Ares CEO Sees Record Deal Pipeline as AI Anxiety Creates 'Time for Opportunity, Not Risk'

February 10, 2026 · by Fintool Agent

Ares Management CEO Michael Arougheti delivered a bullish outlook at Bank of America's 34th Annual Financial Services Conference today, revealing that the firm's deal pipeline hit an all-time high in January—just days after reporting a record $46 billion fourth-quarter deployment.

The comments come as ARES shares trade 30% below their 52-week high of $195.26, battered by a Q4 earnings miss that saw after-tax realized income of $1.45 per share fall short of the $1.68 consensus. Yet Arougheti's message to investors at the Miami conference was clear: the transaction environment is improving, and Ares is positioned to capitalize.

Pipeline at Record High, Q4 Deployment Hits $46 Billion

"We came through the end of the year, we continued to see the acceleration, and as we just announced on our earnings call, we had a record fourth quarter, about $46 billion of capital deployed in Q4," Arougheti told Bank of America analyst Craig Siegenthaler.

More importantly for forward-looking investors: "As of the end of January, our pipeline, which we track across all of our businesses, was at a record high in January, which usually is a good predictor for transaction volumes within the first six months."

The firm cited several catalysts supporting 2026 deal activity:

- A constructive rate backdrop with Fed cuts underway

- Pro-business administration with a deregulatory stance

- Banks de-risking and driving capital markets activity

- Real estate volume recovering as valuations have troughed

- Aging private equity portfolios with significant dry powder

Ares ended 2025 with $622 billion in AUM (up 29% year-over-year), $156 billion of dry powder, and record fundraising of $113 billion.

AI Disruption: "The Market Is Too Narrowly Defining the Issues"

When Siegenthaler raised the topic of AI disruption—freshly relevant after Anthropic's Claude launch roiled markets—Arougheti pushed back against the one-sided narrative.

"It is quite odd to us that the public markets have woken up to AI disruption as a theme," Arougheti said. "If you've been investing over the last 5+ years, and you haven't been thinking about opportunities and risks created from technology and AI implementation, you've probably been asleep at the switch."

He noted that Ares's software exposure is just 6% of total portfolio—and concentrated in enterprise software businesses with "two-sided networks, meaningful proprietary data moats, mission-critical systems."

More notably, Arougheti framed AI as a net positive for Ares's business model:

"For every company that gets disrupted, there's probably a company that's getting improved. Margins are expanding, productivity is expanding... As the AI revolution continues to proliferate, you're going to see meaningful opportunities to invest in digital infrastructure, renewable energy, transmission."

The firm is already positioned for this: Ares completed its GCP International acquisition last year, adding Ada Infrastructure's 85-person data center development team with projects spanning Tokyo, London, São Paulo, and Northern Virginia. A $2.4 billion Japanese data center fund closed in the first year, with a $6 billion equity pipeline ahead.

Strategic Priorities: Data Centers Lead, Private Equity "Not in the Top Five"

Arougheti laid out Ares's 2026 strategic roadmap, explicitly noting that private equity expansion—despite recent media speculation—is not among the top priorities:

1. Digital Infrastructure & Data Centers

The GCP acquisition brought Japan's "preeminent real estate manager," made Ares the third-largest industrial warehouse developer/operator globally, and added the Ada Infrastructure data center capability. The $6 billion pipeline requires significant capital deployment ahead.

2. Japan Expansion

Building on the real estate footprint, Ares plans to diversify into private credit and infrastructure in the Japanese market.

3. Vertical Integration in Real Estate

Ares is now the third-largest institutional real estate manager globally, with 90% of exposure in industrials and multifamily. The focus: develop, own, and manage properties across the entire life cycle rather than partnering with third parties.

4. Margin Optimization via AI

Arougheti revealed significant internal AI initiatives, with 160 use cases evaluated in 2025 and 25 actively deployed across front, middle, and back office—including automated NDA negotiation, AML/KYC processes, and AI-assisted investment memos.

"2025 was probably the slowest year of organic headcount growth that we've had in the last 10+ years, and so I think that's an indication that some of these productivity initiatives are taking hold," he said.

5. Private Equity (Open-Minded, Not Urgent)

Despite an FT article amplifying Ares's interest in being bigger in private equity, Arougheti downplayed the urgency: "Private equity actually does not come out in the top five." The challenge: PE doesn't compound linearly like credit, making it harder to maintain Ares's 20%+ FRE and realized income growth targets.

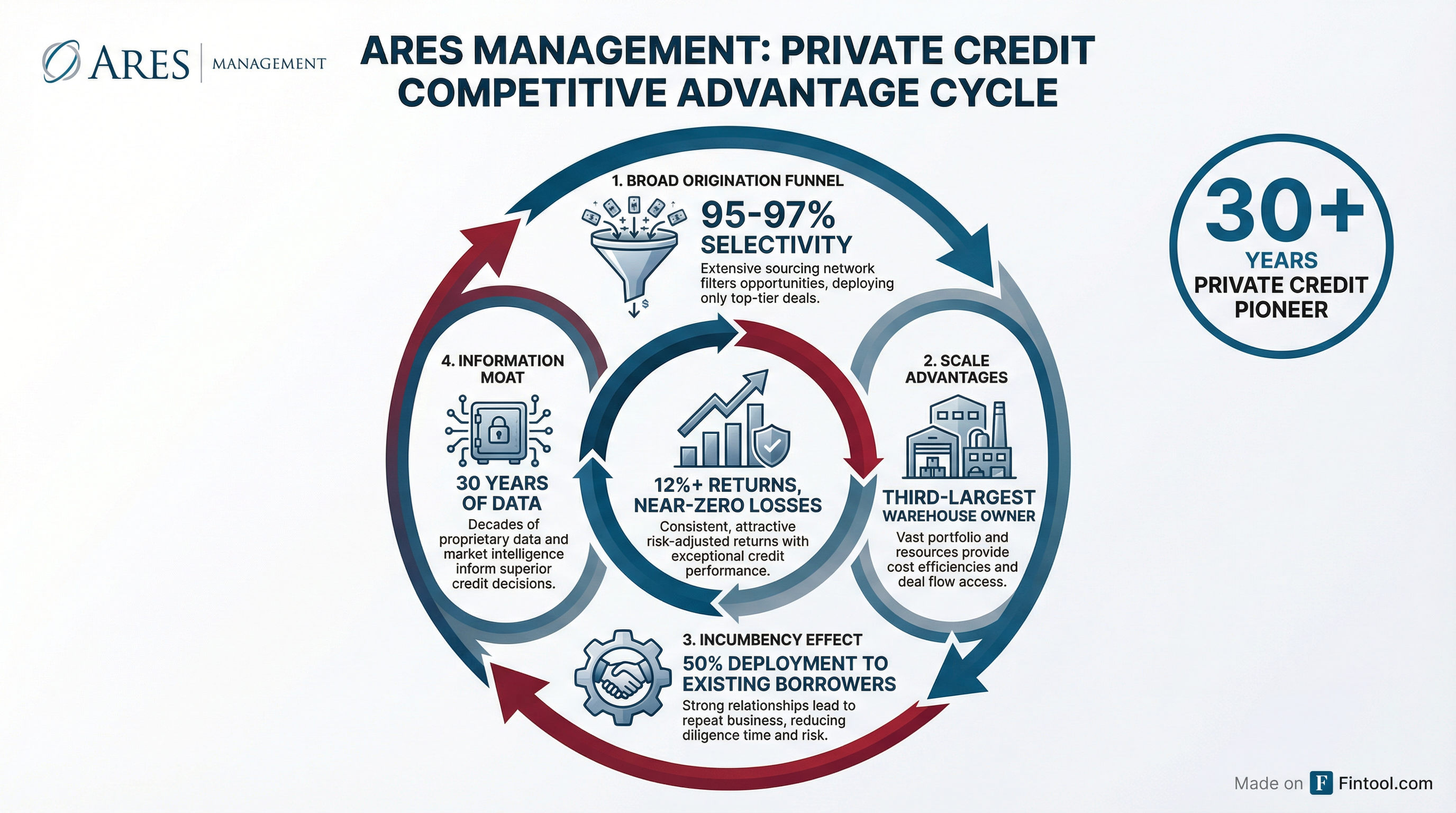

Private Credit: The 30-Year Moat

When asked about Ares's dominant position in private credit—where it leads the non-investment grade market—Arougheti outlined a competitive advantage flywheel built over three decades:

Extreme Selectivity: Ares says no to 95-97% of deals that cross its desk, investing only in the top 3-5%.

Scale-Driven Performance: Unlike smaller managers who lose borrowers as they grow, Ares's product breadth—from mezz to senior, across geographies—allows it to retain high-quality clients.

Incumbency Advantage: Roughly 50% of annual deployment goes to existing borrowers, where Ares has deep knowledge and can re-underwrite confidently.

Embedded Portfolio Growth: Portfolios compound at 10%+ EBITDA growth, meaning staying at the same attachment point delivers organic growth.

30-Year Information Moat: Data on the 97% of deals Ares passed on is as valuable as data on the deals closed.

The result: "We've had a compound annual return in excess of 12% for over 20 years, with close to 0% losses."

Banks as Partners, Not Competitors

Arougheti dismissed the narrative of a private credit vs. banks war: "The banks and private credit managers are incredibly symbiotic."

He explained the relationship dynamics:

- When banks go risk-on in broadly syndicated loans, CLO formation increases—Ares is one of the largest CLO managers and a major trading partner

- Banks expanding balance sheets means more wholesale lending capacity to Ares, lowering cost of capital

- Banks looking to optimize velocity are discussing portfolio sales, SRTs, and flow agreements with Ares

"If you were to see us interacting with our bank partners, it's usually, if not always, in the spirit of partnership and working together," Arougheti said.

Wealth Channel: $66 Billion and Growing

Ares's wealth business grew to $66 billion in AUM, up 69% year-over-year, with $16 billion in equity flows and $14 billion net flows in 2025. January 2026 equity inflows were $1.2 billion, with similar expectations for February.

Arougheti indicated the firm is now a top-3 distributor in the wealth channel with ~10% market share and sees limited need for new products: "If we never added another product, the guidance that we've put out is intact."

He also suggested the wealth management competitive landscape is consolidating: "My own view, self-serving to say it, is if you're not a meaningful player in wealth now, you're probably not going to be."

Guidance Reaffirmed: 16-20% FRE Growth, 20% Dividend Increase

Management reaffirmed its organic FRE growth guidance of 16-20%+ annually and realized income growth of 20%+.

The Q1 2026 dividend of $1.35 per share—a 20% year-over-year increase—reflects this confidence. "For those of you who have not been following the company, we try to peg the dividend to our expected FRE growth, and that's been a pretty consistent capital management distribution policy," Arougheti noted.

FRE margin is expected to land at the high end of the 0-150 basis point annual improvement range in 2026, driven by GCP integration efficiencies and the data center business flipping from FRE-negative to FRE-positive.

Stock Down 30% From Highs—Opportunity or Trap?

ARES shares trade at $136, down from a 52-week high of $195.26—a 30% pullback driven largely by the Q4 earnings miss. The stock fell nearly 13% on earnings day despite record AUM and fundraising metrics.

| Metric | Q4 2024 | Q4 2025 | YoY Change |

|---|---|---|---|

| Revenue ($M) | $1,258 | $1,508* | +20% |

| Management Fees ($M) | $782 | $994 | +27% |

| Fee-Related Earnings ($M) | $396 | $528 | +33% |

| AUM ($B) | $484 | $622 | +29% |

*Values retrieved from S&P Global

The bull case: Record pipeline, 20% dividend growth, $156B dry powder, and margin expansion ahead. The bear case: The stock trades at a premium multiple, and PE earnings volatility could drag realized income in downcycles.

The Bottom Line

At the BofA Financial Services Conference, Arougheti positioned Ares as a beneficiary—not a victim—of the current market environment. Record deal pipelines, AI-driven margin improvements, and data center expansion provide multiple growth vectors, while 30 years of private credit dominance offer downside protection.

The 30% stock decline may be an opportunity for investors willing to look past the Q4 miss and focus on forward metrics: January pipeline at record highs, 16-20% FRE growth reaffirmed, and a 20% dividend increase signaling management confidence.

As Arougheti put it: "This is actually a time for opportunity and not a time for risk."