BOSTON BEER CO (SAM)·Q4 2025 Earnings Summary

Boston Beer Q4 2025: EPS Beats by 15% as Gross Margins Surge, But Volume Declines Persist

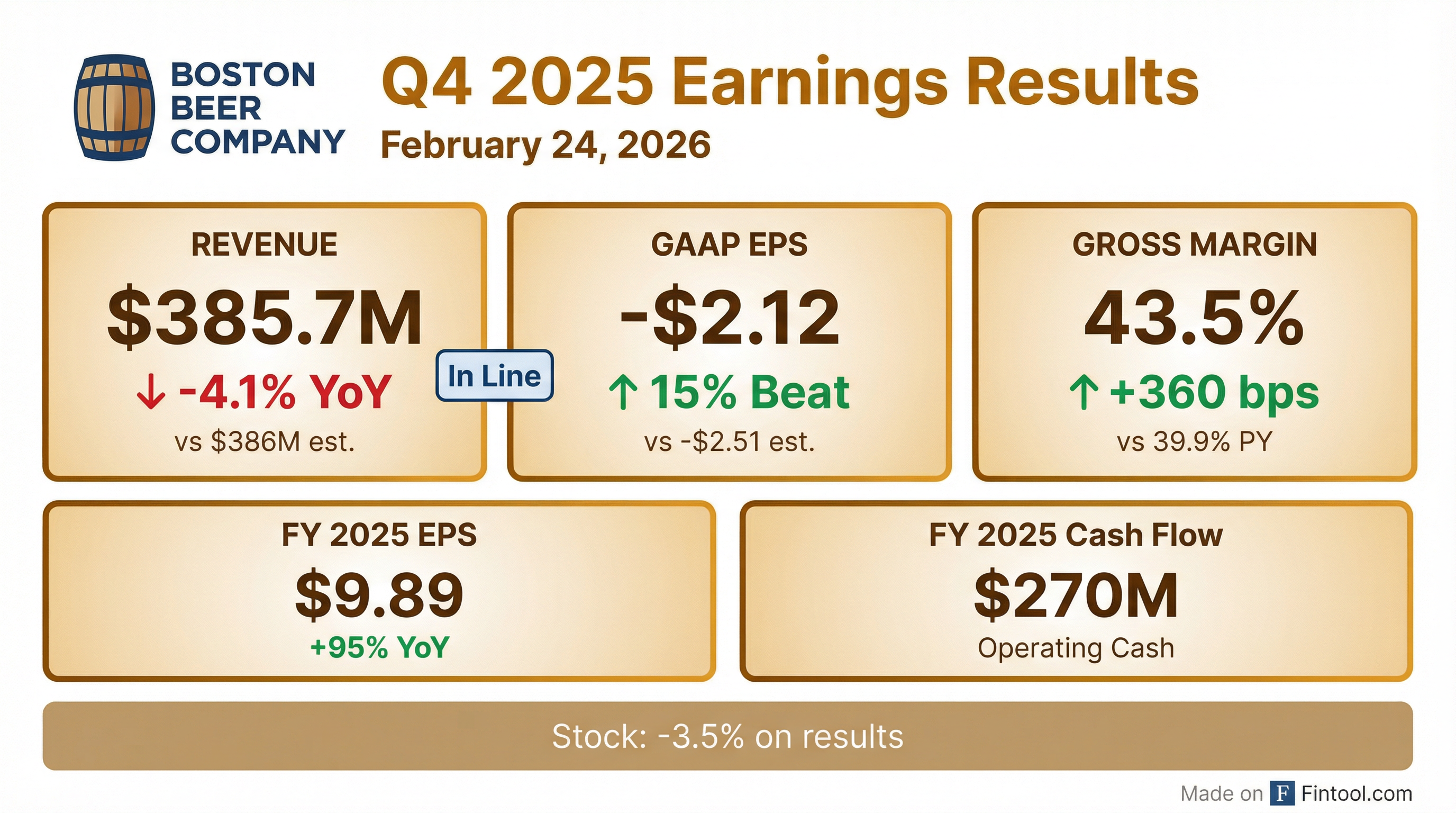

February 24, 2026 · by Fintool AI Agent

Boston Beer Company (NYSE: SAM) reported Q4 2025 results that beat earnings expectations despite persistent volume headwinds. The craft brewer delivered GAAP EPS of -$2.12, beating the consensus estimate of -$2.51 by 15.3%, while revenue of $385.7 million came in essentially in-line with expectations . The story of the quarter was gross margin expansion—up 360 basis points year-over-year to 43.5%—driven by procurement savings, brewery efficiencies, and favorable product mix .

For full year 2025, Boston Beer reported EPS of $9.89, a remarkable 95% increase from the prior year, though this was inflated by comparison against $68.6 million in one-time charges (brand impairment and contract settlement) in 2024 . Excluding those items, adjusted net income declined 2.5%.

Did Boston Beer Beat Earnings?

Yes—on EPS, significantly. Revenue was in-line.

The Q4 EPS beat was driven entirely by gross margin outperformance. Revenue declined 4.1% year-over-year as depletions fell 6% and shipments dropped 7.5% . However, the margin story more than offset volume weakness—gross margin of 43.5% was 360 bps better than Q4 2024's 39.9% .

Key margin drivers:

- Improved brewery efficiencies

- Procurement savings

- Price increases and favorable product mix

- Lower inventory obsolescence

Partially offsetting: $3.6 million negative tariff impact and shortfall fees of $13.9 million .

What Changed From Last Quarter?

Q4 is seasonally the weakest quarter, but the margin trajectory continued improving:

The Q4 gross margin of 43.5% was the lowest of 2025 due to seasonality and $13.9M in shortfall fees, which typically hit hardest in Q4 . However, it still represented meaningful improvement over Q4 2024's 39.9% .

Volume declines accelerated in Q4, with Twisted Tea, Truly Hard Seltzer, and Samuel Adams brands all declining, only partially offset by growth in Sun Cruiser, Angry Orchard, and Dogfish Head .

How Did the Full Year Stack Up?

FY 2025 was a tale of margin expansion offsetting volume declines:

Important context: FY 2024 included a $42.6M Dogfish Head brand impairment and $26M contract settlement charge . Excluding these, FY 2025 net income declined $2.8M or 2.5%.

What Did Management Guide?

2026 guidance implies continued margin progress but no volume inflection:

Timing note: First half 2026 shipments expected to decline toward the lower end of guidance due to tough comps—the company shipped ahead of depletions in H1 2025 to support innovation and build wholesaler inventories .

Tariff caveat: Guidance is based on tariffs in place prior to the February 20, 2026 Supreme Court ruling .

What Did Management Say?

Jim Koch, Chairman, Founder & CEO:

"We were pleased to deliver on our financial commitments in 2025 while maintaining market share in a challenging operating environment. Looking ahead, we are highly focused on operational excellence, including investing in our portfolio of iconic brands, developing a strong innovation pipeline and continuing to execute on our multi-year productivity initiatives. We believe this disciplined focus positions us to improve performance over time and create long-term value for shareholders."

Diego Reynoso, CFO:

"2025 was a year of continued progress for Boston Beer, highlighted by meaningful gross margin improvement and strong cash generation, while significantly increasing advertising support behind our brands. In 2026, we expect continued progress on our multi-year supply chain initiatives which will be reinvested to support our brands."

Tone: Management struck a cautiously optimistic tone, emphasizing operational discipline and brand investment while acknowledging the "challenging operating environment." The focus on "maintaining market share" rather than growing it signals acceptance of category headwinds.

Brand Performance Deep Dive

Declining brands (majority of portfolio):

- Twisted Tea — declining depletions

- Truly Hard Seltzer — declining depletions

- Samuel Adams — declining depletions

Growing brands (partially offsetting):

- Sun Cruiser — growth

- Angry Orchard — growth

- Dogfish Head — growth

Early 2026 signal: Year-to-date depletions through the 8 weeks ended February 21, 2026 are estimated to have decreased approximately 3%, an improvement from the 6% decline in Q4 2025 .

Capital Allocation Update

Balance sheet remains fortress-like:

Management continues prioritizing buybacks, having repurchased $212.9M combined in FY25 and early 2026, reducing shares outstanding meaningfully and supporting EPS growth.

How Did the Stock React?

Down 3.5% following results, despite the EPS beat.

Why down on a beat? The market appeared to focus on:

- Continued volume declines (-6% Q4 depletions)

- Conservative 2026 guidance (flat to down mid-singles)

- Rising tariff headwinds ($20-30M expected vs $10M in 2025)

Valuation context: At $227, SAM trades at 39% below its 52-week high of $371.65, reflecting the sustained skepticism around the company's ability to reignite topline growth.

Key Risks to Watch

- Tariff escalation — Guidance assumes $20-30M impact, but Supreme Court ruling introduces uncertainty

- Continued hard seltzer decline — Truly remains in secular decline with no stabilization in sight

- Shortfall fees — $21.4M in FY25; expected to be 40-60 bps headwind in FY26

- Innovation execution — Must offset declining core brands with Sun Cruiser and new products

The Bottom Line

Boston Beer delivered a solid Q4 beat on operational execution, proving the margin story is real. Gross margin expanded 360 bps YoY despite the seasonally weak quarter, and full-year gross margin of 48.5% was up 410 bps. The balance sheet is pristine with $223M cash and zero debt.

However, the volume picture remains challenging. Depletions declined 6% in Q4 and 4% for the full year, with flagship brands Twisted Tea and Truly both contracting. Growth brands like Sun Cruiser and Dogfish Head are not yet large enough to offset the declines.

Management's 2026 guidance—flat to down mid-single digit volumes with 48-50% gross margin—implies more of the same: margin gains reinvested in brand support rather than falling to the bottom line, with no topline inflection expected.

For bulls: The margin transformation is working, buybacks are reducing shares, and the balance sheet provides optionality. Early FY26 depletion trends (-3%) show improvement.

For bears: This is a shrinking revenue company in a competitive category, trading at a premium to peers despite declining volumes. The hard seltzer implosion may not be over.

Analysis based on Boston Beer's Q4 2025 8-K filing dated February 24, 2026.