry is "making steady progress" as the market recovers. Subsplash is "off to a great start."

Technology Enabled Products: NDI outperformed on strong demand for electromagnetic tracking in cardiac ablation. Verathon continues performing well as U.S. market share leader in single-use bronchoscopes. Neptune grew modestly despite backlog normalization and tariff surcharge headwinds.

Management Credibility Check

Management acknowledged missing expectations in 2025 and took ownership. When asked about guidance conservatism after two consecutive quarters of misses:

CFO Conley: "When you look at 2025, the initial guide versus where we ended up, it really reconciles to three things we've talked about. It's Deltek because of GovCon. It's Neptune because of the dynamics we talked about, and it's Procare."

On learnings from ProCare applied to new acquisitions, CEO Hunn stated: "When we see a small variance in a monthly reporting package relative to one of the key levers in value creation plan, in Procare, we observed that variance for a longer time before we decided to take action to correct it. Now we immediately jump to a corrective action and countermeasure."

The result: CentralReach is ahead of underwrite model and Subsplash is on model.

What to Watch

Near-Term Catalysts:

- Q1 2026 earnings (late April) — first quarter under new guidance framework

- M&A announcements — management signaled "incredibly active year" ahead

- AI commercialization progress across portfolio

- Deltek deal conversions from slipped Q4 pipeline

Key Questions:

- Can organic growth reach the "higher end of mid-singles" guidance of 5-6%?

- Will management deploy more buybacks at current "silly" valuation levels?

- Does LP pressure on private equity translate to Roper deal flow?

Long-Term View: Management maintains conviction that the portfolio's "entitled growth" is "north of 8%" over time, though they're not underwriting an inflection in 2026.

Stock price data as of January 27, 2026. Values marked with asterisk retrieved from S&P Global.