EXXON MOBIL (XOM)·Q4 2025 Earnings Summary

ExxonMobil Q4 2025 Earnings: $28.8B Full-Year, Record Production

January 30, 2026 · by Fintool AI Agent

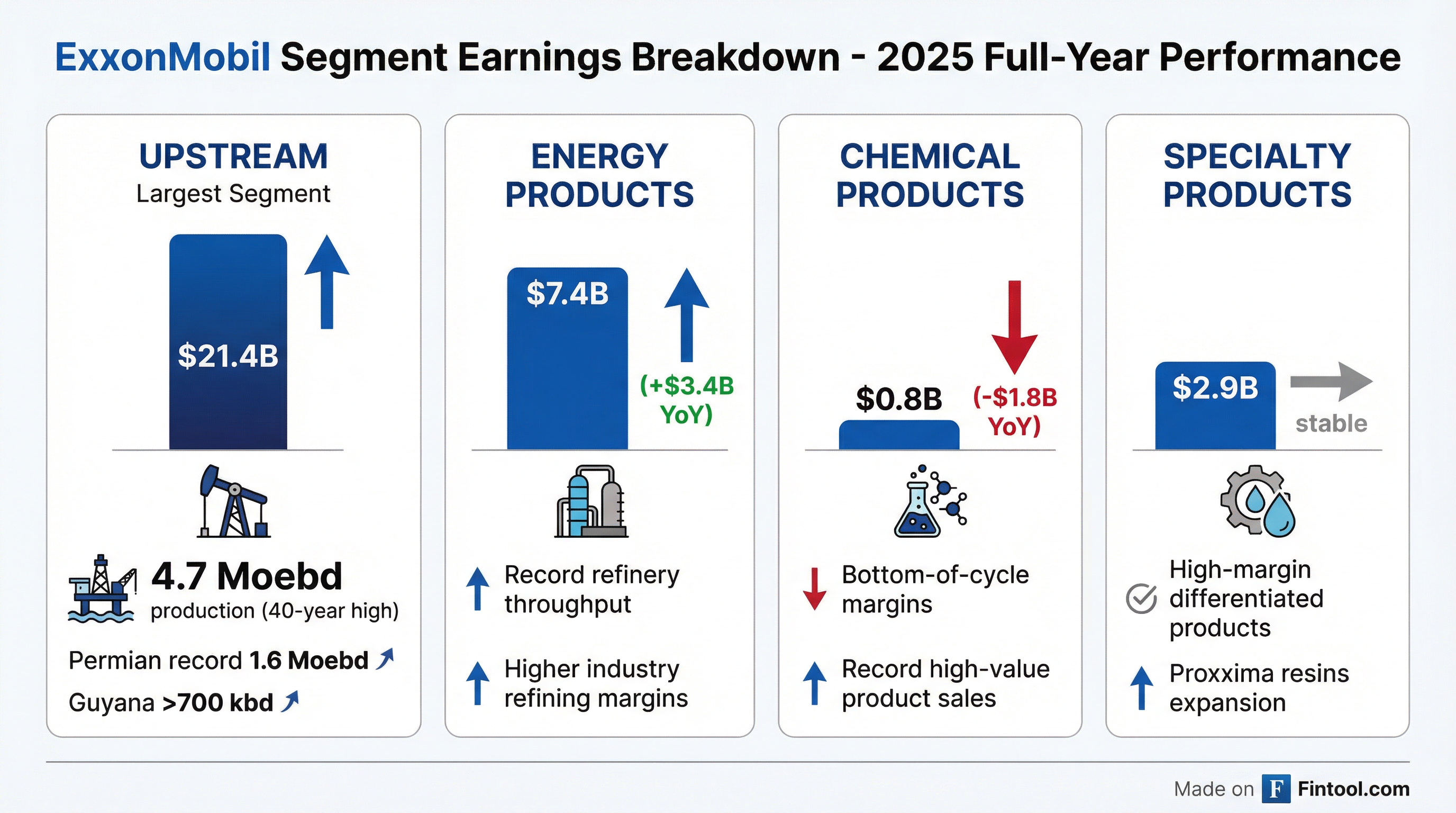

ExxonMobil reported fourth-quarter 2025 earnings of $6.5 billion ($1.53 per share), down from $7.6 billion in Q4 2024, as weaker crude prices and bottom-of-cycle chemical margins pressured results . Despite the quarterly decline, the company delivered full-year earnings of $28.8 billion while achieving its highest annual Upstream production in more than 40 years at 4.7 million oil-equivalent barrels per day .

The stock rose +2.1% on the release, trading at $140.51.

CFO Transition: Kathy (outgoing CFO) will be succeeded by Neil Hansen, a 25-year ExxonMobil veteran who has spent most of his career in the finance organization .

Did ExxonMobil Beat Earnings?

Q4 2025 results came in below both Q4 2024 and street expectations:

Key Drivers:

- Lower crude prices: Brent averaged $63.69/bbl in Q4, down from $69.07 in Q3

- Impairments: $1.7B in Q4, including $640M inventory optimization charge

- Chemical weakness: Bottom-of-cycle margins resulted in a $281M segment loss

Full-year 2025 performance tells a stronger story:

What Did Management Say?

CEO Darren Woods emphasized the company's structural transformation:

"ExxonMobil is a fundamentally stronger company than it was just a few years ago, and our 2025 results demonstrate that. Our transformation is delivering a more resilient, lower-cost, technology-led business with structurally stronger earnings power, grounded in advantaged assets, disciplined capital allocation, and execution excellence."

Management highlighted that structural cost savings have reached $15.1 billion since 2019—more than all other integrated oil companies combined .

How Is Each Segment Performing?

Upstream: Record Production Despite Price Headwinds

Highlights:

- Q4 production hit 5.0 Moebd, a new quarterly record

- Permian volumes reached 1.8 Moebd (quarterly record)

- Guyana gross production approached 875 kbd (quarterly record)

- Yellowtail (Guyana's 4th development) started up four months ahead of schedule

- Bacalhau (Brazil) started up in Q4

- Golden Pass LNG Train 1 achieved mechanical completion

Energy Products: Refining Strength

Energy Products delivered the standout quarterly performance with record global refinery throughput (on a same-site basis) . Full-year earnings of $7.4B were up $3.4B versus 2024, driven by higher industry margins and advantaged project contributions .

Chemical Products: Bottom-of-Cycle

Chemical Products reported a Q4 loss of $281M due to oversupply and bottom-of-cycle margins . Management noted record high-value product sales but emphasized the challenging margin environment. The China Chemical Complex continues ramping up .

Specialty Products: Steady High-Margin Performance

Specialty Products delivered $2.9B in full-year earnings with record high-value product sales . Proxxima resins production capacity more than tripled during 2025 .

What Did Management Guide?

2026 Outlook

Q1 2026 Specific Guidance:

- Production expected 100-200 koebd lower due to timing, downtime, and absence of favorable entitlements

- Higher seasonal scheduled maintenance in Product Solutions

- First full quarter without Gravenchon refinery (~240 kbd)

- Corporate & financing expenses expected at $0.8-1.0B

2030 Plan Update

Management raised 2030 earnings and cash flow growth plans by ~$5B each with no increase in capital spending :

How Did the Stock React?

XOM shares rose +2.1% on the earnings release, closing at $140.51—hitting a new 52-week high of $142.34 intraday. The positive reaction despite the earnings decline suggests the market valued:

- Production execution: 40-year high annual production with record quarterly Permian and Guyana output

- Capital discipline: Maintaining $20B buyback commitment while guiding lower capex

- Balance sheet strength: Industry-leading debt-to-capital of 14.0% and net-debt-to-capital of 11.0%

- Dividend growth: 43 consecutive years of annual dividend-per-share growth, with Q1 2026 dividend raised to $1.03/share

What Changed From Last Quarter?

Better:

- Production hit 5.0 Moebd quarterly record vs 4.8 Moebd in Q3

- Energy Products earnings nearly doubled QoQ ($3.4B vs $1.8B)

- Indicative refining margin improved to $18.3/bbl from $17.5/bbl

- Golden Pass LNG achieved mechanical completion

Worse:

- Upstream earnings fell $2.2B QoQ on lower crude realizations

- Chemical Products swung to a $281M loss from $515M profit

- Brent averaged $63.69/bbl vs $69.07/bbl in Q3

- $1.7B impairment charges vs minimal in Q3

Capital Allocation and Shareholder Returns

ExxonMobil distributed $37.2 billion to shareholders in 2025—more than all but five S&P 500 companies :

Dividend Track Record: 43 consecutive years of annual dividend-per-share growth . The Q1 2026 dividend of $1.03/share represents a 4% increase .

Key Projects Delivered in 2025

Management delivered 10 of 10 key projects in 2025, expected to add $3B in earnings on a constant price and margin basis in 2026 :

Q&A Highlights: What Did Management Say?

Guyana Exploration & Force Majeure

On the Stabroek Block exploration license expiring in late 2027, CEO Darren Woods noted the company continues drilling in accessible areas while managing the force majeure portion under Venezuela border dispute:

"The portion of the block that's under force majeure as a result of the border dispute remains there... One of the advantages of force majeure is it pauses the clock, and so we will have an opportunity to do what we need to do in that portion of the block when it's available to us."

The International Court of Justice ruling on the border dispute will be a critical milestone .

Venezuela Re-Entry

When asked about Venezuela, Woods acknowledged he called it "uninvestable" at the White House but sees potential:

"What I said at the White House was, given the current fiscal structures in place, legal, that you couldn't invest, but that there was opportunities to address that... The Trump administration is committed to doing that... stabilizing the country, kickstarting the economy, and then ultimately transitioning into a more representative democratically elected government."

ExxonMobil offered to send a technical assessment team to support administration decision-making .

LNG Expansion: Golden Pass, Mozambique, Papua New Guinea

- Golden Pass: First LNG expected "very early March" with commissioning and startup underway

- Mozambique: FID expected back half of 2026; used the force majeure delay to drive cost innovation and improve the design

- Papua New Guinea: Continuing to work through development with cost-competitive design

Data Center CCS Opportunity

Woods revealed serious, substantive conversations with hyperscalers about gas-fired power generation with carbon capture for data centers:

"I would say that today we are engaged in very serious, substantive conversations with a number of the hyperscalers. There is a commitment to finding a competitive way to decarbonize these data centers... My hope is and expectation is we should see that work manifest itself, hopefully by year-end, with a project announcement."

Permian Technology & Recovery

On technology deployment in the Permian:

"We're not changing our approach of maximizing ultimate recovery... Simply put, there is no near-term peak Permian for us. Our growth trajectory remains robust, and we expect to exceed 2.5 million oil equivalent barrels a day beyond 2030."

- Lightweight proppant deployed in ~25% of wells in 2025, targeting 50% by end of 2026

- 40+ stackable technologies in various stages of testing and deployment

- Management actively pursuing technology to improve recovery from already-drilled areas

Data & AI Transformation

The company is consolidating from 10+ ERP systems to a single platform with unified data nomenclature:

"It will be the first time in the history of this company that we can actually tap into everything that we're doing across the company. And when you couple that with the opportunity with AI and the data set that that represents, I don't think there's a company out there that can match what we're trying to accomplish here."

Key metrics: 97% fewer profit centers, 70% fewer cost centers, eliminating 65 million lines of custom code .

Chemical Segment Outlook

On chemical margins, Woods acknowledged the supply-side challenge but emphasized differentiation:

"Despite record levels of demand and very good growth in demand, there continues to be a lot of capacity that comes on that expresses the margin... Our focus continues to be the same: sell into high-value products, continue to drive costs down, be efficient, take advantage of every lever that you've got to pull."

Battery Materials Progress

ExxonMobil's advanced battery anode graphite program is delivering exceptional performance: 30% faster charging, up to 3% higher available capacity, and up to 4x battery life .

Risks and Concerns

- Commodity exposure: Q4 demonstrated sensitivity to crude prices—~$6B headwind from lower prices YoY

- Chemical cycle: Bottom-of-cycle margins dragged full-year Chemical earnings to $0.8B (vs $2.6B in 2024)

- Q1 2026 seasonality: Guided 100-200 koebd lower production and higher maintenance

- Geopolitical: Tengiz depreciation added ~$900M to 2025 expenses

- Guyana exploration timeline: Stabroek Block exploration license expires late 2027; force majeure portion remains inaccessible pending ICJ ruling

Summary

ExxonMobil's Q4 2025 results reflected challenging commodity conditions but showcased operational excellence with record production. The company's transformation thesis—advantaged assets, structural cost savings, and disciplined capital allocation—continues to deliver industry-leading returns despite lower oil prices. With $37.2B returned to shareholders, 43 years of dividend growth, and a clear runway to 2030, XOM maintains its position as the integrated oil major to beat.

Key Numbers:

- Q4 2025 Earnings: $6.5B (GAAP) / $7.3B (adjusted)

- Full-Year 2025 Earnings: $28.8B

- 2025 Production: 4.7 Moebd (40-year high)

- 2025 Shareholder Returns: $37.2B

- 2026 Capex Guidance: $27-29B

Forward Catalysts:

- Golden Pass first LNG: Early March 2026

- Mozambique LNG FID: H2 2026

- Data center CCS project announcement: Potential by year-end 2026

- Permian lightweight proppant: 50% of wells by year-end 2026

Next earnings: Q1 2026 results expected late April 2026

Related Documents: