Select Water Solutions (WTTR)·Q4 2025 Earnings Summary

Select Water Solutions Posts Record EBITDA Year as Infrastructure Strategy Gains Traction

February 17, 2026 · by Fintool AI Agent

Select Water Solutions (NYSE: WTTR) delivered a record year for Adjusted EBITDA in 2025, with Q4 results showcasing the company's strategic pivot toward high-margin water infrastructure. The quarter featured a record performance from Chemical Technologies, continued infrastructure build-out in the Northern Delaware Basin, and management guidance pointing to 20-25% revenue growth for Water Infrastructure in 2026.

Did Select Water Solutions Beat Earnings?

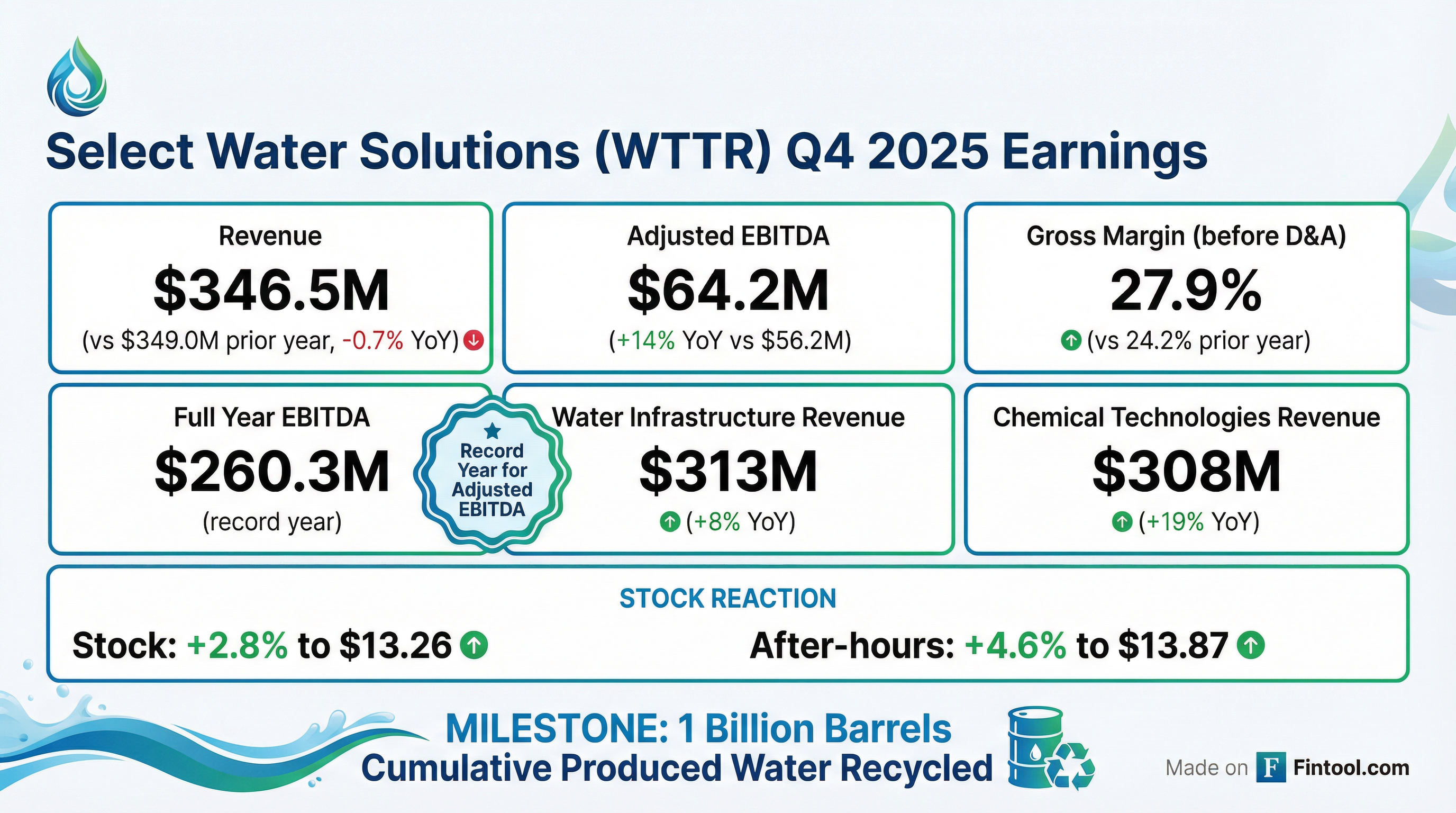

Select Water reported Q4 2025 revenue of $346.5 million and Adjusted EBITDA of $64.2 million, representing a 14% year-over-year increase in EBITDA despite relatively flat revenue.

Full year 2025 Adjusted EBITDA reached $260.3 million, a record for the company, compared to $258.4 million in 2024.

What Changed From Last Quarter?

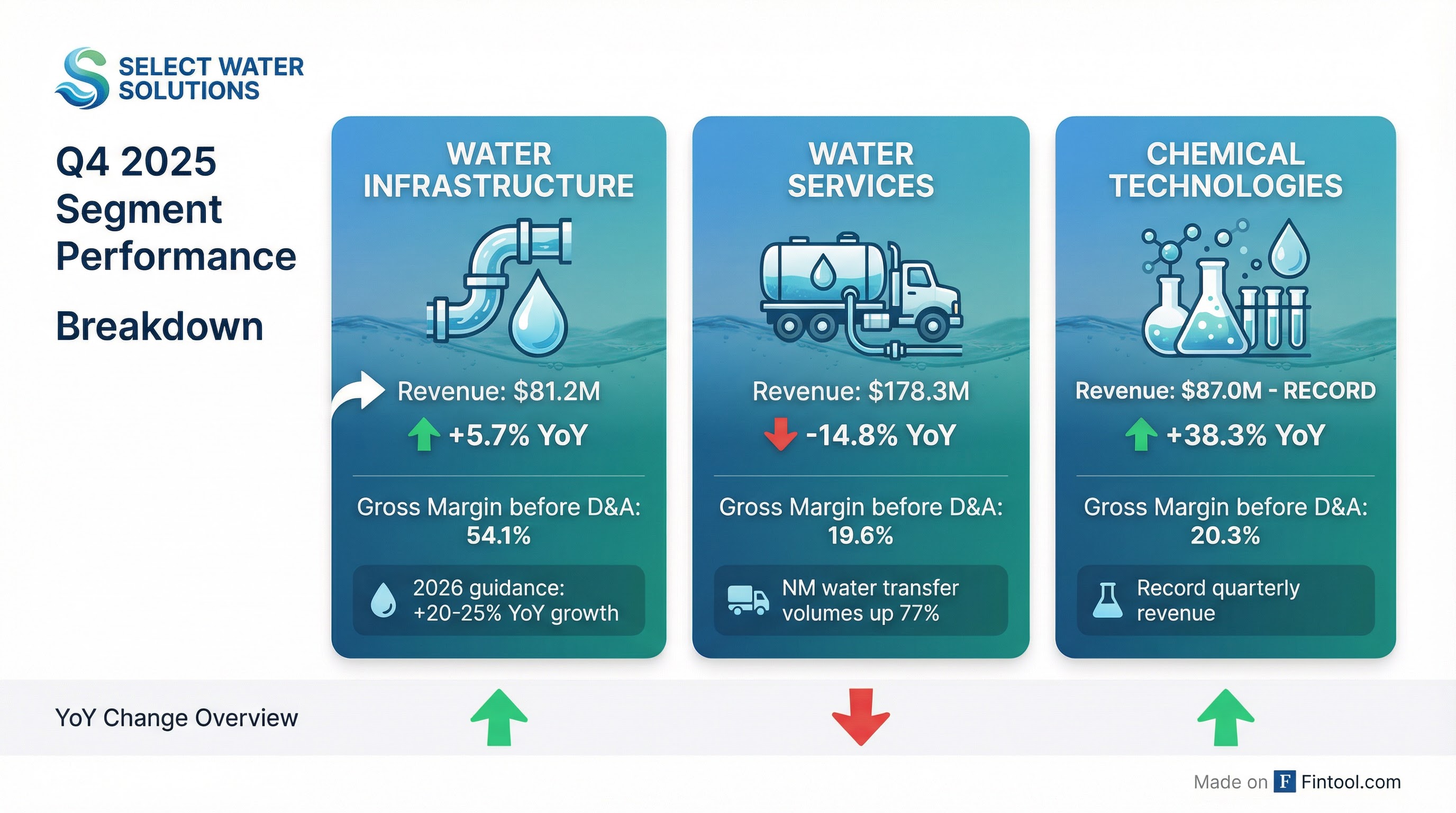

The most notable shift was the 77% sequential increase in water transfer revenues in New Mexico, driven by temporary logistics supporting the Northern Delaware infrastructure build-out. This caused Water Services to outperform expectations despite a broader trend of volumes shifting onto fixed infrastructure.

Key changes:

- Chemical Technologies posted a record quarter at $87.0M revenue (+38.3% YoY), driven by market share gains and new product initiatives

- Water Infrastructure revenue grew 3% sequentially to $81.2M, with project timing delays pushing some growth into 2026

- Total debt increased to $320M (term loan + revolver) from $85M at year-end 2024, reflecting infrastructure investment

How Is Each Segment Performing?

Water Infrastructure remains the growth engine. Since 2021, segment revenue has grown more than 800%, supported by the company's recycling-first commercial platform. The segment's 54% gross margin before D&A dwarfs the other segments.

Chemical Technologies delivered a breakout quarter, with 45% year-over-year growth in gross profit before D&A for full year 2025. Management attributed gains to R&D-led product initiatives driving higher product margins.

Water Services declined due to the OMNI divestiture in Q3 2025 and the ongoing shift from variable services to fixed infrastructure.

What Did Management Guide?

Management provided detailed Q1 2026 and full-year 2026 guidance:

Q1 2026 Guidance:

- Consolidated Adjusted EBITDA: $65-68 million (sequential growth)

- Water Infrastructure revenue: +7-10% QoQ

- Chemical Technologies revenue: High $70s to $80M

Full Year 2026 Guidance:

- Water Infrastructure: 20-25% YoY revenue growth

- Net capex: $175-225 million (after $10-15M asset sales)

- Maintenance capex: ~$50-60M, consistent with 2025

- SG&A: 5-10% reduction vs. 2025

CEO John Schmitz emphasized confidence in the trajectory: "We believe we are establishing a strong foundation for continued growth into 2027. We anticipate an increasingly improved free cash flow profile over time with the ongoing maturation of the Water Infrastructure segment."

What Strategic Milestones Were Announced?

The quarter marked several significant achievements:

-

1 Billion Barrels Recycled — Select surpassed one billion barrels of cumulative produced water recycled, a milestone from its multi-year infrastructure strategy.

-

950,000 Acres Added in 2025 — New dedications carry an 11-year average contract length, providing long-term visibility.

-

15 Million Barrels of New MVCs — Minimum volume commitments secured since Q4 start, with 179,000 dedicated acres across new projects.

-

Northern Delaware Build-Out — Multiple new agreements including:

- 10-year and 7-year produced water handling agreements in Lea County, NM

- Asset conveyance from a key customer (3 pits + disposal permit)

- Acquisition of disposal facilities in Winkler County, TX

-

Rockies Expansion — 15-year agreement for gathering pipeline infrastructure with 9.6M barrel MVC and 24,000-acre dedication.

How Did the Stock React?

WTTR shares rose 2.8% to $13.26 during regular trading on February 17, 2026. After-hours trading pushed the stock higher, reaching $13.87 (up 4.6% from the close).

The stock is trading near 52-week highs, having rallied from the $7.20 low in mid-2025. The market appears to be rewarding the strategic shift toward contracted infrastructure and the margin expansion story.

What Are the Key Risks?

Management's forward-looking statements highlighted several risk factors:

- Customer schedule variability — Project timelines depend on operator development schedules, which can shift

- Leverage increase — Total debt rose to $320M from $85M YoY, though liquidity improved to $163.6M

- Commodity exposure — While infrastructure provides stability, Water Services remains tied to drilling activity

- OPEC+ policy — Production decisions by oil-producing nations impact U.S. drilling activity

- Regulatory risk — Water handling, hydraulic fracturing, and environmental regulations could impact operations

Forward Catalysts

Earnings Call: Wednesday, February 18, 2026, at 11:00 AM ET / 10:00 AM CT

Next Steps:

- View WTTR Company Page

- Read Full Transcript (available after call)

- View Q3 2025 Earnings