SIMILARWEB (SMWB)·Q4 2025 Earnings Summary

Similarweb Beats Estimates but Guides Lower as AI Deals Slip — Stock Crashes 19%

February 17, 2026 · by Fintool AI Agent

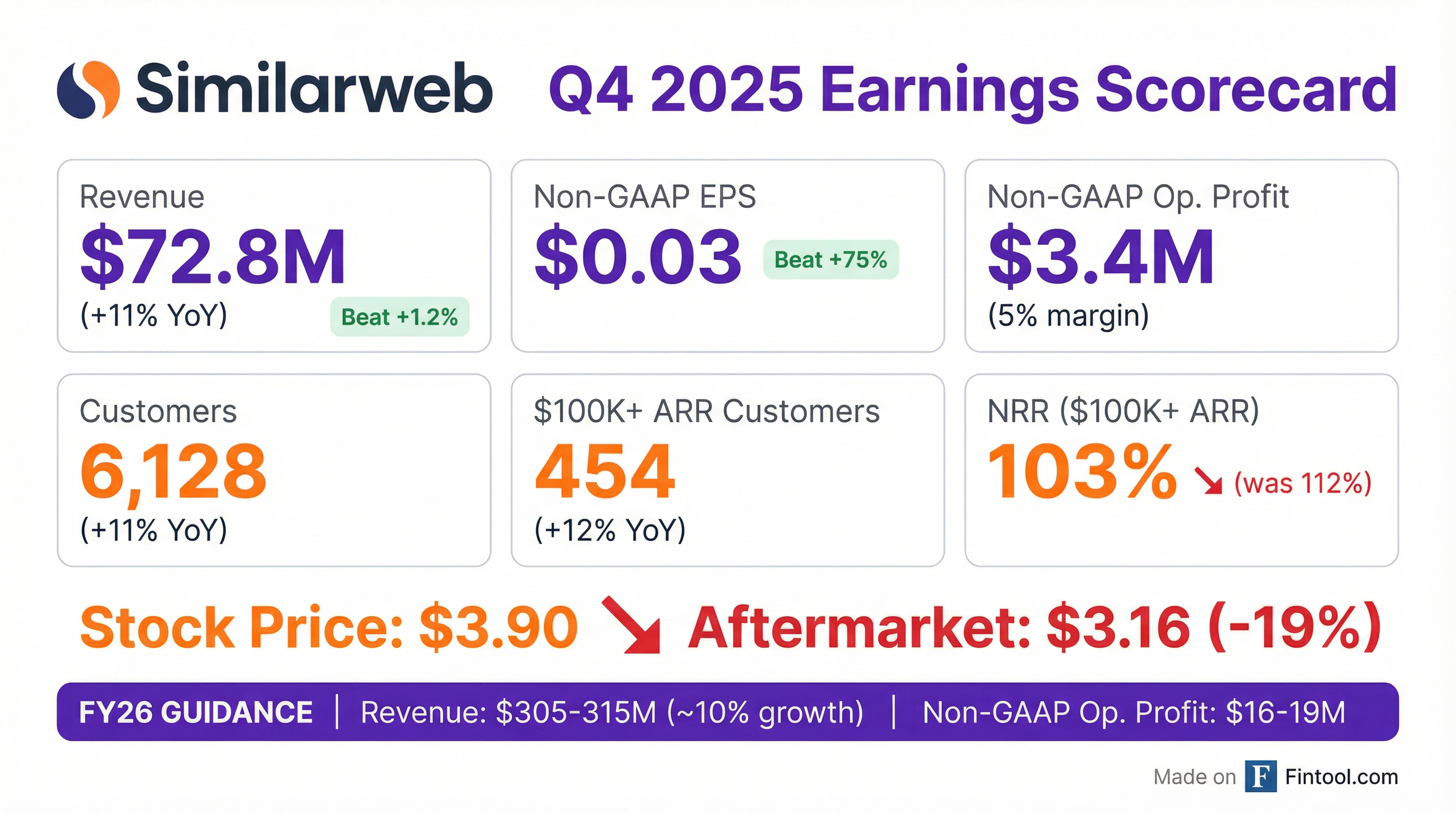

Similarweb (NYSE: SMWB) delivered a mixed Q4 2025, beating both revenue and EPS estimates but sending shares down 19% in after-hours trading as FY2026 guidance came in below expectations. The digital data platform reported revenue of $72.8M (+11% YoY) and non-GAAP EPS of $0.03, both topping consensus. However, management acknowledged that "revenue growth in the fourth quarter was slower than expected" due to two large LLM data training contracts that failed to close.

Did Similarweb Beat Earnings?

Yes — SMWB beat on both the top and bottom line, though the margin was narrower than recent quarters.

*Values retrieved from S&P Global

The company maintained its track record of profitability with its ninth consecutive quarter of positive free cash flow ($1.0M normalized FCF). Full-year 2025 revenue reached $282.6M (+13% YoY), with non-GAAP operating profit of $9.1M (3% margin).

Beat/Miss History (Last 8 Quarters)

*Values retrieved from S&P Global

What Happened to the AI Deals?

CEO Or Offer attributed the growth shortfall to two large LLM data training contracts that failed to close in Q4 but remain active in the pipeline. This is significant because Similarweb has been positioning itself as a critical data provider for training large language models.

Key AI metrics from Q4:

- GenAI revenue reached 11% of total revenue, up from 8% at the beginning of the year

- GenAI Intelligence product (launched Q3 2025) has ~200 customers and ~$3M ARR

- New Manus partnership validates Similarweb's role in powering agentic AI tools

- AI Studio launched — new conversational AI interface for accessing digital data

"The AI revolution fundamentally favors companies with proprietary, high-quality, and real-time data... While the scale of new larger, multi-year opportunities has resulted in longer sales cycles and revenue growth did not yet accelerate in the fourth quarter as we expected, the demand we see in the pipeline and the steps we have taken to upskill and specialize our sales force reinforce our confidence in our strategy." — Or Offer, CEO

What Did Management Guide?

Guidance was the clear disappointment, implying a deceleration from FY25's 13% growth to just 10% in FY26.

The guidance notably does not include the two large LLM deals that management highlighted as pipeline opportunities, creating a potentially conservative baseline.

How Did the Stock React?

SMWB cratered in after-hours trading:

The stock is now trading near its 52-week low of $3.66, down ~64% from its 52-week high. The sharp after-hours decline reflects investor disappointment with:

- Guidance deceleration from 13% to 10% growth

- Slipped AI deals that were expected to close in Q4

- NRR deterioration from 112% to 103% for $100K+ customers

What Changed From Last Quarter?

Positive Changes

- Multi-year subscriptions hit 60% of ARR, up from 49% a year ago and 58% last quarter — indicating stronger customer commitment

- RPO grew 17% YoY to $288.8M with 69% expected to convert in 12 months

- $100K+ customers grew 12% YoY to 454 accounts, representing 63% of ARR

- Gross margin improved to 81% from 78% in Q4 2024

Negative Changes

- NRR deteriorated sharply — 103% for $100K+ customers vs 112% a year ago

- Total customer NRR fell to 98% from 101%

- Growth decelerated — Q4 was 11% vs 13% for FY25 overall

- Average account value declined slightly to $370K from $376K YoY (but up from $366K sequentially)

Quarterly Revenue Trend

Key Operating Metrics

What Management Avoided Discussing

Management was notably optimistic about AI opportunities but provided little clarity on:

- When the large LLM deals might close — described only as "active in our pipeline" with varying timing

- Specific NRR improvement timeline — only said they expect improvement "during 2026"

- Competitive pressure from AI-native companies potentially building their own data capabilities

- Margin guidance for FY26 beyond operating profit range

New CFO Perspective

New CFO Ran Vered (who joined recently) offered a measured view:

"I joined Similarweb because of the irreplaceable value of our data and the massive opportunity to enhance and leverage this asset as a critical necessity for companies to win their markets in the generative era... Our outlook for another year of growth in 2026 is prudently grounded in high-visibility core business drivers, while gaining momentum for large strategic AI deals."

Forward Catalysts & Risks

Potential Catalysts

- Large LLM contract closings — two deals still in pipeline could meaningfully accelerate growth

- AI Studio adoption — could drive higher utilization and expansion within existing accounts

- Bloomberg partnership expansion — Similarweb data now in {ALTD <GO>} for alternative data

- NRR stabilization — GRR has remained stable, suggesting churn is contained

Key Risks

- Continued NRR deterioration if enterprise expansion stalls

- AI deal timing uncertainty — long sales cycles could push revenue into 2027

- Macro headwinds — management cited "broader market weakness as companies reallocate current budgets toward AI transition"

- Competition from AI-native platforms building proprietary data capabilities

The Bottom Line

Similarweb delivered a beat on both revenue and EPS, but the market is clearly focused on the forward outlook. With FY26 guidance implying just 10% growth (down from 13%) and two high-profile AI deals failing to close, investors punished the stock with a 19% after-hours decline. The bull case hinges on those LLM contracts eventually closing and AI becoming a meaningful growth driver. The bear case is that the core digital intelligence business is mature and AI deals may prove elusive. At $3.16 aftermarket (~$275M market cap), the stock trades at less than 1x forward revenue — but execution on AI monetization remains the swing factor.