INTERFACE (TILE)·Q4 2025 Earnings Summary

Interface Delivers Record FY25, EPS Beats by 21% Despite Slight Revenue Miss

February 24, 2026 · by Fintool AI Agent

Interface, Inc. (NASDAQ: TILE), the global flooring and sustainability leader, reported Q4 2025 results this morning with a mixed bag: adjusted EPS crushed expectations by 21%, but revenue came in fractionally light. The stock fell ~3% in early trading despite the company delivering record full-year 2025 results and unveiling noravant—a groundbreaking rubber flooring platform management expects to generate $50-100M over 5 years.

Did Interface Beat Earnings?

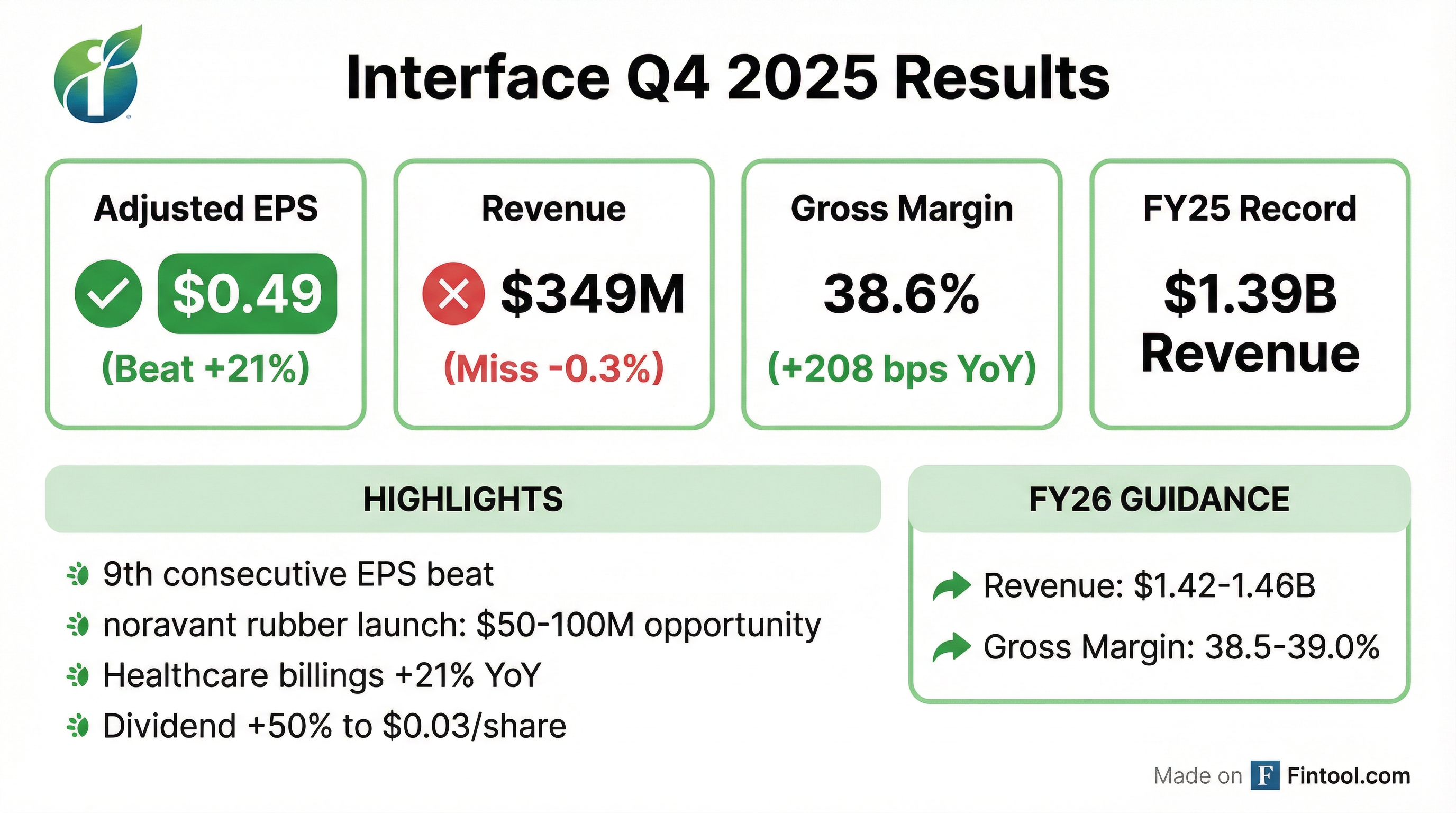

Adjusted EPS: Beat by 21.5%

- Actual: $0.49

- Consensus: $0.40

- GAAP EPS: $0.41

Revenue: Miss by 0.3%

- Actual: $349.4 million

- Consensus: $350.5 million

- YoY Growth: +4.3% reported, +1.6% currency-neutral

The EPS beat was driven by margin expansion (+208 bps YoY gross margin improvement) and operational discipline, offsetting the slight revenue miss.

How Did the Stock React?

TILE shares opened at $32.47 and fell to $31.50 (-3.3%) despite the EPS beat. The market appears to be reacting to:

- Slight revenue miss despite strong profitability

- Currency headwinds - currency-neutral growth was only +1.6% vs +4.3% reported

- Elevated expectations - stock up 83% from 52-week low of $17.24 to recent highs of $35.11

The aftermarket quote shows some recovery to $32.10 as investors digest the full picture.

What Made FY 2025 a Record Year?

Interface delivered record results across key metrics in FY 2025:

Key drivers of the record year:

- Currency-neutral sales up 4.3% with growth across all regions, product categories, and key market segments

- Healthcare and Education verticals particularly strong with global billings up 21% and 8% respectively

- Continued share gains in Corporate Office segment

- Adjusted gross profit margin expanded to 39.0%, reflecting favorable pricing, mix, and manufacturing efficiencies

What Did Management Guide?

Interface provided FY 2026 guidance with cautious optimism, noting solid orders and healthy backlog while acknowledging macro uncertainty:

Q1 FY 2026 Guidance:

Full Year FY 2026 Guidance:

Note: FY 2026 includes 53 weeks with an extra week in Q1.

The midpoint of FY 2026 revenue guidance ($1.44B) compares to current consensus of $1.45B, suggesting guidance is roughly in-line with expectations.

What is Noravant and Why Does It Matter?

The most exciting announcement from the call was the launch of noravant—a groundbreaking rubber flooring platform that management believes could generate $50-100 million over the next 5 years.

Key Details:

- First-of-its-kind: Industry's first wood grain design in rubber flooring

- PVC-free: Combines high performance, design flexibility, and sustainability

- Target market: Healthcare patient rooms, classrooms, corridors, waiting areas

- Revenue timing: Expected to begin contributing in Q4 2026, building over time due to nora's longer selling cycle

- 2026 revenue expectation: $5-10 million

CEO Laurel Hurd explained the strategic rationale:

"We've developed a completely new rubber offering that will compete at the premium end of the vinyl sheet category. This is an incremental growth opportunity that will meaningfully expand our addressable market in resilient over time."

"We launched with a wood grain look to support strong demand from healthcare customers for patient rooms to look more like luxury hotel rooms."

The launch comes as Interface has already demonstrated strong momentum in nora rubber, with global rubber billings up 17% in 2025.

What Changed from Last Quarter?

Balance Sheet Strengthened Dramatically:

- Total debt reduced 40% YoY to $181.6M

- Net debt/EBITDA improved to 0.5x from prior levels

- Repaid $128M of debt in Q4 alone

- Extended remaining debt maturities to 2030

Capital Returns Initiated:

- Repurchased $13M of common stock in Q4 ($18M for full year)

- Increased quarterly dividend from $0.02 to $0.03 per share (+50%), "reflecting confidence in our cash flow generation and our earnings durability"

Segment Performance:

The EAAA segment showed particular strength with adjusted operating income up 198% YoY ($10.1M vs $3.4M), while AMS operating income declined slightly.

What Did Management Say?

CEO Laurel Hurd emphasized the One Interface strategy driving results:

"2025 was a record year for Interface, as net sales, Adjusted Operating Income, and Adjusted EBITDA reached their highest levels in the company's history, driven by a One Interface strategy."

"We're just getting started. We enter 2026 with confidence in our strategy and our ability to create long-term value for our shareholders."

On the combined selling team success:

"Our combined U.S. selling team model is a key enabler, allowing us to harness the full strength of our sales organization and present a single, cohesive Interface to our customers across carpet tile, LVT, and nora Rubber."

CFO Bruce Hausmann on strategy execution:

"Often you see companies state a strategy, and you wonder, where is that showing up on the P&L? I think we're the dead opposite of that. Our strategy is actually revealing itself on the P&L, which is fantastic to see."

On customer diversification:

"One thing that helps us is that our customer concentration is so low. We're not dependent on any one or two or three or four customers. We have a big, diverse group of customers, which I think is actually a strength."

Revenue by Geography and Vertical

Geographic Mix (FY 2025):

- Americas: 61%

- EMEA: 29%

- APAC: 10%

Customer Vertical Mix (FY 2025):

- Corporate/Office: 44%

- Education: 20%

- Healthcare: 11%

- Other: 25%

Q&A Highlights: What Did Analysts Ask?

On Gross Margin Puts and Takes (Brian Biros, TRG): CFO Hausmann explained that achieving the high end of 38.5-39% gross margin guidance would represent ~100 bps improvement: "We're offsetting about 50 basis points of tariff-related headwinds, and then we're offsetting about 50 basis points due to the inventory adjustment."

On Tariff Impact (Alex Paris, Barrington Research): Tariffs diluted gross margin by ~20 bps in 2025, expected to be ~50 bps YoY impact in 2026. Management confirmed they are "covering dollar for dollar" but it has a dilutive effect on GP%. Regarding recent Supreme Court decision on tariffs: "We were at 15% tariffs last week. The Supreme Court struck that down... On Saturday, we were back to 15%, kinda right back where we started."

On Regional Performance (Reuben Garner, Benchmark): CEO Hurd noted: "We've really seen New York and the Bay Area come back strong. They were obviously harder hit in COVID. It took a longer time to recover, but we're seeing those really strengthen. Texas remains strong. The Southeast remains strong."

On Healthcare/Education Runway (Reuben Garner, Benchmark): CEO Hurd: "Healthcare, great macros with the aging population, more focus on preventative care, a lot of technology happening in healthcare... This is the place that has been most strongly impacted by our combined selling team, where we have our sales force focused on each market."

On SG&A Discipline (David MacGregor, Longbow Research): CEO Hurd: "We know where every dollar is and are very, very disciplined in what and how we spend it. We're focused on making sure that we drive the front end of the business—the selling, the sales and innovation get the investment—while we do everything possible to be efficient on the back end."

Q4 2025 Billings by Segment:

Historical EPS Beat/Miss Trend

Interface has beaten EPS estimates for 9 consecutive quarters:

*Values retrieved from S&P Global

Key Risks and Considerations

- Currency headwinds - Reported growth of 4.3% masks underlying currency-neutral growth of just 1.6%

- Americas softness - AMS segment showed flat currency-neutral growth in Q4

- Gross margin guidance - FY26 guidance of 38.5-39.0% implies potential margin compression from record 39.0% in FY25

- Macro uncertainty - Management repeatedly cited uncertain conditions

- Limited analyst coverage - Only 3 analysts covering the stock

What's Next?

Upcoming Catalysts:

- Noravant revenue expected to begin in Q4 2026 ($5-10M in first year)

- Q1 FY 2026 earnings (expected late April/early May)

- 53-week fiscal year effect on Q1 results (extra week adds ~$5-10M to FY26 sales)

- Return-to-office trends impacting Corporate Office segment

- Healthcare and Education spending patterns

Key Metrics to Watch:

- Currency-neutral sales growth acceleration

- Gross margin sustainability near 39% despite 50 bps tariff headwind

- Noravant traction and healthcare patient room penetration

- Automation investments expanding to Europe and Australia

- Healthcare/Education vertical momentum (combined selling team ROI)

Interface will host a conference call on February 24, 2026, at 8:00 a.m. Eastern Time to discuss these results. The webcast will be available at investors.interface.com.