Danaher Pays $9.9 Billion for Masimo, Expanding Diagnostics Empire

February 17, 2026 · by Fintool Agent

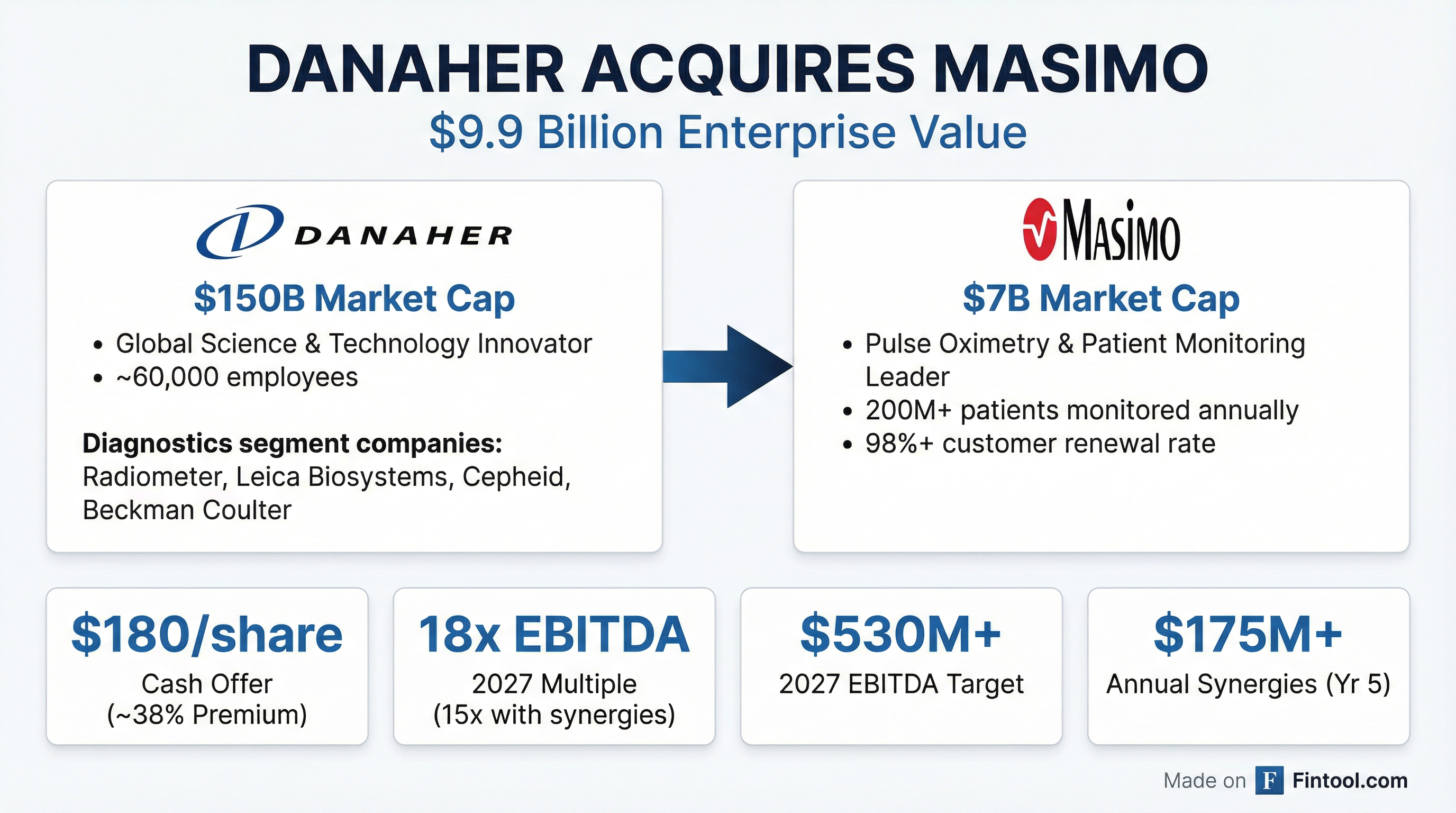

Danaher is acquiring Masimo, the pulse oximetry pioneer, for $180 per share in cash—a 38% premium that values the patient monitoring company at $9.9 billion including debt.

The deal marks Danaher's largest acquisition since the $21 billion Cytiva transaction in 2020 and signals CEO Rainer Blair is ready to deploy capital aggressively after signaling improved M&A conditions on last month's earnings call.

"We've followed this innovative company for many years and see it as an exceptional strategic fit for Danaher," Blair said in the announcement. "Masimo's advanced sensor technology and AI-enabled monitoring bring powerful new capabilities to our diagnostics portfolio."

The Deal Terms

Masimo shareholders will receive $180 per share in cash, representing an 18x multiple on 2027 estimated EBITDA—or 15x including the full benefit of expected synergies.

Under Danaher's ownership, Masimo is expected to generate EBITDA exceeding $530 million in 2027. Danaher projects more than $125 million in annual cost synergies and over $50 million in annual revenue synergies by the fifth year post-close.

The acquisition is expected to be accretive to adjusted diluted EPS by $0.15-$0.20 in the first full year and approximately $0.70 by year five.

| Deal Metric | Value |

|---|---|

| Price Per Share | $180 (all cash) |

| Enterprise Value | $9.9 billion |

| Premium | 38% |

| EV/EBITDA (2027) | 18x (15x with synergies) |

| Expected Close | H2 2026 |

| Yr 1 EPS Accretion | $0.15-$0.20 |

| Yr 5 EPS Accretion | $0.70 |

Danaher will fund the acquisition with cash on hand and proceeds from debt financing. Citi served as financial advisor and Kirkland & Ellis as legal counsel.

Strategic Rationale: Strengthening Diagnostics

Masimo will become a standalone operating company within Danaher's Diagnostics segment, joining Radiometer, Leica Biosystems, Cepheid, and Beckman Coulter Diagnostics.

The acquisition addresses a clear gap in Danaher's portfolio. While Beckman Coulter dominates in clinical chemistry and immunoassay and Cepheid leads in molecular diagnostics, Danaher lacked a meaningful presence in acute care patient monitoring—exactly where Masimo excels.

Masimo SET pulse oximetry technology is used in all 10 of the top U.S. hospitals as ranked by Newsweek and monitors an estimated 200 million patients globally each year. The company maintains a 98%+ customer renewal rate with over 80% recurring revenue.

"Masimo's trusted brand and differentiated technology will greatly strengthen our diagnostics franchise," Blair said. "We see opportunities to expand Masimo's reach and continue improving outcomes for patients, particularly those in acute care settings."

Julie Sawyer Montgomery, EVP for Diagnostics at Danaher, emphasized the technology angle: "Integrating these strengths into Danaher will create meaningful opportunities to innovate for clinicians and improve decision making in critical settings."

The deal is expected to accelerate Danaher's Diagnostics segment from low-single-digit to high-single-digit core revenue growth over the long term.

Masimo's Transformation Journey

The acquisition comes as Masimo executes a strategic pivot back to its core medical technology business. Under CEO Katie Szyman, who took the helm in 2025, the company divested its Sound United consumer audio business in September 2025 and unveiled an ambitious long-range plan at its December investor day.

Masimo's standalone targets called for 7%-10% revenue CAGR through 2028, operating margins reaching approximately 30%, adjusted EPS of $8.00, and cumulative operating cash flow of roughly $1 billion from 2026-2028.

| Metric | FY 2024 | FY 2025E | 2028 Target |

|---|---|---|---|

| Revenue | $1.4B | $1.51-$1.53B | 7-10% CAGR |

| Operating Margin | 19.3% | 27.3-27.7% | 30% |

| Adj. EPS | $3.29 | $5.40-$5.55 | $8.00 |

The company's growth algorithm centered on four pillars: accelerating U.S. pulse ox growth (contributing 2.75-3.75 percentage points), penetrating international pulse ox markets (1.75-2.25 ppts), expanding advanced monitoring (2.5-3.0 ppts), and executing new product launches (up to 1 ppt).

A three-wave innovation pipeline included near-term AI-enabled sensors (Smart SET for opioid-induced respiratory depression detection launching H1 2026), next-generation Root monitors (2027), and future wearables for continuous patient monitoring.

The Apple Factor

Masimo has been locked in a high-stakes patent dispute with Apple that recently delivered a major win. A California jury found Apple infringed Masimo's patents, awarding $634 million in damages—with implied interest still to be determined.

The International Trade Commission (ITC) also announced a new proceeding in November 2025, with a Delaware trial anticipated in 2027 or later.

Danaher's 8-K filing acknowledges litigation risks, noting the possibility that "stockholder litigation in connection with the transactions contemplated by the merger agreement may result in significant costs." However, the company appears comfortable assuming these contingencies as part of the broader strategic opportunity.

Danaher's M&A Playbook Returns

The deal validates signals Blair sent on Danaher's January 28 earnings call, where he described the M&A environment as "more constructive" with "valuations moving in the right direction."

"Our cash flow generation puts our balance sheet in a place where we're able to act on opportunities," Blair said at the time. "We're gonna stick with our discipline of looking at end markets that we believe have long-term tailwinds, attractive assets within that market that have defensible value or value creation opportunities that we can compound over time."

Danaher reported FY 2025 revenue of $24.6 billion with $6.4 billion in operating cash flow. The company's net debt stood at approximately $13.8 billion at year-end, leaving ample capacity for a deal of this size.*

| Danaher Metric | FY 2023 | FY 2024 | FY 2025 |

|---|---|---|---|

| Revenue | $23.9B | $23.9B | $24.6B |

| EBITDA | $7.5B* | $7.5B* | $7.1B* |

| Cash from Operations | $7.2B | $6.7B | $6.4B |

| Cash & Equivalents | $5.9B | $2.1B | $4.6B |

*Values retrieved from S&P Global

For FY 2026, Danaher had guided to 3%-6% core revenue growth and adjusted EPS of $8.35-$8.50 before accounting for the Masimo acquisition.

What to Watch

Regulatory Path: The deal requires Hart-Scott-Rodino clearance and other regulatory approvals. Danaher's diagnostics focus and Masimo's patient monitoring positioning suggest limited antitrust overlap, though review timelines remain a wildcard.

Shareholder Vote: Masimo shareholders must approve the transaction. The 38% premium and Danaher's reputation for operational excellence should facilitate approval, but activist or competing bidder risks exist until the vote concludes.

DBS Execution: Danaher's famed Business System (DBS) will be critical to realizing the projected synergies. Management's track record on previous acquisitions like Cytiva suggests high confidence, but integration complexity in a regulated industry bears monitoring.

Innovation Pipeline: Masimo's AI-enabled Smart SET sensors and next-generation monitors were central to its standalone growth story. Whether Danaher accelerates or reshapes these programs will impact long-term value creation.

The transaction is expected to close in the second half of 2026.