SYSCO (SYY)·Q2 2026 Earnings Summary

Sysco Beats on EPS, Raises Full-Year Guidance as Local Volume Turns Positive

January 27, 2026 · by Fintool AI Agent

Sysco Corporation (NYSE: SYY) reported Q2 FY2026 results that exceeded adjusted EPS expectations while raising full-year guidance. The foodservice distribution giant delivered adjusted EPS of $0.99 (up 6.5% YoY), beating consensus by $0.02, as local case volume growth turned positive for the first time in several quarters.

Shares surged 9.8% to $83.01, marking the stock's best single-day performance in over a year and pushing it near 52-week highs. The strong reaction reflects enthusiasm for the volume inflection, AI-driven productivity gains, and continued January momentum.

Did Sysco Beat Earnings?

Sysco delivered mixed results on the top line but outperformed on profitability:

Gross margin expanded 15 basis points to 18.3%, driven by effective product cost management and strategic sourcing efficiencies despite 2.9% product cost inflation, primarily in meat and seafood categories.

The gap between GAAP and adjusted results reflects $57M in restructuring and transformation costs, plus $58M in acquisition-related costs including intangible amortization.

What Did Management Guide?

Management raised full-year guidance, signaling confidence in the company's momentum:

CFO Kenny Cheung noted this guidance includes an $100 million ($0.16 per share) headwind from lapping lower incentive compensation in FY2025. Excluding this impact, adjusted EPS growth would be at the high end of the company's 5%-7% long-term algorithm.

Q3 Specifics: Management is comfortable with the current consensus estimate of $0.94 for Q3. The incentive compensation impact is $63M in Q3 and $11M in Q4.

How Did the Stock React?

Shares surged 9.8% following the earnings release, the stock's best single-day performance in over a year. The strong reaction reflects investor enthusiasm for the guidance raise, the inflection in local case volume growth, and continued momentum in January—a key metric Wall Street has been watching closely.

What Changed From Last Quarter?

The most significant development is the turnaround in U.S. local case volume:

CEO Kevin Hourican called out this inflection: "We delivered our third consecutive quarter of sequentially improving local case growth. More importantly, USFS local case volume is now positive, having delivered positive 1.2% case volume growth in the quarter."

This improvement came despite industry traffic (per Black Box) declining 200+ basis points year-over-year and sequentially. CFO Cheung noted: "We are encouraged by the meaningful acceleration in our local volume performance, even as the industry decelerated throughout the quarter." International local case growth was even stronger at +4.5%, marking the 9th consecutive quarter of double-digit operating income growth for that segment.

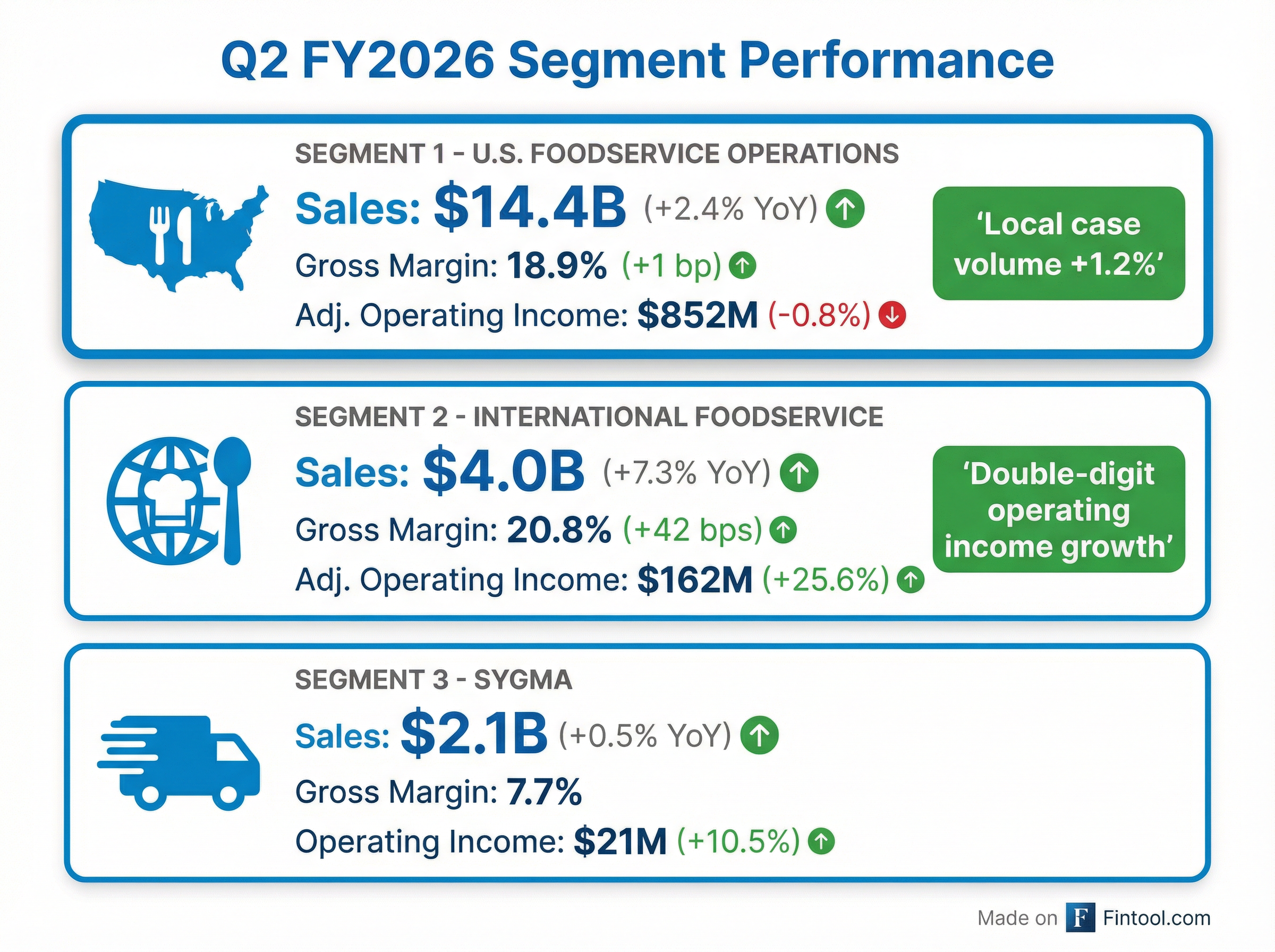

Segment Performance

U.S. Foodservice Operations (69% of sales)

The slight decline in adjusted operating income reflects planned investments in sales headcount and capacity, which management views as positioning the company for accelerating growth.

International Foodservice (19% of sales)

International was the standout segment, delivering double-digit operating income growth through strong local volume gains and disciplined margin management. On a constant currency basis, sales grew 3.6%.

SYGMA (10% of sales)

Key Growth Initiatives: AI 360 and Perks 2.0

Management highlighted several company-specific initiatives driving the local volume turnaround:

AI 360 CRM Tool — Now 4 months live in production with impressive adoption:

- 95%+ of sales colleagues using the tool weekly

- Clear correlation: "Those that are using the tool more often are outperforming those that use it less often. The math is very clear: If you use the tool, you sell more."

- New "Swap and Save" feature coming that provides one-click product substitution suggestions that save customers money while improving Sysco margins

Sysco Your Way & Perks 2.0 — Loyalty programs delivering results:

- Sysco Your Way neighborhoods continue mid-single-digit volume growth despite being in their 4th year

- Perks 2.0 revamp driving improved customer retention and increased share of wallet

Ginsberg's Foods Acquisition — Tuck-in acquisition completed at end of Q2:

- Premier broadline distributor in the Northeast

- Expected to contribute ~50 bps to local case growth in H2

- Management sees opportunity to unlock additional growth by introducing Sysco's buying programs

Capital Allocation & Balance Sheet

Management continues to prioritize returning capital to shareholders through dividends while maintaining investment-grade leverage.

Key Management Commentary

CEO Kevin Hourican on momentum:

"It is an exciting time to be at Sysco... Our building momentum and progress with key growth initiatives gives us confidence that we will deliver at least 2.5% local case growth in the 2nd half of the fiscal year."

CFO Kenny Cheung on quality of earnings:

"Second quarter results reflected high-quality performance across the income statement and cash flow. These results highlight our operational execution on Sysco specific initiatives."

Q&A Highlights

On monthly momentum through Q2: CEO Hourican: "The performance of Sysco, relative to the industry, strengthened each month of Q2... We've seen that strength continue into January." Despite industry foot traffic declining from -2% in October to -3%+ in December, Sysco's outperformance widened each month, with December being the strongest.

On January trends: "January is off to a strong start on the controllables... Foot traffic to restaurants improved in January versus Q2, quite notably." Management noted weather favorability in January may give back some gains due to this week's winter storms across the U.S.

On customer retention improving: CFO Cheung: "We had the highest growth of new [customers] and the lowest level of loss in the past 12 months." The new-versus-loss ratio expanded solidly in Q2, driven by improved sales colleague retention translating to improved customer retention.

On Sysco Brand penetration: Sysco Brand (over $20B in sales) remains down year-over-year but saw nominal improvement Q1 to Q2. CEO Hourican expects positive penetration year-over-year by the end of H2, driven by: (1) expanding value tier assortment, (2) improved price architecture using AI tools, and (3) renewed sales force focus on "swap and save" conversions.

On automation and AI investments: Sysco is evaluating warehouse automation solutions for future new facilities and expansions, with presentations from "top engineering firms from around the world" occurring this week. The company is also deploying agentic AI tools across all functions—HR, merchandising, finance—to drive productivity.

What to Watch Going Forward

-

Local Case Volume Trajectory: Management's 2.5% H2 target implies 100 bps organic acceleration plus 50 bps from Ginsberg's. Two-year stack expected to improve in H2, with Q4 stronger than Q3 despite tougher compares.

-

Q3 Expectations: Management is "comfortable with" Q3 consensus EPS of $0.94, which includes a $63M incentive compensation lap headwind (Q4 lap is only $11M).

-

Restaurant Traffic Trends: Sysco is outperforming despite industry foot traffic declining. Management sees potential tailwinds from: improved consumer confidence vs. last year, higher tax refund checks, and restaurants leaning into value offerings.

-

Sysco Brand Inflection: Currently down year-over-year but expected to turn positive by end of H2. Key lever for margin expansion given ~50% penetration with local customers.

-

COO Transition: Greg Bertrand (35-year Sysco veteran) retiring, will serve as strategic advisor part-time through next year. Management highlighted strong depth of field leadership.