Verastem (VSTM)·Q4 2025 Earnings Summary

Verastem Q4 2025: Revenue Surges 56% as KRAS Cancer Drug Gains Traction

February 4, 2026 · by Fintool AI Agent

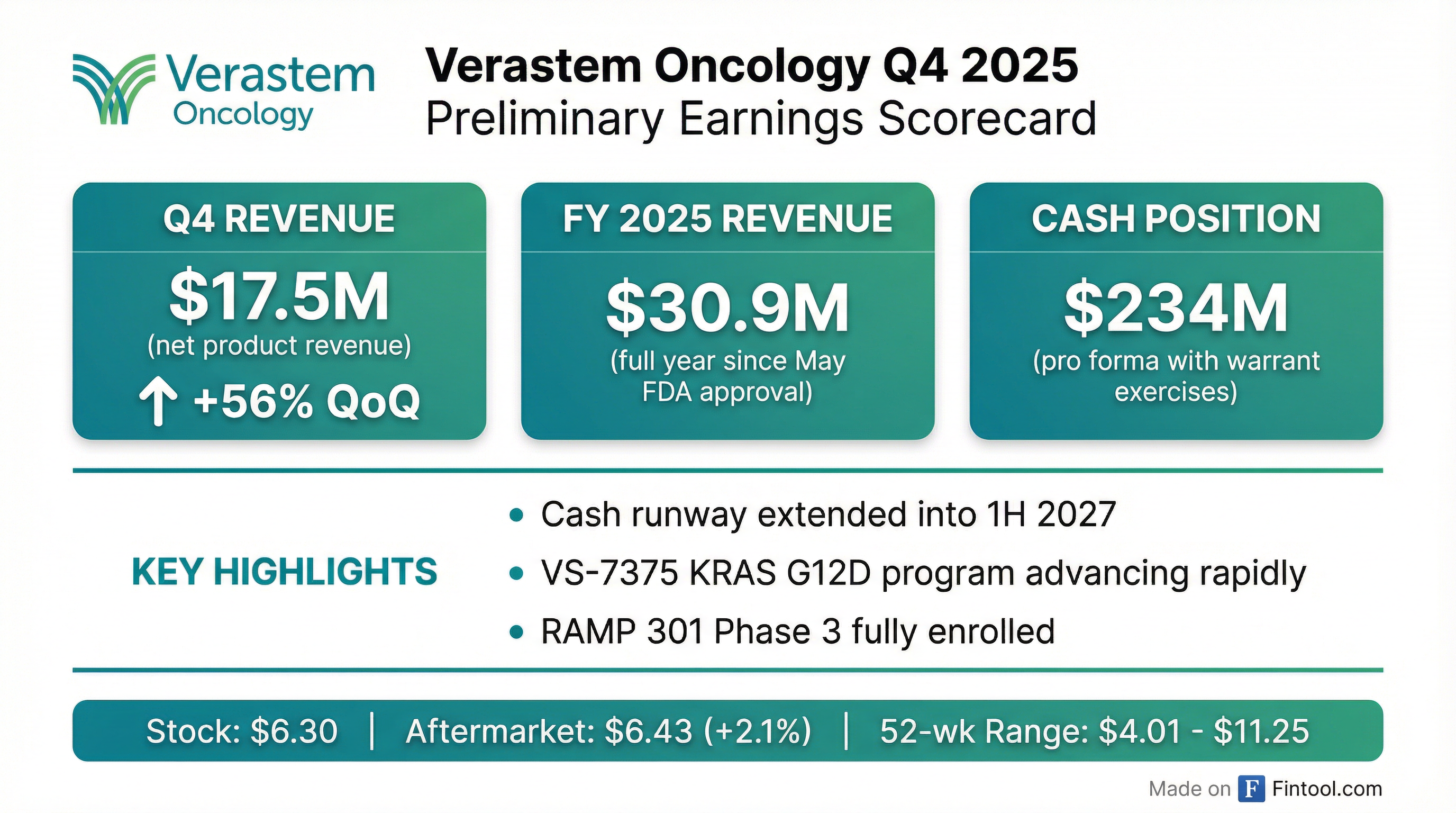

Verastem Oncology reported preliminary Q4 2025 results showing continued strong momentum for its first commercial product, AVMAPKI FAKZYNJA CO-PACK. The company generated ~$17.5M in net product revenue for Q4, up 56% sequentially from $11.2M in Q3 2025 . Full year 2025 revenue totaled approximately $30.9M following the May 2025 FDA approval . The company also provided key updates on its VS-7375 KRAS G12D inhibitor program, which continues advancing toward potential registration trials.

Did Verastem Beat Revenue Expectations?

Yes, significantly. Verastem's Q4 2025 preliminary revenue of ~$17.5M represents a substantial acceleration from its first full commercial quarter:

The company achieved full year 2025 net product revenue of approximately $30.9M in just eight months since FDA approval in May 2025 . Management noted that AVMAPKI FAKZYNJA CO-PACK is the first treatment specifically approved by the FDA for KRAS-mutated recurrent low-grade serous ovarian cancer (LGSOC) .

"2025 was a transformative year for Verastem Oncology and the patients we serve. We transitioned to a commercial-stage company with the launch of AVMAPKI FAKZYNJA CO-PACK." — Dan Paterson, President and CEO

How Did the Stock React?

The stock closed at $6.30 on February 4, 2026, up 0.8% on the day. In after-hours trading, shares rose to $6.43 (+2.1% from close). The stock is trading well below its 52-week high of $11.25 and above its 52-week low of $4.01.

Key context on valuation: At $6.30 per share, Verastem has a market cap of approximately $381M, representing roughly 12x annualized Q4 2025 revenue.

What Is Verastem's Cash Position?

Verastem strengthened its balance sheet with both product revenue growth and warrant exercises:

Key financial highlights from the preliminary announcement:

- Cash warrants exercised: $29.4M net proceeds from exercise of expiring cash warrants as of January 25, 2026

- No remaining cash warrants: All outstanding cash exercise warrants have been exercised

- Extended runway: Cash runway now expected into 1H 2027 (vs. 2H 2026 prior guidance)

- Self-sustaining target: Company anticipates the LGSOC commercial launch will be self-sustaining by 2H 2026

What Did Management Say About VS-7375?

VS-7375, Verastem's oral KRAS G12D (ON/OFF) inhibitor, is the company's most significant pipeline asset. Key updates include:

Clinical Progress:

- Cleared 400, 600, and 900 mg once daily (QD) dose levels with no dose-limiting toxicities (DLTs) and no major toxicities

- Monotherapy expansion cohorts initiated and expanded in 2L PDAC, 2L/3L NSCLC, and tumor agnostic solid tumors

- Combination cohort with cetuximab cleared 400 mg QD dose, now evaluating 600 mg QD

2026 Milestones:

What Changed From Last Quarter?

Several key developments occurred since Q3 2025:

Commercial Momentum Accelerated

- Q4 revenue of $17.5M vs. Q3's $11.2M represents 56% sequential growth

- Full year 2025 revenue of $30.9M exceeded expectations for an 8-month launch period

RAMP 301 Fully Enrolled

- Phase 3 confirmatory trial in recurrent LGSOC completed enrollment as of December 2025

- Topline primary endpoint readout expected mid-2027

- Study will serve as confirmatory trial for initial indication and could expand to all LGSOC regardless of KRAS status

Japan Data Updated

- RAMP 201J Phase 2 trial in Japan showed 38% confirmed ORR overall (6/16 patients)

- KRAS-mutant patients: 57% ORR (4/7), 100% DCR (7/7)

- KRAS wild-type patients: 22% ORR (2/9), 89% DCR (8/9)

- 11 of 16 patients remain on treatment; no discontinuations due to adverse events

Cash Position Strengthened

- $67M increase in cash position from Q3 ($137.7M → $205M)

- Additional $29.4M from warrant exercises in January 2026

- Runway extended from 2H 2026 to 1H 2027

RAMP 203 Program Discontinued

- Company announced in December 2025 that it is discontinuing RAMP 203 (avutometinib ± defactinib + sotorasib in KRAS G12C NSCLC)

- Resources being pivoted to accelerate VS-7375 development

What Are the Key Risks?

Several factors warrant investor attention:

-

Accelerated Approval Contingency: AVMAPKI FAKZYNJA CO-PACK was approved under accelerated approval. Continued approval is contingent on the RAMP 301 confirmatory trial results expected mid-2027

-

FDA Workforce Concerns: Management noted risks "associated with the current administration's reductions to the FDA's workforce" that "may lead to disruptions and delays in the FDA's review and oversight"

-

Competitive Landscape: KRAS G12D inhibitor space is highly competitive with multiple programs from major pharma companies

-

Small Market: KRAS-mutated LGSOC is a rare disease with limited patient population, though expansion to wild-type could significantly increase addressable market

What's Next for Verastem?

Near-term catalysts:

- Full Q4 2025 and FY 2025 results in early March 2026

- VS-7375 interim Phase 1/2 update in 1H 2026

- RAMP 205 expansion cohort update with 6+ months follow-up in Q2 2026

- FDA engagement on VS-7375 registration path in 1H 2026

Medium-term catalysts:

- RAMP 301 topline primary endpoint readout in mid-2027

- Potential regulatory expansion into Europe and Japan

Management will participate in a fireside chat at the Guggenheim Emerging Outlook: Biotech Summit on February 11, 2026 .

This is a preliminary Q4 2025 update. Final audited results and earnings call are expected in early March 2026. All revenue figures are preliminary, unaudited estimates subject to adjustment.