Vir Biotechnology (VIR)·Q4 2025 Earnings Summary

Vir Biotechnology Soars 53% After-Hours on $335M Astellas Deal and Positive VIR-5500 Data

February 23, 2026 · by Fintool AI Agent

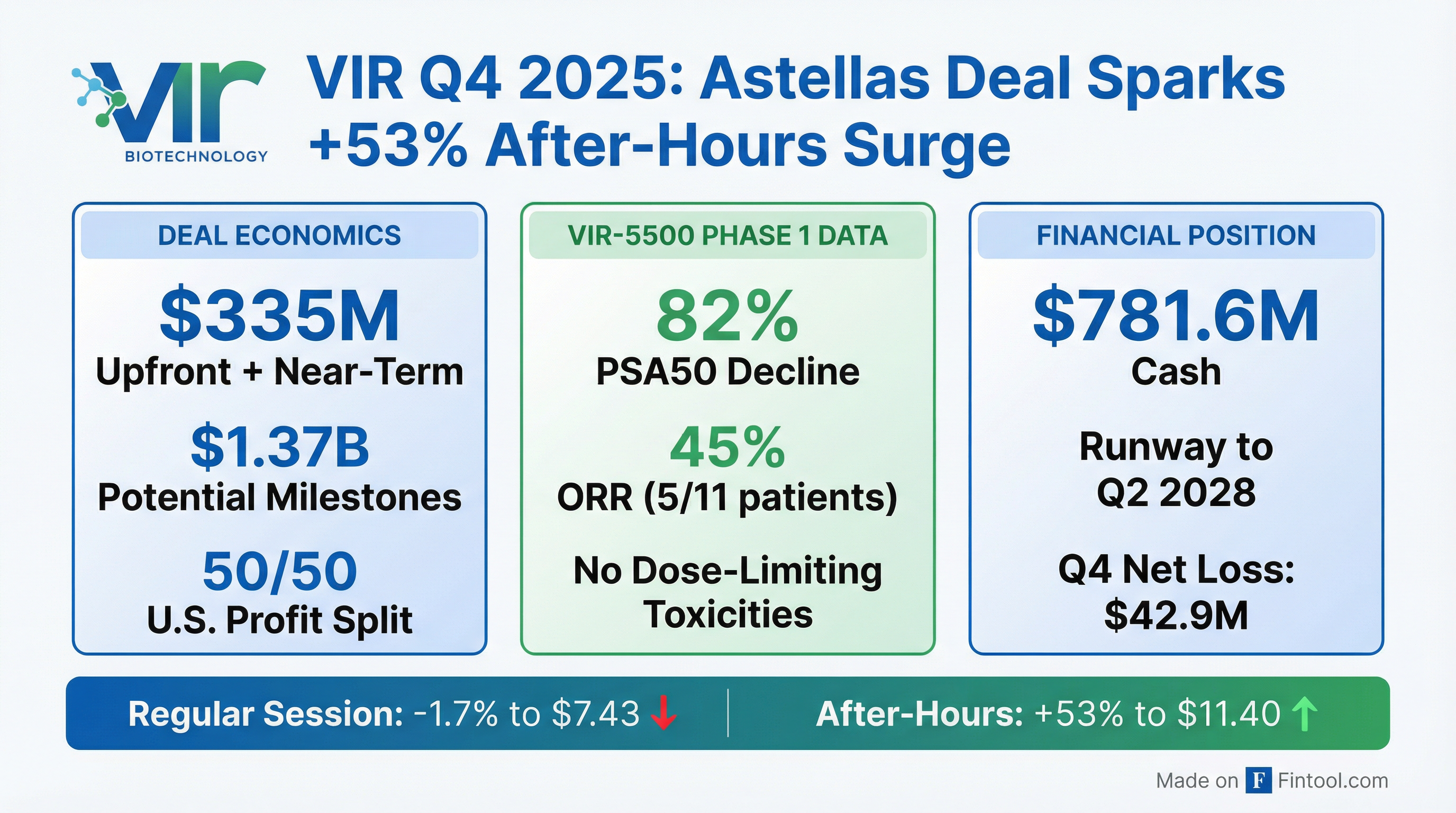

Vir Biotechnology (VIR) announced a transformative global strategic collaboration with Astellas Pharma worth up to $1.7B alongside positive Phase 1 data for its lead oncology asset VIR-5500, sending shares surging 53% in after-hours trading to $11.40 from a $7.43 close.

The clinical-stage biotech delivered Q4 revenue of $64.1M versus $12.4M in the year-ago quarter, driven almost entirely by a $64.3M license revenue recognition from the December 2025 Norgine deal for its hepatitis delta program. Net loss narrowed significantly to $42.9M (-$0.31/share) from $104.6M (-$0.76/share) a year ago, reflecting restructuring benefits.

What's the Astellas Deal?

Astellas agreed to co-develop and co-commercialize VIR-5500, Vir's PRO-XTEN dual-masked T-cell engager targeting PSMA for prostate cancer. The economics are substantial:

Development costs will be shared 40% Vir / 60% Astellas globally, with U.S.-specific studies split equally. Astellas will lead commercialization in the U.S. (Vir retains co-promote option) and has exclusive ex-U.S. rights.

Vir also has an opt-out right: if exercised, Vir would receive up to $1.37B (or $1.60B if meeting a pre-defined funding threshold) in milestones plus tiered double-digit global royalties instead of U.S. profit share.

Why Astellas? CEO Marianne De Backer cited Astellas' "successful track record advancing therapies across the treatment continuum, building blockbuster franchises and delivering value to patients through strategic development alliances." Astellas has deep prostate cancer expertise, having served 1.5 million patients with the disease.

How Did VIR-5500 Perform in Phase 1?

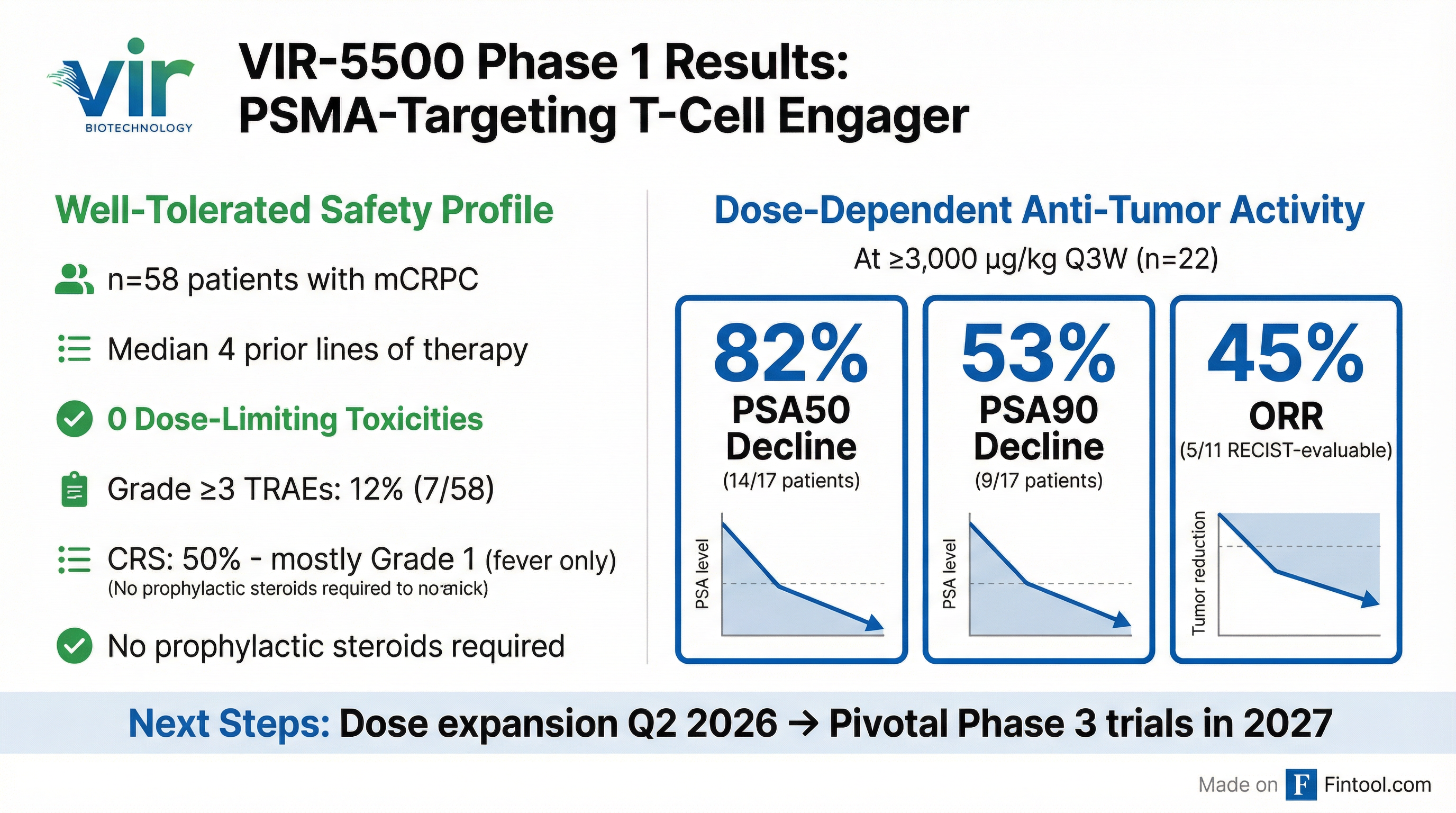

The updated Phase 1 data (n=58, NCT05997615) presented alongside the deal demonstrated a favorable safety profile and promising anti-tumor activity in heavily pre-treated metastatic castration-resistant prostate cancer (mCRPC) patients.

The study enrolled patients with mCRPC who progressed on at least one prior ARPI (100%) and one prior taxane (95%), with median 4 prior lines of therapy and 18% with poor-prognosis liver metastases. All dose escalation cohorts cleared DLT evaluation:

Safety Profile

At higher doses (≥3,000 µg/kg Q3W, n=22), the most common TRAEs were: CRS (59%), back pain (23%), fatigue (23%), infusion-related reaction (23%), and anemia (19%). Grade ≥3 events at higher doses included blurred vision (9%, 2/22) which was incorporated into dose-escalation considerations.

Efficacy in Higher Dose Cohorts (≥3,000 µg/kg Q3W, n=22)

Patients were heavily pre-treated with a median of four prior lines of therapy, and nearly half had visceral metastases. Reductions on PSMA-PET affirmed PSA declines and radiographic responses, with tumor shrinkage observed across multiple lesions including visceral metastases.

Dr. Johann de Bono, Principal Investigator at the Institute of Cancer Research, called the early signs "remarkable" and noted VIR-5500's favorable tolerability "means VIR-5500 could play a role in treating earlier disease."

Compelling Case Studies Highlight Durability

The earnings presentation included five detailed case studies demonstrating durable responses in heavily pre-treated patients:

Notably, Case Study 4 demonstrates activity in a patient who previously received PSMA-radioligand therapy (225Ac-pelgifatama), suggesting VIR-5500 may have utility in RLT-refractory patients.

What's Next for VIR-5500?

How Did the Stock React?

VIR closed the regular session at $7.43 (-1.7%), but exploded 53% higher in after-hours trading to $11.40 following the dual announcement. The stock had been trading near its 52-week range of $4.16-$9.84 prior to the news, reflecting limited visibility into near-term catalysts.

The magnitude of the after-hours move signals the market was not fully pricing in either the Astellas partnership or the strength of the VIR-5500 data. At $11.40, VIR trades at a market cap of approximately $1.6B—still below the total potential deal value of $1.7B+ from Astellas alone.

What Did Management Say?

CEO Marianne De Backer framed this as a "seminal moment" for Vir:

"This is a seminal moment for Vir Biotechnology, marked by key high-potential partnerships on two of our programs showcasing the strength of our pipeline and technology platforms."

On VIR-5500 specifically:

"We are encouraged by VIR-5500's safety and tolerability profile and the early signals of durable anti-tumor activity in a heavily pre-treated population, which validate our PRO-XTEN masking strategy aimed at achieving a differentiated therapeutic index."

On the Norgine hepatitis delta deal from December 2025:

"Our licensing agreement with Norgine signed in December 2025, for the combination of tobevibart and elebsiran for the treatment of hepatitis delta, positions us to reach patients worldwide who face hepatitis delta, the most severe form of chronic viral hepatitis."

What's the Financial Position?

Q4 2025 Results

Full Year 2025 Results

Cash, cash equivalents and investments stood at $782M as of December 31, 2025. The company received $64.3M from Norgine in Q4 as an initial cost reimbursement payment.

Cash Runway: Based on current operating plans and the expected net effects of the Astellas collaboration and equity investment, Vir expects cash to fund operations into Q2 2028.

What Changed This Quarter?

Before Q4 2025:

- VIR was a clinical-stage biotech with two main programs (hepatitis delta, oncology) but limited near-term revenue visibility

- VIR-5500 was in early Phase 1 dose-escalation with limited data

- Cash runway was a concern, with the company running ~$120M quarterly burn

After Q4 2025:

- Astellas validation of PRO-XTEN platform and VIR-5500 with $335M upfront

- Clinical proof-of-concept for VIR-5500 with 82% PSA50 and 45% ORR

- Extended runway to Q2 2028 removes near-term dilution risk

- Two major partnerships (Astellas + Norgine) de-risk both lead programs

What's the Full Pipeline Status?

Hepatitis Delta (CHD)

- Tobevibart + Elebsiran: Phase 2 SOLSTICE showed 88% undetectable HDV RNA at Week 96

- ECLIPSE 1 Trial: Topline data expected Q4 2026

- ECLIPSE 2 & 3 Trials: Topline data expected Q1 2027

- Commercial Partner: Norgine (Europe, Australia, New Zealand)

Oncology (Solid Tumors)

Response data for VIR-5818 in combination with pembrolizumab is expected in H2 2026.

Q&A Highlights

On Post-Radioligand Therapy Activity

Paul Choi (Goldman Sachs) asked about PSA responses in patients with prior radioligand therapy. CMO Mark Eisner highlighted Case 4:

"This patient had received radioligand treatment, an actinium conjugated agent, PSMA targeted agent. That patient had a PSA 99 response and a complete response in the target lesions... at least in this 1 patient, post-RLT, very, very promising results."

Management noted that while they don't have extensive post-RLT data yet, the responses across heavily pre-treated patients "appear to be strong across the board, particularly when we get to the higher doses."

On Platform Validation

CEO Marianne De Backer addressed how VIR-5500 data validates the broader PRO-XTEN platform:

"We really believe that the data we have showed you today validates our dual masking, steric hindrance approach... the lower systemic immune activation is reflected in limited CRS toxicity, very low incidence of high-grade treatment-related AEs, and very limited number of PSMA target-related AEs."

The PRO-XTEN technology enables higher dosing with less frequent administration (Q3W) while maintaining tolerability—a key differentiator versus other T-cell engagers.

On Go-Forward Dose Selection

Philip Nadeau (TD Cowen) asked about specific dose selection. Mark Eisner confirmed:

"We've done a lot of work on that, integrating safety, the efficacy, PSA, PSMA, PAD, RECIST responses... we've gotten to a range in the 3,000 to 3,500 maintenance dose range."

The specific dose will be communicated jointly with Astellas. There was no grade 3 CRS at doses ≥3,000 µg/kg Q3W—only one grade 3 CRS event occurred in a lower-dose patient with intra-participant dose escalation.

On Durability Confidence

Michael Old (Morgan Stanley) asked about confidence in sustaining early responses. Eisner responded:

"We are very encouraged by the RECIST responses... particularly those that have occurred up to 27 weeks and the fact that we're able to confirm RECIST responses in patients. We're also seeing a concordance of RECIST responses with PSMA PET responses and deep PSA responses."

On Development Path & Combinations

Josh Schimmer (Evercore) asked about next steps before Phase 3. Management outlined:

- Q2 2026: Expansion cohorts in late-line mCRPC (monotherapy), early-line mCRPC (combination with enzalutamide), and mHSPC (combination)

- Dose optimization work in parallel to satisfy FDA Project Optimus requirements

- Phase 3 in 2027 with Astellas support

The enzalutamide combination dose escalation is "almost complete" in frontline mCRPC, with similar dosing expected across populations.

On Partnership Strategy for Broader Pipeline

Rina Ruiz (Leerink) asked how the Astellas deal impacts resourcing for other PRO-XTEN programs. De Backer explained:

"From a finance perspective, also, it allows us to leverage certain expenses to our other programs and potentially accelerate those as well. We think that the collaboration certainly has a lot of benefits beyond just for VIR-5500 alone."

For the seven preclinical masked T-cell engagers, Vir will seek partners: "this is just too much for us to move forward on our own."

Dr. de Bono's Clinical Perspective

Dr. Johann de Bono, Principal Investigator at the Institute of Cancer Research, emphasized the clinical significance:

"I believe that the data from this trial show that the dual masking approach works at minimizing cytokine release syndrome... We are reporting multiple amazing responses with little clinically significant CRS."

"Reduction in such pain is incredibly important to these men that we serve... VIR-5500 resulted in pain disappearing following treatment in many patients as their disease regressed."

On liver metastases responses: "In my practice, these patients are very hard to treat, and seeing such remarkable responses in late stage heavily treated prostate cancer is really quite amazing, really unprecedented, maybe even."

What to Watch

- HSR Clearance: The Astellas deal is contingent on Hart-Scott-Rodino antitrust clearance

- VIR-5500 Expansion Data: Monotherapy and combination cohorts initiating Q2 2026

- ECLIPSE Trials: Pivotal hepatitis delta data starting Q4 2026

- VIR-5818 Response Data: H2 2026 readout for HER2-targeting TCE

- ASCO GU Presentation: Full VIR-5500 data presented February 26, 2026

Key Takeaways

- Transformative Deal: Astellas partnership worth up to $1.7B+ validates VIR-5500 and PRO-XTEN platform

- Clinical Proof-of-Concept: 82% PSA50 declines and 45% ORR with clean safety profile

- De-Risked Balance Sheet: Cash runway extended to Q2 2028; equity dilution concerns removed

- Two Partnered Programs: Both lead assets (VIR-5500, hepatitis delta) now have commercial partners

- Stock Reaction: +53% after-hours reflects market underappreciation of pipeline value pre-announcement

Data as of February 23, 2026. Clinical results are preliminary and subject to change as trials progress.