Dover CEO Sees Three-Year Fueling Upcycle, $1.5B Ready for M&A at Barclays Conference

February 17, 2026 · by Fintool Agent

Dover Corporation CEO Rich Tobin told investors at the Barclays Industrial Select Conference in Miami Beach that the company's 2026 outlook is materially stronger than where it stood a year ago—and unlike last year, he has the order book to prove it.

"The setup for 2026 is constructive," Tobin said. "We actually have hard data points that, generally speaking, in a normal year, we wouldn't have. We're fundamentally mostly a short cycle business. In any given year, we would expect to see orders accelerate in Q1 for deliveries in Q2 and Q3. We actually had a lot of orders come in in Q4."

That's a stark contrast to early 2025, when Dover was "betting on the come" based on expectations of lower interest rates. Instead, tariff volatility derailed the U.S. industrial economy from February through September, causing widespread CapEx deferrals across Dover's customer base.

Dover shares are trading at $230.67, up 24% year-to-date and near their 52-week high of $237.54.

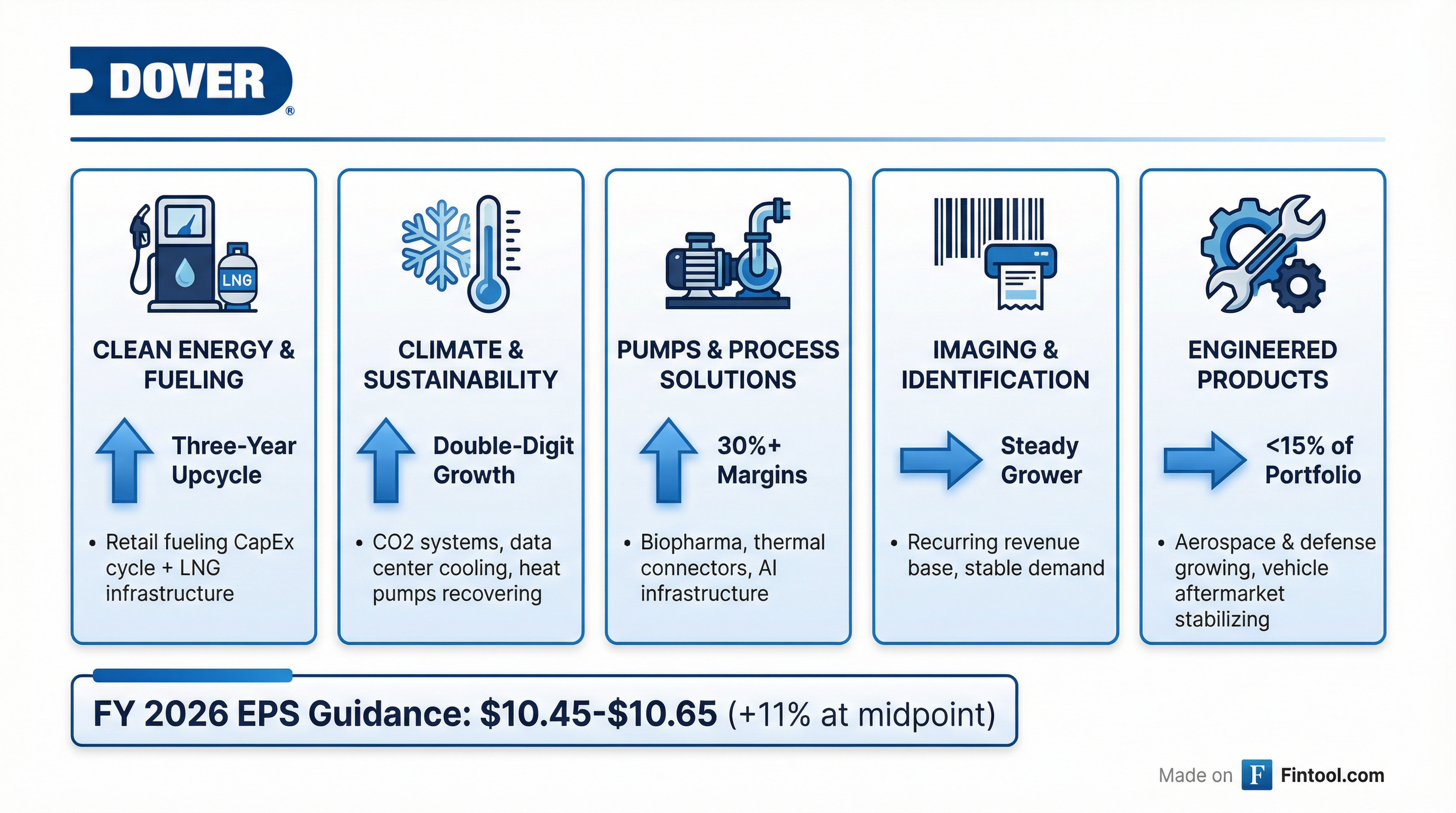

Two Segments Set to Lead

Tobin identified Clean Energy & Fueling and Climate & Sustainability Technologies as the primary growth engines for 2026, each benefiting from distinct secular tailwinds that have been building for several years.

A Three-Year Fueling Upcycle Begins

Clean Energy & Fueling has been transformed through aggressive M&A in the cryogenic and LNG space. Dover has roughly doubled the segment's revenue by acquiring nine cryogenic component businesses, which it is now consolidating from nine factories down to four—a process Tobin expects to complete by midyear 2026.

The traditional retail fueling business is also turning. After years of underinvestment as the industry questioned ICE vehicle demand due to EV expectations, Tobin sees a multi-year CapEx recovery beginning:

"We went through a period—I remember being here in 2001 when ICE was uninvestable, right? EVs were taking over the world. Every auto OEM was gonna build a battery plant. Well, the worms turned a little bit here. Not only is there a requirement for refurbishment of the installed base, everybody woke up and discovered that profit margins on gasoline, that Costco has proven, has been pretty lucrative. We would think that we're likely gonna go into a three-year upcycle on fueling solutions."

Clean Energy & Fueling grew 4% organically in Q4 2025 and is tracking toward Dover's goal of 25% segment margin.

Data Centers and CO2 Refrigeration Power Climate Segment

Climate & Sustainability Technologies posted 9% organic growth in Q4, driven by three distinct product lines:

-

Brazed Plate Heat Exchangers: Record U.S. shipments in Q4, with demand for liquid cooling of data centers booking "well beyond Q1."

-

CO2 Refrigeration Systems: Continuing at a double-digit growth clip. Dover brought European CO2 technology to the U.S. market and grew this business from zero to over $300 million in revenue in approximately 18 months.

-

Refrigerated Display Cases: National retailers are resuming maintenance and upgrade spending after tariff-related delays throughout 2025.

The segment posted a book-to-bill of 1.21 in Q4—a strong forward indicator.

$1.5 Billion in Dry Powder—But Patience on Price

Dover deployed $700 million across four strategic acquisitions in 2025, primarily in the Pumps & Process Solutions segment. Combined with a $500 million accelerated share repurchase initiated in November 2025, the company has self-funded all capital deployment while maintaining $1.5 billion of liquidity.

Tobin was candid about the M&A environment: the middle market where Dover operates saw few deals in 2025 as corporate activity was dominated by large-cap breakups. The deals that did transact went off at elevated multiples.

"We've demonstrated a lot of patience sitting on $1.5 billion of liquidity for 18 months," Tobin said. "If you look at the M&A markets in total, you would say you read the paper, and it's a record year, but the deals that were there were very large. The middle market, where we participate, there was very few."

Looking ahead, he sees favorable conditions for sellers to bring assets to market—lower discount rates, strong equity markets—but early 2026 pricing signals remain elevated:

"The early signal is they're gonna be kind of high, but maybe with more deals coming, that'll put some top-line pressure on multiples paid. But it's February sixteenth, so we'll see it over the next 180 days or so."

If multiples don't cooperate, Tobin confirmed that share repurchases remain an option: "At the end of the day, capital return is always an option for us."

Pumps at 30%+: Growth Over Margin Expansion

Dover's Pumps & Process Solutions segment achieved 30.3% margins in FY 2025 on 13.4% revenue growth, driven by biopharma components, thermal connectors for data center liquid cooling, and precision components for natural gas infrastructure.

When asked about further margin expansion, Tobin was pragmatic:

"We're north of 30 now. We'll take 30 all day long and just grow the top line as quickly as we can. If we were to do M&A in there, the likelihood, it would probably be dilutive, because assets that generate margins north of 30 don't come available very often, and when they do, they're very expensive."

The segment benefits from exposure to AI infrastructure build-out, including thermal connectors for liquid cooling and Sikora's inspection equipment for high-voltage wire and cables—critical components for data center power delivery.

Stock Performance and Valuation

Dover's stock has gained 24% year-to-date, outperforming the broader industrial sector. At current prices of $230.67, the stock trades at approximately 22x the midpoint of 2026 EPS guidance ($10.55).

| Metric | FY 2023 | FY 2024 | FY 2025 | FY 2026E |

|---|---|---|---|---|

| Revenue ($B) | $7.68 | $7.75 | $8.09 | $8.57* |

| EBITDA ($B) | $1.58 | $1.63 | $1.82 | $2.00* |

| EBITDA Margin | 20.5% | 21.0% | 22.5% | 23.3%* |

| Adj. EPS | $6.71 | $10.09 | $9.61 | $10.55** |

*Consensus estimates. **Midpoint of company guidance ($10.45-$10.65). Values from S&P Global.

A live audience poll at the conference showed approximately 50% of attendees favoring M&A as the preferred use of excess cash, with a consensus view that Dover should trade at 19-20x forward earnings—modestly below current levels.

The main perceived headwind on valuation, according to audience feedback, remains the conglomerate discount typically applied to diversified industrials.

What's Changed Since Last Year

Tobin's commentary highlighted a meaningful shift in Dover's visibility compared to the uncertain start to 2025:

| Factor | Early 2025 | Early 2026 |

|---|---|---|

| Order Visibility | "Betting on the come" | Q4 orders accelerated into backlog |

| Tariff Environment | February-September uncertainty | Largely resolved |

| Interest Rates | Hoping for cuts | Lower than expected |

| Retail Fueling | EV concerns, CapEx deferred | Three-year upcycle beginning |

| Cryogenic Footprint | 9 factories (post-M&A) | Consolidating to 4 by midyear |

| Vehicle Aftermarket | Double-digit decline | Stabilizing, constructive bookings |

"It feels eerily similar than it did this time last year. I thought the setup was good going into 2025, until we ran into tariff tumults in February, and it kind of upset the apple cart," Tobin reflected.

The difference now: "We go in kind of a credit position from a backlog point of view, that makes us feel good for the setup for the year."

What to Watch

- Q1 2026 earnings (expected late April): Validation of order flow translating to revenue; seasonal ramp into Q2-Q3 peak

- Cryogenic consolidation completion: Factory footprint reduction to 4 sites by midyear should drive margin accretion in H2

- M&A pipeline: Tobin signaled proprietary deal flow and expects to "be active in 2026" if pricing cooperates

- Heat pump recovery: European heat pump manufacturers have called the market up; SWEP brazed plate demand could reaccelerate

- Retail refrigeration CapEx: Continued release of pent-up spending from 2025 tariff delays

Related: Dover Corporation Research