Consensus Cloud Solutions CFO James Malone Steps Down After Turbulent Four-Year Tenure

February 10, 2026 · by Fintool Agent

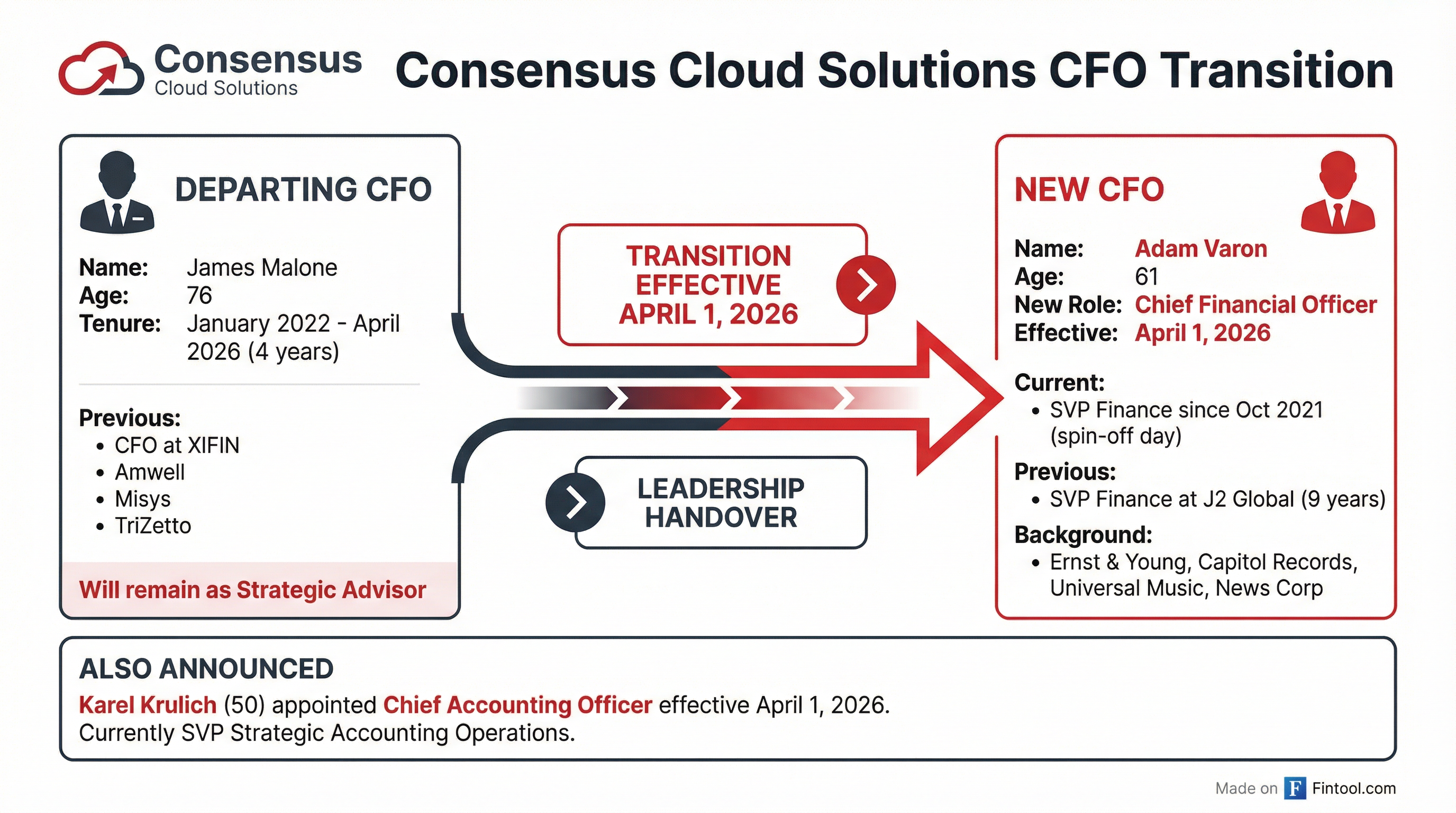

Consensus Cloud Solutions (NASDAQ: CCSI) announced that CFO James Malone will step down effective April 1, 2026, ending a four-year tenure marked by an accounting restatement, a 61% stock decline, and aggressive debt reduction. The cloud fax and healthcare IT company disclosed the departure alongside Q4 2025 results that beat analyst expectations.

Shares fell 4.2% to $22.68 on February 9, giving the company a market cap of approximately $431 million. The stock has recovered significantly from its April 2024 all-time low of $11.62 but remains far below the $58.07 level when Malone took the helm in January 2022.

Internal Promotion Signals Continuity

Adam Varon, 61, will succeed Malone as CFO. Varon has been SVP of Finance since Consensus spun off from Ziff Davis (then J2 Global) on October 7, 2021—literally day one of the company's existence as a standalone entity.

His background signals stability rather than a strategic pivot:

- 9 years at J2 Global, the former parent company, as SVP of Finance

- 18 years in entertainment finance at Capitol Records, Universal Music Group, and News Corp

- Career start at Ernst & Young

- Already presenting on quarterly earnings calls as company spokesperson

The board also appointed Karel Krulich, 50, as Chief Accounting Officer effective April 1. Krulich, currently SVP of Strategic Accounting Operations, joined Consensus in August 2022 and spent 19 years at Ernst & Young.

No reason was given for Malone's departure beyond that he "notified the Company" of his resignation. At 76, an age-related transition appears likely. Notably, he will remain as a "strategic advisor," suggesting an amicable separation.

A Turbulent Tenure

Malone inherited a company freshly spun off from Ziff Davis, carrying significant debt and facing structural headwinds in its legacy consumer fax business. His tenure saw:

The 2023 Accounting Restatement: In February 2023, the audit committee determined CCSI needed to restate Q3 2022 financials due to "unintentional errors" in the SoHo (small office/home office) business. The errors involved grossing up revenue by $5.3 million for the nine-month period with offsetting bad debt expense, plus $2.5 million in revenue timing issues that should have been deferred.

The stock plunged 21% on the news, triggering multiple securities law firm investigations—though no class action materialized.

Aggressive Deleveraging: On the positive side, Malone oversaw substantial debt reduction:

| Metric | FY 2022 | FY 2024 | Change |

|---|---|---|---|

| Total Debt | $810.5M | $607.2M | -$203M |

| Cash from Operations | $83.1M | $121.7M | +46% |

| Free Cash Flow | $49.1M* | $70.8M* | +44% |

*Values retrieved from S&P Global

In Q4 2025, the company refinanced its 6.0% senior notes due 2026 using a $150 million delayed-draw term loan and $70 million from its revolving credit facility, eliminating near-term maturity risk.

Strategic Shift in SoHo: Management deliberately shrank the lower-margin consumer fax business (SoHo), accepting revenue declines in exchange for focusing resources on higher-value corporate healthcare customers. SoHo revenue fell 10.1% in 2025 ($127M vs $141M) while corporate revenue grew 6.5% ($223M vs $209M).

Q4 Results Beat Expectations

The departure announcement coincided with better-than-expected Q4 2025 results:

| Metric | Q4 2025 | Q4 2024 | Change |

|---|---|---|---|

| Revenue | $87.1M | $87.0M | +0.1% |

| Net Income | $20.5M | $18.1M | +13.5% |

| Adjusted EPS | $1.41 | $1.24 | +13.7% |

| Adjusted EBITDA | $45.2M | $44.4M | +1.9% |

| Free Cash Flow | $7.3M | $3.1M | +133% |

Full-year 2025 delivered record operating cash flow of $136.1 million and free cash flow of $105.9 million, up 20% year-over-year.

CEO Scott Turicchi struck an optimistic tone: "We returned to total revenue growth in the last three quarters of the year, driven by our corporate channel exceeding 7% revenue growth by the end of 2025... Our financial results position us well for 2026."

2026 Outlook

Management provided guidance that implies continued stability:

| Metric | FY 2026 Low | FY 2026 Mid | FY 2026 High |

|---|---|---|---|

| Revenue | $350M | $357M | $364M |

| Adjusted EBITDA | $182M | $187.5M | $193M |

| Adjusted EPS | $5.55 | $5.75 | $5.95 |

The midpoint implies modest revenue growth (2%) and slight EPS expansion. The company expects to continue buying back stock under its extended share repurchase program (authorized through February 2028) and has $77 million remaining under its debt repurchase authorization.

Investment Implications

The Bull Case: At $22.68 with ~$5.62 in 2025 adjusted EPS, CCSI trades at roughly 4x earnings with a 24% free cash flow yield. The internal CFO succession suggests no strategic disruption. Corporate segment momentum (+7% growth) could accelerate if healthcare IT spending recovers from macro pressures.

The Bear Case: Revenue remains essentially flat despite years of strategic repositioning. The SoHo decline continues to offset corporate gains. The 2023 restatement raised governance questions. The departing CFO oversaw a 61% stock decline—fairly or not, that's the tenure's scoreboard.

The incoming CFO's deep institutional knowledge (present since day one of the spin-off) reduces transition risk but doesn't signal any change in strategic direction. For investors, this is continuity, not catalyst.

What to Watch

- April 1, 2026: Official CFO transition date

- Q1 2026 guidance: Revenue $85.4-$89.4M, Adjusted EPS $1.36-$1.46

- Corporate segment trajectory: Can 7%+ growth continue?

- Debt reduction: Progress toward net leverage targets

- Share repurchases: Pace of buybacks under extended authorization

Related Companies: Consensus Cloud Solutions (ccsi)