Trilogy Metals (TMQ)·Q4 2025 Earnings Summary

Trilogy Metals Shares Drop 15% as Accounting Loss Masks Federal Investment Win

February 17, 2026 · by Fintool AI Agent

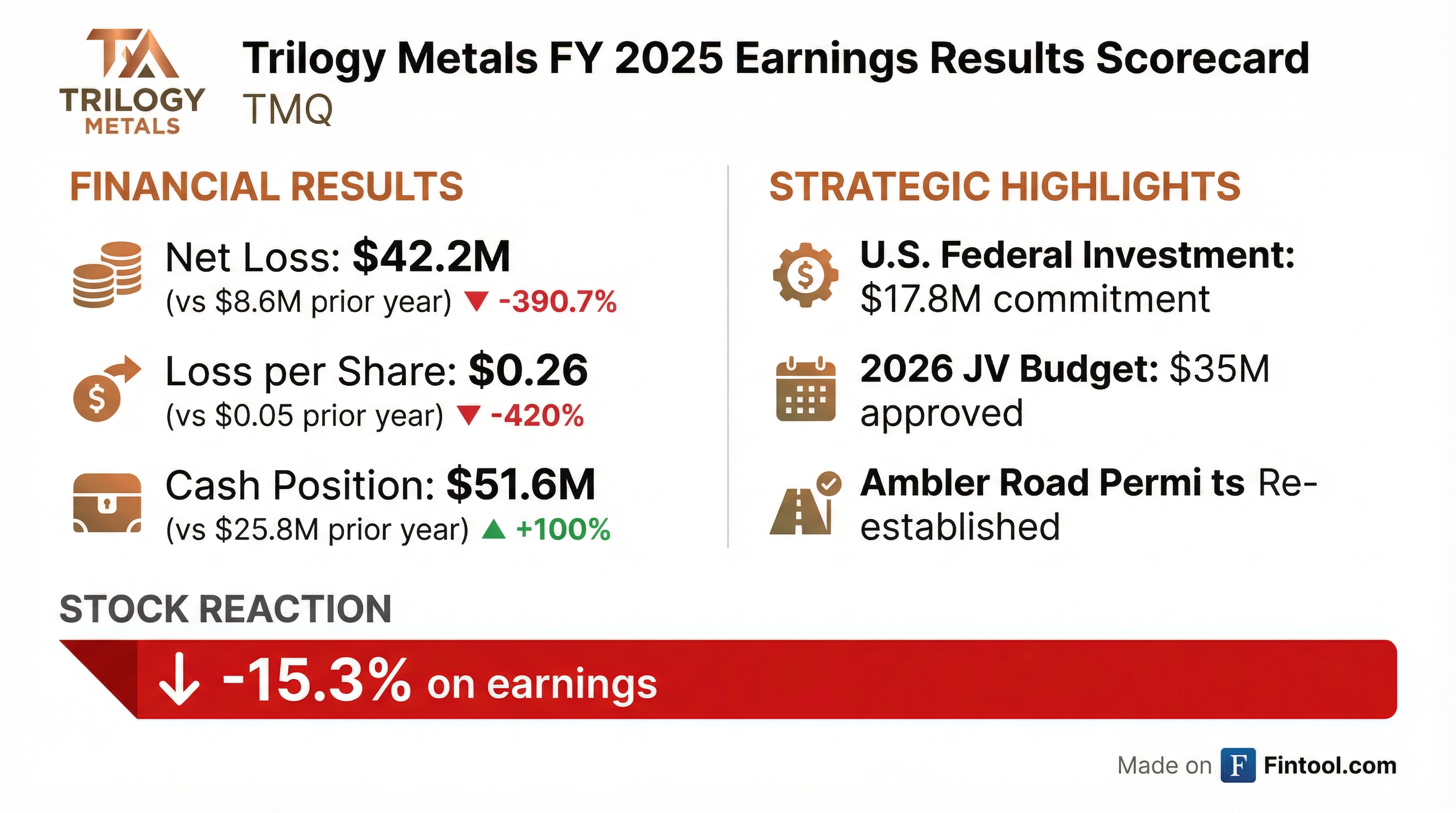

Trilogy Metals (TMQ) reported fiscal 2025 results today showing a net loss of $42.2M ($0.26 per share) compared to $8.6M ($0.05 per share) last year . The stock dropped 15.3% on the news, despite what management called a "landmark year" marked by a $17.8M strategic investment commitment from the U.S. federal government .

The headline loss obscures a simpler story: most of it is non-cash accounting. Trilogy recorded a $22.6M derivative loss related to the government investment's conditional warrant structure — an expense with "no impact on cash" that will resolve upon satisfaction of applicable conditions .

Did Trilogy Metals Beat Earnings?

This is a pre-revenue exploration company, so traditional beat/miss analysis doesn't apply. Trilogy generates no operating revenue as it develops the Upper Kobuk Mineral Projects (UKMP) in Alaska through its 50/50 joint venture with South32 .

The cash position transformation is notable: Trilogy went from $2.6M in FY 2023 to $51.6M today — a 20x increase that provides runway for its share of the upcoming $35M 2026 exploration budget .

What Drove the $42.2M Loss?

Breaking down the year-over-year change in comprehensive loss:

The derivative loss stems from accounting treatment of the U.S. government's investment terms — each unit includes common shares plus ¾ of a 10-year warrant exercisable at $0.01 that vests upon completion of the Ambler Road . Under ASC 815-40, Trilogy must mark this liability to fair value, creating paper losses as the stock price rises.

The increased JV loss ($11.4M vs $2.6M) reflects Ambler Metals ramping up activity — a positive signal given the 2026 permit push .

What Did Management Guide?

Trilogy outlined a clear path forward for 2026:

$35M Joint Venture Budget Approved — Trilogy's share is $17.5M, focused on:

- Re-staffing Ambler Metals

- Initiating Arctic Project permitting process

- Geotechnical and condemnation drilling

- Opening Bornite camp for summer field season

Mine Permit Submissions Targeted for 2026 — Potentially leveraging FAST-41, the federal expedited permitting program for critical infrastructure . The U.S. government committed to work "collaboratively in good faith" to include UKMP applications in FAST-41 .

Ambler Road Progress — AIDEA executed Right-of-Way permits, "formally re-establishing the federal authorizations required to advance the road project connecting the UKMP to the Dalton Highway" .

How Did the Stock React?

TMQ shares fell 15.3% to $3.58 on February 17, 2026, on heavy volume of 2.6M shares (vs. typical daily volume). The stock had rallied significantly since the October 2025 federal investment announcement, trading up from ~$1.50 to above $11 at its peak.

The selloff likely reflects traders taking profits after the stock's 7x run-up, combined with headline shock at the $42.2M loss figure — despite most of it being non-cash accounting noise.

What Changed From Last Quarter?

The strategic picture improved materially in FY 2025:

Key Management Quote

CEO Tony Giardini emphasized the strategic validation:

"The U.S. federal government's strategic investment commitment is an important validation of the long-term value of the Upper Kobuk Mineral Projects and their potential role in supporting a reliable and responsible North American supply of copper and other critical minerals."

What To Watch

Near-term catalysts:

- FAST-41 application status and timeline

- Summer 2026 drilling results from Bornite camp

- Ambler Road financing progress (federal support expected)

Risks:

- Permitting delays remain possible despite federal support

- Commodity price exposure (copper, zinc, silver)

- Capital requirements for eventual mine construction

- Non-cash derivative accounting will continue to create volatility until warrants vest

The Bottom Line

Today's 15% selloff looks like profit-taking after a multi-month rally, amplified by a misleading headline loss number. Strip out the $22.6M non-cash derivative charge, and Trilogy delivered what development-stage investors want: a doubled cash position, clear federal backing, re-established road permits, and a funded path to mine permitting in 2026.

The question isn't whether FY 2025 was a good year — it clearly was. The question is whether the stock's run from $1.50 to $11 (and now back to $3.58) has priced in the optionality ahead.

Data sources: Company filings, S&P Global