CECO Environmental to Acquire Thermon for $2.2 Billion, Creating Industrial Solutions Powerhouse

February 24, 2026 · by Fintool Agent

Ceco Environmental is acquiring Thermon Group Holdings in a $2.2 billion cash-and-stock transaction that combines two industrial specialists riding the AI infrastructure and power generation boom. The deal, announced alongside CECO's record Q4 2025 results, values Thermon at approximately 17x adjusted EBITDA—or roughly 13x including $40 million of expected synergies.

The Deal Structure

Thermon shareholders have three options for consideration, subject to proration:

| Election Type | Consideration per Thermon Share | Implied Value |

|---|---|---|

| Mixed (default) | 0.6840 CECO shares + $10.00 cash | $63.13 |

| All-Cash | $63.89 cash | $63.89 |

| All-Stock | 0.8110 CECO shares | $63.00 |

The mixed consideration represents a 26.8% premium to Thermon's February 23 closing price of $49.77. Upon closing, CECO shareholders will own approximately 62.5% of the combined company and Thermon shareholders about 37.5%.

Both boards unanimously approved the transaction, and supporting stockholders holding 15.2% of CECO shares have signed voting agreements. The deal is expected to close mid-2026, subject to shareholder approvals and regulatory clearances.

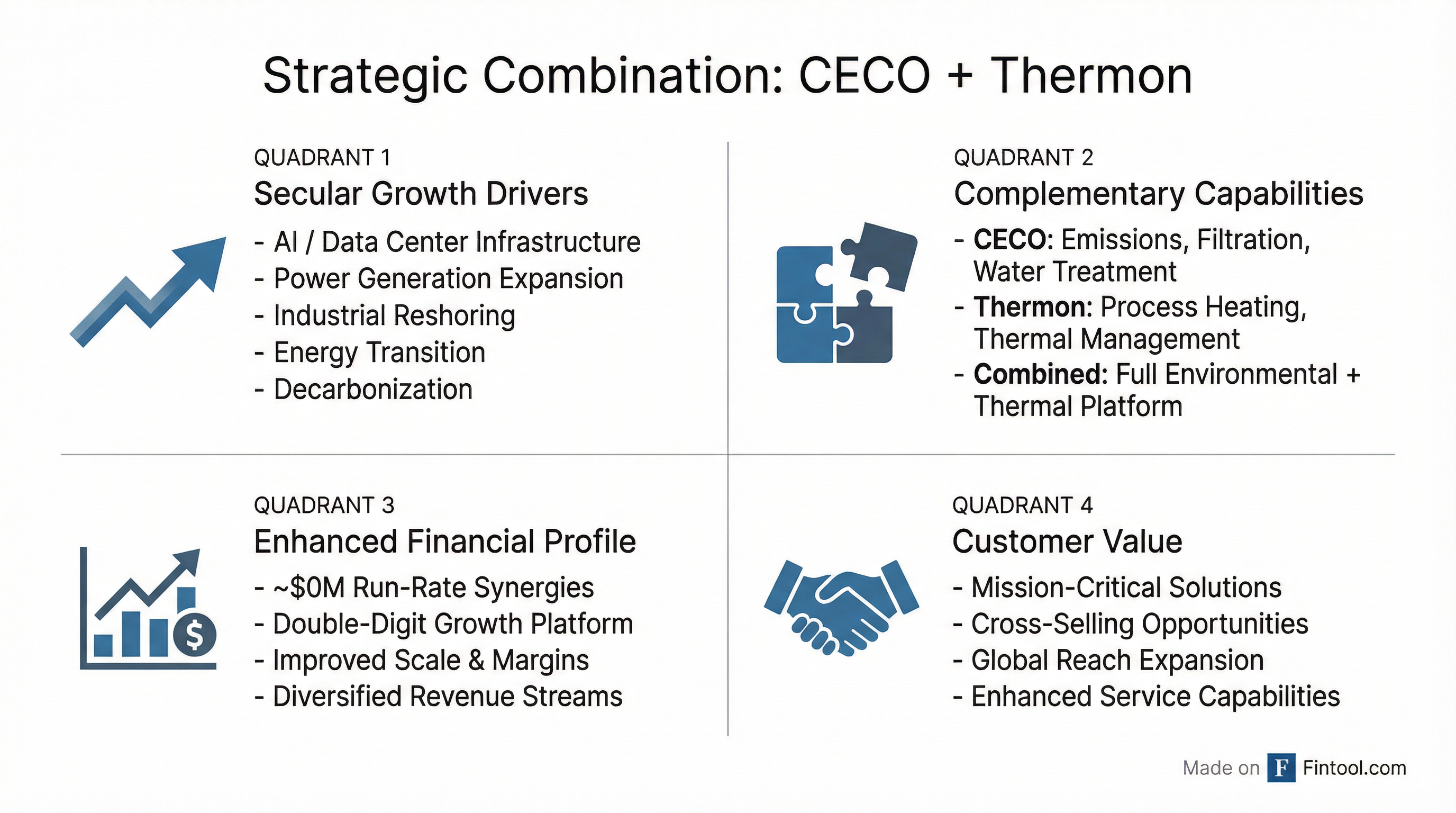

Strategic Rationale: Riding Secular Tailwinds

The combination creates a comprehensive industrial solutions platform with approximately $1.5 billion in combined revenue and $295 million in adjusted EBITDA (including synergies), positioning the company to capitalize on multiple converging trends:

AI and Data Center Infrastructure: Thermon has rapidly pivoted toward the data center opportunity, launching liquid load bank solutions to test critical cooling systems in AI data centers. The company's quote log for these products has doubled sequentially to $60 million, and management expects this to become a multi-year growth driver.

Thermon CEO Bruce Thames noted in the company's most recent earnings call that liquid-cooled data centers—which offer higher efficiency and server densities—now represent 40-50% of new data centers planned for construction.

Power Generation Expansion: CECO has secured its largest-ever project booking—approximately $135 million for a natural gas power generation facility in Texas. The company's power-related pipeline exceeds $1 billion, supported by baseload power needs for data centers, nuclear momentum, and alternative energy backup solutions.

Industrial Reshoring: Both companies benefit from semiconductor investments, chemical and petrochemical expansion, and broader manufacturing reshoring trends driven by supply chain security concerns.

CECO's Record Q4 Sets the Stage

The merger announcement coincided with CECO's strongest results ever:

| Metric | Q4 2025 | Year-over-Year Change |

|---|---|---|

| Revenue | $215M | +35% |

| Orders | $329M | +50% |

| Backlog | $793M | +47% |

| Adjusted EBITDA | $29.8M | +57% |

For the full year, CECO achieved orders exceeding $1 billion for the first time, while revenue reached $774 million—up 39% including 25% organic growth.

Management raised 2026 standalone guidance (excluding Thermon) to revenue of $925-975 million and adjusted EBITDA of $115-135 million, citing a sales pipeline now exceeding $6.5 billion that is "converting quickly."

Thermon: The Acquisition Target

Thermon brings a complementary portfolio of industrial process heating and thermal management solutions:

| Metric | FY 2025 | FY 2024 | FY 2023 |

|---|---|---|---|

| Revenue | $498M* | $495M | $441M |

| EBITDA | $104M* | $99M | $78M |

| EBITDA Margin | 20.9%* | 20.1% | 17.7% |

*Values retrieved from S&P Global

Thermon's higher EBITDA margins (approximately 21% vs. CECO's 10%) and significant aftermarket/short-cycle business add a more stable revenue stream to CECO's project-driven model. The company has also been expanding into medium voltage heaters for electrification applications, with a pipeline exceeding $150 million.

Market Reaction

Despite the strategic logic, stocks diverged following the announcement:

- CECO: Down 12.6% to $62.95, reflecting deal execution risk and the substantial stock component

- Thermon: Up 5.7% to $52.61, trading below the implied deal value of $63.13, suggesting some skepticism about closing

The divergence between Thermon's trading price and the deal value creates a merger arbitrage spread of approximately 17%, wider than typical for transactions at this stage, likely reflecting the mid-2026 expected close date and regulatory uncertainties.

Financing and Integration

Bank of America has committed $200 million in incremental term loans, with additional capacity from CECO's existing credit facility. CECO ended 2025 with leverage of approximately 2.2x and liquidity of $124 million.

The merger agreement includes customary termination fees—$74.7 million payable by Thermon and $105 million by CECO under specified circumstances—and a "go-shop" period has not been disclosed, though both boards unanimously support the transaction.

What to Watch

Near-term catalysts:

- Proxy filings with detailed synergy breakdowns and pro forma financials

- Shareholder meeting dates for both companies

- Hart-Scott-Rodino antitrust clearance timeline

Integration execution:

- Achievement of $40 million synergy target

- Cross-selling traction between environmental and thermal solution portfolios

- Retention of Thermon's technical talent and customer relationships

Market tailwinds:

- Data center capex trends and liquid cooling adoption rates

- Power generation project awards and conversion timelines

- Industrial reshoring policy developments